Questions on Trumponomics

Dave Mohr, Chief Investment Strategist at Old Mutual.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Are we on the verge of a shift in the global macroeconomic environment? That seems to be the overarching question as investors still try to come to terms with the Donald Trump presidency. Since the global financial crisis, the world has been stuck in a steady growth, low inflation rut, punctuated by the odd crisis. The US is a case in point: between 1950 and 2008, US real economic growth averaged 3.4% and inflation 3.8%, but from 2010 onwards, the averages are 2% and 1.6% respectively. Interest rates have been close to zero over the latter period as a result.

For some, Trump’s election promises to yank the US (and by implication the world) out of this sluggish trend with tax cuts, deregulation and deficit spending, heralding a potential return of boom-bust cycles. For sure, part of the reason behind the tepid growth and low inflation has been psychological, the absence of what the great British economist John Keynes referred to as “animal spirits”, the appetite to take risks and reap rewards. A shift in confidence can result in an increased willingness to spend and invest, creating a feedback loop of higher growth, leading to more spending. However, the big structural factors that have dampened global growth remain: China’s rebalancing, slower population growth in the developed countries, technological progress weighing on production prices, a vast global labour force putting pressure on wages in the West, a debt overhang from the pre-2008 boom years, a savings glut and persistent current account surpluses in China, Germany and the oil producers. For instance, Abenomics, the attempt by Japanese Prime Minister Abe to shock the economy out of its deflationary rut, has largely failed, despite much initial excitement.

Trumponomics or Reaganomics?

Some commentators are also referring to the return of “Reaganomics”. However, the starting conditions are very different. President Reagan slashed taxes and ramped up defence spending, but probably the most important contributor to the Reagan boom was that the Fed’s interest rate was 19% in 1981 at the start of his first term and the US in a deep recession. As inflation declined, rates halved over the next four years and the US economy took off. US equities and bonds entered a multi-year bull market. By contrast, Trump will start his term with ultra-low rates and low unemployment, and with the current bull market already eight years old.

The Reagan era’s combination of high interest rates and loose fiscal policy resulted in a very strong dollar. South Africans paid 70 cents for a dollar at the start of Reagan’s first term in 1981 but R2 by the time his second term began in 1985. It is not a given that the dollar will surge though: a strong deficit-funded US economy under George W. Bush resulted in a weak dollar, even as the Fed steadily hiked rates. The rise of the dollar (to a 13-year high on a trade-weighted basis) and the strength of US equities (the S&P 500 hit a new record high last week) suggest investors are betting on a Reaganesque outcome. This might be premature, especially if Trump follows through on some of his anti-trade promises.

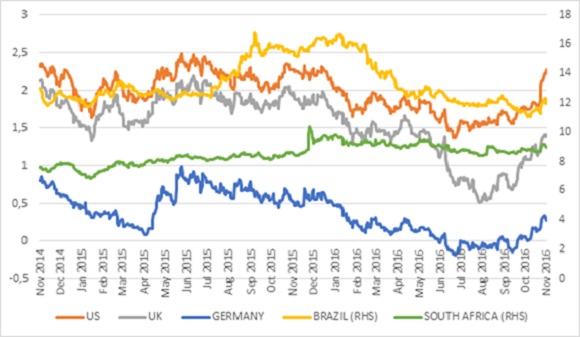

At the same time, there has been a massive sell-off of global bonds in anticipation of higher inflation and interest rates. However, developed market bonds have been weakening since the middle of the year as investors questioned the commitment of the Japanese and European central banks to expanding monetary stimulus. The rise in market-based inflation expectations since the election does indeed make the expansion of these central banks’ quantitative easing programmes less likely. We have held no global bonds in our portfolios for a long time.

