Possible outcomes from the 2019 National General Elections and potential impact on markets

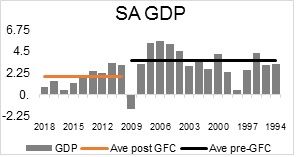

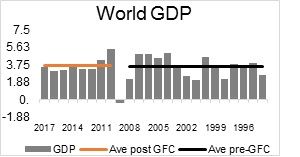

South Africa will be going to the polls on Wednesday the 8th May for the sixth time since the first democratic elections in 1994 and the outcome of these elections could have a pronounced impact on markets. Why is this time different you may ask? From an economic perspective South Africa has been on a slippery slope for the last decade, with real Gross Domestic Growth (GDP) averaging below 2% per year since the Global Financial Crisis (GFC), whereas growth averaged 3.6% prior to the GFC. Compare this to world real GDP growth of 3.7% post GFC and 3.6% pre-GFC it is not hard to see that South Africa has fallen behind. Against other Emerging Market (EM) economies we have weakened even more, with EM growth averaging 5.5% both pre-and post GFC

.

.

There are multiple reasons for this deterioration, but without any doubt a lack of structural reform to boost growth is one of the main culprits. The effect of sub-par growth can be clearly seen in the unemployment rate (over 27% and considerably higher amongst youth) as well as South Africa’s deteriorating fiscal deficit. This in turn has caused us to lose our investment grade credit rating from Standard & Poor as well as Fitch, with only Moody’s giving us the benefit of the doubt currently. Although, they too may cut us to non-investment grade if signs of improvement are absent. All these negative hits to our economy have had a detrimental effect on confidence and trust and this, in turn has prevented corporates from investing in the economy. A favorable election outcome has the possibility to attract capital back into the economy and improve overall confidence. Therefore the election on the 8th May is so important for the country.

The table below illustrates the past outcomes of the 2014 General Elections, the 2016 Municipal Elections, as well as the most recent IPSOS and IRR poll predictions:

|

|

ANC |

DA |

EFF |

|

2014 General Election |

62.1 |

22.2 |

6.3 |

|

2016 Municipal Election |

53.9 |

26.9 |

8.2 |

|

IPSOS |

61 |

19 |

11 |

|

IRR |

51 |

24 |

14 |

To formulate our roadmap we look at scenarios where the ANC does better or worse than the previous 2016 election.

However, what is also important to monitor are the Provincial outcomes. Gauteng is an important province because it represents 35% of the country’s GDP and 25% of the country’s population. A loss of below 50% for the ANC would lead to a coalition which would not be ideal as decisions and implementation may be compromised.

Below we consider a range of different scenarios and the potential impact on financial markets:

Scenario 1: ANC wins 55-60%

This is probably the most likely outcome and we would put a 60% probability on this transpiring. The initial market reaction could be positive, however the provincial outcome should also be considered. As explained above a Gauteng loss of the ANC might be slightly negative. Overall the Governing party should feel that the deteriorating trend shown in the 2016 municipal election has reversed and that faith in the leadership has been restored. Under this scenario the President will have more weight to institute much needed structural reform. The appointment of the new Cabinet (expected at the end of May) would indicate his ability in this regard. The current cabinet ministers of 34 could be cut to under 30 under this scenario and many deputy ministers would be disposed of. The Rand could strengthen and SA Inc stocks should outperform the index. Bonds and Property could also do well under this scenario. Growth may get an initial boost from confidence, however more importantly longer-term trend growth should shift higher as reforms take shape. A rating downgrade by Moody’s could be avoided.

Scenario 2: ANC wins 50-55%:

We would put a 30% probability to this outcome. Clearly not as positive as the above scenario, but again very dependent on how the other parties do, as well as the Gauteng outcome. The perception would be that the President does not have a clear reform mandate and that a compromised outcome would hinder growth over the medium term. Initial market reaction could be negative, but again the new cabinet could be the main market mover by the end of May. If the cabinet confirms the compromise theory then risky assets could sell off with the Rand deteriorating. SA Inc stocks, bonds and property could be in for a tough period as well. A rating downgrade could follow. But you might still find a muddle along outcome depending on the cabinet structure. Certainly, an initial disappointment, but not an all fall down outcome.

Scenario 3: ANC wins < 50% or >65%:

These tail events would clearly have the biggest impact on markets. We ascribe a 5% probability on either outcome. Initially SA Inc risky assets could sell off meaningfully on either outcome. The theory behind this sell-off would be that a coalition-government would stall reforms, and that a ruling government with a two-thirds majority can change the constitution and even become complacent. Cash and rand hedges would be the only place of comfort to investors.

The above scenarios are guidelines for potential market movements, but as discussed provincial outcomes are important and further to that cabinet is key. It is therefore crucial for investors to stay invested through the cycle in a well-diversified portfolio and not to panic on wild shorter-term market swings.

The next important dates to watch out for would be:

|

8 May |

10 May |

25 May |

25-30May |

|

Elections |

Results |

Inauguration (Loftus) |

New Cabinet |