Post-pandemic policy prognosis

Once again, the past week has brought the policy response to the Covid-19 pandemic into focus. This, as global confirmed cases inch towards 16 million (with actual, undetected cases likely to be several times more), and deaths towards 650 000.

A new game in town

Four years ago, the prominent economist Mohammad El-Erian wrote a book titled “The Only Game in Town”, referring to the outsized role central banks played in the post-financial crisis era. And while central banks in many economies have been aggressive and innovative in responding to the pandemic, fiscal policy (government spending and taxation measures) has finally stepped up, and in a big way.

Let’s start with some good news. The leaders of the member states of the European Union (EU) have agreed to a €750 billion recovery plan that is historic for a number of reasons.

One is the size of the package, which comes on top of what individual countries have committed to their own economies. However, the most important is the concept of fiscal solidarity. More than half of the proposed fund, €390 billion, will be in the form of grants to the hardest-hit countries, notably Italy. In other words, taxpayers across Europe, including the frugal Germans, Austrians and Dutch, will contribute to recovery efforts in Italy and elsewhere. The healthy supporting the sick, and the rich the poor.

This marks an important step towards building a stronger, more united Europe. For many years, the key weakness in Europe has been the existence of a single currency and monetary union, without fiscal resources to back it up. The European Central Bank could set policy for all countries, but there was no real fiscal stabilisation mechanism, which left the whole enterprise vulnerable, as we saw in 2011/12.

What is also historic about the deal is that the European Commission (the government of the EU) will issue AAA-rated bonds against its own €1 trillion budget to fund the grants, and also loan money to individual countries at competitive rates. Finally, it comes at a point in time when relations with the US are at a low and China is rising as a superpower. In the geopolitical context too, more European solidarity now is crucial.

US potential double-whammy

In the US, the latest policy news is worrying. A $600 per week pandemic unemployment benefit expires this week, and no replacement has been legislated. This means the US economy, which actually recovered quite strongly as lockdowns were lifted, faces the double-whammy of renewed layoffs due to the surge in virus cases, and the loss of support for affected workers.

There is no doubt that the improvement in economic activity in May and June was fuelled in part by the extraordinary fiscal stimulus, including a one-off $1200 cheque to most households, as well as the additional unemployment benefits and special loans and grants to businesses. True, most of the money has been saved, not spent, but it was sufficient to see overall household incomes rise, not fall, despite the economic calamity. Despite some early hiccups, the $3 trillion support package under the CARES Act largely did what it was meant to do. The gains are now at risk. Remember that almost 30 million workers are receiving some form of unemployment benefit, a significant portion of the 150 million people who had jobs pre-pandemic.

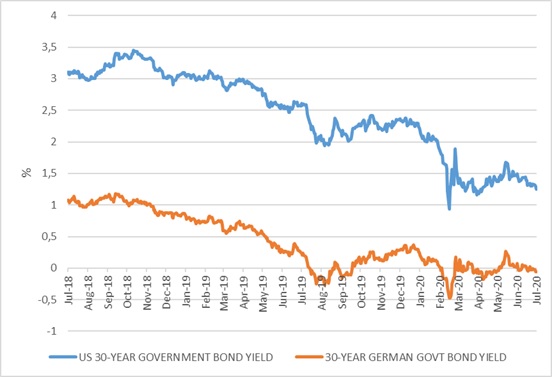

Chart 1: Long-term borrowing costs in Europe and America

Source: Refinitiv Datastream

Debt levels high, debt burden low

While US debt levels are surging, long-term borrowing rates are at record lows. The US government’s 30-year bonds are trading at a 1.3% yield. If inflation averages anywhere close to the Federal Reserve’s 2% target over the next 30 years, any new borrowing done now will essentially be free in real terms. In Europe, yields are even lower and therefore it makes sense for governments to borrow more. New debt pays for itself, so sustainability is not the problem.

The opposition is therefore largely political and ideological. In Europe, some of these stumbling blocks have been removed for now. In the US, with elections around the corner, there is a lot at stake politically. Republicans have always opposed an interventionist government role. But obstructionism as the economy recovers from the deepest recession in living memory might not play well at the polls in November. So there is hope for a further round of stimulus.

The South African government clearly cannot borrow cheaply, and it is hard to argue that new debt will pay for itself with local 30-year bonds trading at almost 12%. A high hurdle indeed, especially given the fierce debate raging over the size of ‘fiscal multipliers’, the amount of economic growth generated by each rand of fiscal spending (or simply, the bang-for-buck of fiscal spending). It is clear that substantial government spending over the past decade did not deliver faster growth, because the spending was poorly directed (to SOE bailouts and public sector pay rises).

The main game in town

While there has been some support from the fiscal side, as well as through the Unemployment Insurance Fund (which thankfully had a robust surplus going into the crisis), the SA Reserve Bank (SARB) is the main game in town as far as policy support is concerned. It is a role it has embraced reluctantly.

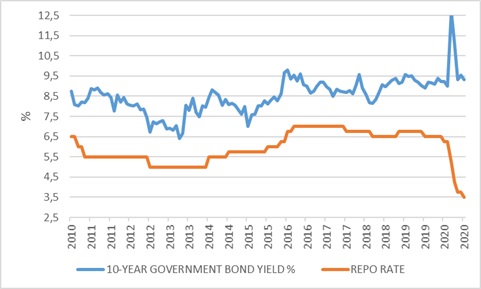

Chart 2: Short and long-term interest rates in South Africa

Source: Refinitiv Datastream

The 300 basis points in repo rate cuts since the start of the year, including another 25 last week, is not to be sneezed at, and the repo rate is now at 3.5%, the lowest level since it was first employed as a policy tool in 1998. But this has to be seen against the backdrop of the worst economic shock in living memory. The SARB’s own forecast sees a 7.3% economic contraction this year and a 3.7% rebound next year. The economy will still be smaller with far fewer jobs at the end of 2021 than it was in 2019.

