President Trump – the next step in global disestablishmentarianism

Sanisha Packirisamy, Economist at Momentum.

Herman van Papendorp, Head of Asset Allocation at Momentum.

The shock outcome to the US presidential race has roiled global financial markets.

Initial market reaction to the Trump presidency

At the time of writing, S&P futures were down around 2%, while the Japanese Nikkei lost 5.4%. The Mexican peso, which has acted as a barometer for a Trump win in the US elections, plummeted around 8%, with losses extending to a wider range of emerging market (EM) currencies. Asset classes traditionally viewed as safe-havens were bid higher. The spot price of gold rose 2.3%, while the Japanese yen gained 2.1%. Similarly, US bond yields dropped initially on a flight-to-quality trade, but later retraced on fiscal worries.

The US people have spoken – out with mainstream policies

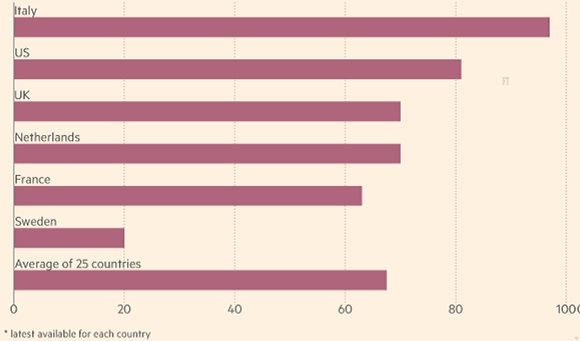

Almost by stealth in recent years, there has been a gradual, but accelerating, build up in the discontent felt by large sections of global developed market (DM) populations about their poor and deteriorating economic circumstances. In this regard, it is telling that an overwhelming majority of DM households have experienced no improvement in their real income levels over the past decade (see chart 1). According to the Financial Times, the US has the highest inequality of any high-income country and has seen the fastest rise in inequality among the seven leading high-income economies. US inequality has worsened considerably over time, with the total income share of the top 1% in pre-tax income surging from 10% in 1980 to 18% more recently.

Chart 1: Percentage of DM households with flat or falling real incomes, 2005-2012/14*

Source: Financial Times Page 2 of 3

So far in 2016, this discontent reality has culminated in two monumental political events where rich country voters have rejected mainstream policies in favour of previously unthinkable alternatives. First came the Brexit referendum vote in June 2016, where Britain surprisingly decided to leave the European Union. Then today the America people elected the anti-establishment candidate Donald Trump as the 45th US President with an implicit mandate to change the policy status quo. And this trend is likely to continue in coming years, with a plethora of political events scheduled to take place in Europe, where broad voter bases that feel deeply disenfranchised by the incumbent system could express their dissatisfaction tangibly by voting in an unconventional way (see chart 2).

Chart 2: Calendar of European political risk events

Source: RMB Morgan Stanley, Momentum Investments

The broad investment implications of disestablishmentarianism…

One of the main results of the escalating discontent among the voter bases of developed countries has been the rise of nationalistic tendencies at the expense of internationalism as voters increasingly deem the former to be more beneficial to their self-interest. As a result, protectionist policy thinking has gained rapid ground around the world. Should protectionism be widely implemented globally through high tariff barriers, world-wide price structures would inevitably rise, eroding real returns from asset classes in general, and inflation-sensitive assets like vanilla bonds in particular. In contrast, the relative attractiveness of inflation-protected securities that guarantee real returns would rise.

As emerging markets (EM) have arguably been the biggest beneficiaries of the globalisation trend, gaining from the free flow of trade and capital into its economies, it stands to reason that a global reversal towards protectionist policies would hurt this region’s trend growth the most. However, with DMs increasingly reliant on EM populations for cross-subsidising its own growth performance, DM growth is also likely to suffer from protectionism. The resultant lower aggregate global corporate top-line growth will inevitably have a negative bearing on equity market and corporate bond performance, in our view. While South African equities are unlikely to escape the negative global impact of rising protectionism, the reality that a dominant part of the market is positively geared to a likely simultaneously falling local currency, should provide some offset for the asset class.

Should such a fundamental transition from globalisation to protectionism indeed take place in coming years, it is likely to be accompanied by increasing uncertainty and hence volatility in financial markets.

…and more specifically of Trumpgate

We expect a short-term negative impact on EM asset classes in response to a rise in risk aversion. Although many of Mr Trump’s economic policies have not been clearly defined, the ones he has outlined suggest increased vulnerability for EMs as US self-interest could dominate, with the advent of anti-trade and anti-immigration policies harming EMs that are dependent on trade with the US.

Mr Trump’s declared inward focus on US domestic stimulus, which is likely to incorporate massive transport infrastructure spend, as well as corporate and personal income tax cuts, should provide some focused support for construction and consumer related industries within the US, but its fiscal implications could be negative for the US sovereign bond market.

While the full geopolitical ramifications are difficult to assess at this early stage, a full implementation of Mr Trump’s proposed changes to trade policies could result in a more isolated US economy as cross-border trade and immigration moderates. If the economy backtracks on prior globalisation gains, overall growth prospects could weaken for the US economy, leading to capped gains on average American incomes. Given Mr Trump’s strong criticism of the North American Free Trade Agreement (NAFTA - which has been in effect since January 1994 and nearly eliminated tariffs between Mexico, Canada and the US), this could be renegotiated. Mr Trump has also been vocal on his view of currency manipulation by the Chinese and has proposed a 45% tariff on Chinese imports unless the renminbi is allowed to float freely. With China accounting for 15% of total traded goods in the US between January and September 2016, Sino-US tensions could have significant negative global trade implications.

Mr Trump has previously accused the US Federal Reserve (Fed) of being too political, expressing concerns that stock markets are in a bubble thanks to Fed policies keeping interest rates at ultra-low levels. Although increased uncertainty and volatility could derail a December interest rate hike scenario, Mr Trump’s earlier comments would imply that a more hawkish committee could replace the current Fed, particularly if an implementation of further tariffs raises the prospect of inflation. Fed chair Yellen’s four-year term expires in January 2018, but we cannot rule out an earlier departure, particularly given Mr Trump’s public criticisms.

Our clients to benefit from diversified and risk-robust portfolios

At Momentum Investments, our holistic outcome-based approach to investment ensures that we construct client portfolios in a diversified manner in order to minimise the potential detrimental impact that specific global or domestic events could have on aggregate investment returns. While parts of the investment universe will no doubt be adversely impacted by the global trend of disestablishmentarianism, other asset classes are likely to offer offsetting benefits. In addition, the incorporation of risk parameters in our strategic asset allocation process ensures that the drawdown risk within our investment portfolios is minimised over appropriate investment horizons. As always, we continuously aim to utilise opportunities to increase exposure to asset classes that are unfairly punished by risk events in striving to increase the long-term financial wellness of our clients.