Fed still on course

With recent US economic data being fairly solid, the Federal Reserve is likely to hike by 0.25% next month, with Chair Janet Yellen confirming this view in testimony to Congress. The stronger US dollar is one reason why the Fed did not increase rates by more than the single December 2015 hike over the past two years. A strong dollar dampens US inflation and hurts the earnings of exporters. A leading Fed official argued that one further hike would leave US interest rates at a neutral level, in other words where it is neither too hot nor too cold. Rate hikes beyond December will then most likely depend on how actual inflation behaves. In the shorter term, the decline in the oil price over the past month also puts a lid on inflationary pressures.

Closer to home

The short to medium term impact of all this on South Africa lies in the exchange rate. While all emerging market currencies sold off after the US election, the rand has held up relatively well. The Mexican peso was hardest hit, while the Turkish lira fell to a record low on domestic political concerns. The Russian rouble also wobbled further after the dismissal of the economy minister. The rand has traded in a broad range of around R13.50 to R14.50 to the dollar since July. This range is weak enough to continue supporting exports and tourism, but still stronger than the average exchange rate over the preceding period, supporting the view that inflation and interest rates have peaked. Given the renewed uncertainty, interest rate cuts are off the table for now. While the rand has gained around 8% against the US dollar since the start of the year, it has appreciated by 14% against the Chinese yuan, which is helpful given how much of our goods imports come from China.

The outlook for inflation and interest rates in turn are important for consumer spending. Consumption in its various forms (groceries, clothing, transport, housing, medical treatment, education, leisure) accounts for two thirds of the local economy. If inflation declines next year, it should take pressure off households that are currently clearly facing the squeeze. As a result of rising interest rates over the past two years, the cost of servicing debt has eroded an additional 1% of household disposable income. Since consumer debt is growing by less than income, interest rates are the key variable that could ease or worsen the pressure on households.

The squeeze is on

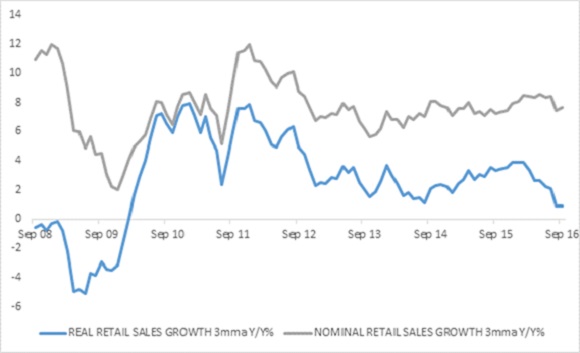

If households are under pressure, so are retailers. New StatsSA data shows that real retail sales grew by 1.4% year-on-year in September, while declining marginally in the third quarter (putting a damper on the expected third quarter GDP growth rate). Nominal retail sales grew by 8.1% year-on-year. This implies retail inflation of almost 7%, up from 4% (overall consumer inflation includes services and fuel, where prices have risen much more slowly). The growth rate of nominal spending has remained in the 7-8% range for some time. In other words, the amount that consumers are spending at retailers has grown steadily, but what consumers get for their money has been growing much more slowly. The rise in inflation is also eating into listed retailers’ margins (since they are not able to fully pass on higher merchandise costs).The latest round of results and trading updates from local listed retailers has largely been disappointing, especially from clothing retailers. Local retailers are also increasingly facing competition from foreign entrants whose sales will show up in the official StatsSA numbers. The JSE’s general retail index (which includes clothing retailers) is down 20% since the start of the year and decreased by 30% since the recent peak in August. The JSE’s food and drug retailers index (containing the likes of Shoprite and Pick n Pay) is down 10% over the past four months.

While consumers will be hoping for a stronger rand as the year draws to a close, investors should remain appropriately diversified. Although the weaker rand would hurt the local bond market, it would boost offshore investments and JSE-listed rand hedges. A stronger rand will benefit interest rate-sensitive assets. Our Strategies remain diversified for each targeted outcome, with overweight allocations to global equities and local fixed income, and underweight allocations to local equities with zero global bonds.

Chart 1: Trade-weighted US dollar index

Source: Datastream

Chart 2: Global 10-year government bond yields, %

Chart 3: South African retail sales growth, %

Source: Datastream