Inflation not a concern

Inflation is not a concern now, nor should it be. Consumer inflation fell to a 15-year low of 2.1% in May. While this number should be taken with a pinch of salt, given that lockdowns distort some prices (with tobacco and alcohol not for sale, 6% of the total basket), there is no denying that the economy faces a massive deflationary shock. Incomes are falling, and this has to put downward pressure on prices. Price increases that are not subject to market forces – most notably and notoriously, Eskom’s tariffs – can push up the headline index in the short term, but are ultimately deflationary.

Unless incomes are rising strongly, consumers will either have to reduce electricity usage or cut spending elsewhere while electricity tariffs continue to rise in defiance of all logic. The same applies to fuel prices that have recovered somewhat after the rout in the global oil market. The petrol price is on course for a 16 cents per litre increase next week, but more expensive petrol only gives rise to sustained higher inflation if companies raise their selling prices to offset higher input costs. Doing so in this climate means chasing away customers.

A big component of the CPI basket – 15% in total – is rents. Rents are surveyed quarterly, and we’ll get the new June numbers this week, too late to be included in the SARB’s forecast. While there might be some new demand for residential property as more people work from home, it is extremely hard to imagine landlords pushing for rental increases given widespread job and income losses among tenants. In fact, rents are more likely to fall.

The SARB forecast is that inflation will average 3.4% in 2020 and 4.3% for 2021. This is not only below the midpoint of the 3% to 6% target range, but also means that the real repo rate – the effective policy stance – could end the year in flat to positive territory and then only turn negative next year if the economy recovers and inflation rises somewhat. This is precisely the wrong way round. Other countries have pushed real rates below zero.

There is therefore more scope for rate cuts, and the SARB’s forecast model points to one more 25 basis points cut in the fourth quarter, though this is not a given, since two of the five MPC members voted to keep rates unchanged last week.

More bond purchases to nudge longer-term interest rates lower should also be considered. The reason is not to fully monetise government’s deficit, but rather to ease overall financial conditions. The difference between short and long-term interest rates remains as wide as it’s ever been, known as a steep yield curve. It means that banks have every incentive to just earn a return by sitting in long bonds rather than lending out into the real economy. No surprise then that local bank holdings of government bonds has doubled as a portion of total assets in the past six years.

Currency considerations

The currency has always been an important consideration for the Reserve Bank, and one of the arguments against more aggressive bond buying is that it would weaken the exchange rate by increasing the money supply. But it could just as easily cause the rand to strengthen if foreign capital flows in to invest alongside SARB. So far, the R25 billion worth of bond purchases has coincided with the rand strengthening from bombed-out levels. At any rate, firefighters shouldn’t worry about getting the place wet.

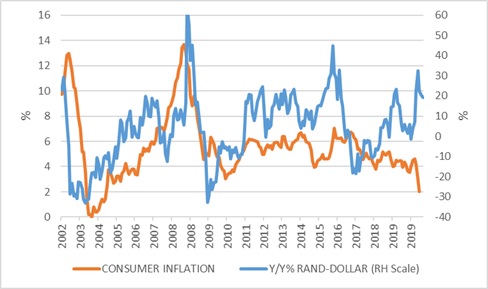

Chart 3: Local inflation and change in the exchange rate

Source: Refinitiv Datastream

It is also notable that when South Africa last had 2% inflation in 2004, it was due to a very strong currency. The fact that we have 2% inflation today with the currency still quite weak (it averaged R18 per dollar in May) tells you that the exchange rate has less influence on inflation than in the past. The same reasoning applies to fuel prices and electricity tariffs: a weaker rand only results in sustained higher inflation to the extent that retailers and other firms can pass the costs on to consumers. When demand is weak, it is difficult to do so. Low global inflation also plays a role. If the rand does appreciate, retailers might use the opportunity to raise margins again, and not pass on the savings to customers. This will only work if you are not undercut by your competitors, of course.

For what it’s worth, the Reserve Bank’s forecasts include an assumption of an exchange rate that starts at R17.93 to the dollar and barely recovers over the next two years. In other words, it is a conservative assumption. After all, we are starting to see signs of the US dollar coming under pressure. The policy developments noted above have been positive for the euro and negative for the greenback.

Ultimately, it is the dollar, commodity prices and global risk appetite that will determine what happens to the rand. If the stars do align for a weaker dollar – and it is only an ‘if’ – we should see the rand firming. How would the SARB react? It would certainly place some downward pressure on inflation and create more room for rate cuts as well as more bond purchases.

The more intriguing question, rarely asked these days, is if the SARB should prevent an appreciation and shore up its foreign exchange reserves. Though it is unlikely to say so out loud, the SARB’s low level of foreign exchange reserves relative to overall foreign debt in the economy is one of the reasons global investors look askance at South Africa, or at least the ones we’ve spoken to. Gross forex reserves have remained more or less unchanged over the past decade, at around $52 billion.

Ultimately, while we as investors can suggest what we think policy should be, we need to invest according to what it is now and how it is likely to evolve. Two things remain clear: real interest rates in developed countries are likely to remain in negative territory for some time, while locally shorter-term rates are still positive in real terms and longer-term rates very high. It still makes sense to earn interest income locally and not globally.