Putting a tough year behind us

Dave Mohr, Chief Investment Strategist at Old Mutual.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

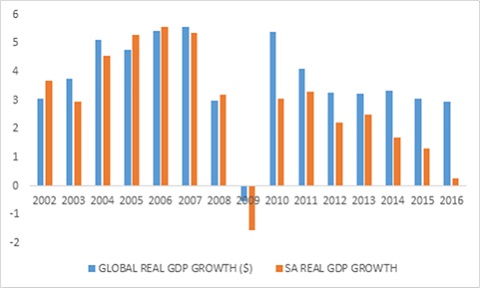

It’s official. 2016 truly was a terrible year. According to StatsSA, gross domestic product (GDP), a broad measure of a country’s economic activity, declined by 0.3% in the fourth quarter after inflation. For the year as a whole, GDP growth was barely positive at 0.3%, the slowest expansion in a calendar year since the 1.5% decline in 2009. Chart 1 also shows how growth declined every year since 2012. At least things never got as bad as in Brazil, where it was announced last week that GDP contracted by 3.6% in 2016, the second consecutive negative year.

A sharp 11.5% decline in the mining sector was largely to blame for the fourth quarter contraction. Manufacturing and agriculture were also negative. Agriculture and mining subtracted 0.6% from GDP growth for 2016 as a whole. In the case of agriculture, it was the eighth consecutive negative quarter. However, the outlook for agriculture is much better as the drought came to an end in most parts of the country and crop sizes are expected to rebound. This has already been reflected in substantial declines in traded maize and wheat prices.

One can also look at GDP from the spending side (instead of the contribution by sector from the production side). What is notable is the 3.9% decline in fixed investment spending in 2016, the first such decline since 2009. Private fixed investment spending collapsed by 6% in 2016, amid depressed business confidence due to a combination of policy and political uncertainty, threats of a ratings downgrade and weak demand. However, the fourth quarter saw positive growth in fixed investment.

Cycle has turned

The fourth quarter GDP release contained evidence that the cycle has turned with a modest improvement in growth ahead. Household consumption spending of 2.2% was reasonably healthy. Exports increased by 12.5%, and came from mining inventories, which suggest mining production would have to increase in the coming quarters if companies respond to the higher dollar commodity prices.

GDP can also be looked at from the perspective of income. Compensation of employees (the wage bill) grew slower at 7% year-on-year, largely due to a slowdown in Government’s wage bill growth. This suggests some progress on the part of Government in containing costs. With inflation set to decline, overall wage bill growth of 7% should translate into real disposable income growth for households. Slower compensation growth also implies that companies are claiming a bigger slice of the GDP pie. Gross operating surplus for the private sector, a rough proxy for profits, grew at a faster annual pace of 6.3% in the fourth quarter.

Global environment more supportive

Significantly, the global environment is turning more supportive of the domestic economy. The global growth forecast of the Organisation for Economic Co-operation and Development (OECD), representing the most advanced economies, was revised from 3% in 2016 to 3.5% in 2018. This represents a modest improvement in global growth and indicates that growth forecasts are no longer being revised downwards. At turning points forecasters are typically too pessimistic, so forecasts may be upgraded. The global growth slide that started in 2011 (when the global economy grew by 4%) bottomed out last year. South Africa, as a small open economy, usually follows the global cycle with a lag. It materially underperformed over the last few years, but should follow the world economy.

Disappointed investors

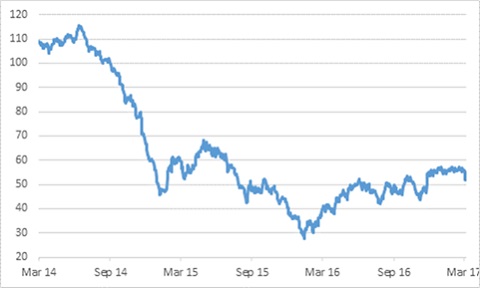

2016 also wasn’t a great year for investors. The average retail balanced fund returned only 1.4%. Is this year’s outlook better? The JSE All Share Index is hovering below 52 000, a level it first hit in July 2014. In other words, investors have basically just earned dividends, with no price appreciation at an index level. But this period of underperformance means valuations are a lot more reasonable. In dollar terms, the JSE is back where it was in 2010, seven lean years indeed. The gap between rand and dollar returns points to how much the weaker currency has helped the JSE over this period as more than half the earnings comes from abroad. The rand could therefore complicate matters if it continues strengthening, but it was weaker last week as commodity prices, particularly oil, pulled back. Surging US shale oil production has resulted in a big jump in oil inventories to a record high level, causing the price to tumble. The current average 45 cents per litre over-recovery on the petrol price means next month’s 39 cents jump in fuel levies could be offset.

If the rand strengthens further, it would help with declining inflation and possible interest rates, providing support to consumers. Companies focused on the domestic economy could benefit. SA bonds should also benefit, aided by a decreased likelihood of a ratings downgrade following the tough Budget and better growth outlook. If the rand retreats, rand-hedge shares should do well.

Global factors key

As usual it is global factors rather than domestic that will drive the currency, particularly commodity prices, sentiment towards emerging markets, and the outlook for American interest rates. Investor sentiment towards emerging markets continues to improve, as reflected by capital flows into bond and equity markets. The Federal Reserve is expected to hike interest rates this week. The important question therefore is whether the pace of hiking will pick up faster than expected over the coming year or two. The US economy added 235 000 jobs last month, a strong performance showing the economy no longer needs ultra-low interest rates. US long-term bond yields rose to 2.6%. The Fed will also start discussing how to shrink its $4trillion balance sheet soon. Until now, it has reinvested maturing bonds bought during its quantitative easing programme. The president of the European Central Bank (ECB) also noted that there was no longer any “urgency” to add additional stimulus as the European growth and inflation outlook improved. Although no rate increases are expected anytime soon, the market will start wondering when the ECB eases up its bond-buying programme.

Therefore, being appropriately diversified is important. At the start of 2016, investors may have been tempted to be fully invested offshore (the rand was collapsing and a downgrade seemed imminent). But South African bonds were the best performing local asset class. Markets are simply unpredictable. Just as it would’ve been a bad idea to get carried away with the bad news then, one shouldn’t get carried away with good news from the global economy now. There are still risks, notably unpredictability in US fiscal and trade policy, while the era of large-scale central bank stimulus is slowly coming to an end. Diversification remains key.

Chart 1: Global and local economic growth

Source: OECD and StatsSA

Chart 2: Brent crude oil, US dollars per barrel

Source: Datastream