Out of recession

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

South Africa exited a short-lived technical recession after posting positive growth in the second quarter. Gross domestic product (GDP), a broad measure of economic activity, rebounded by 2.5% in real terms in the second quarter, after declining in the two prior consecutive quarters. This was better than the market expected.

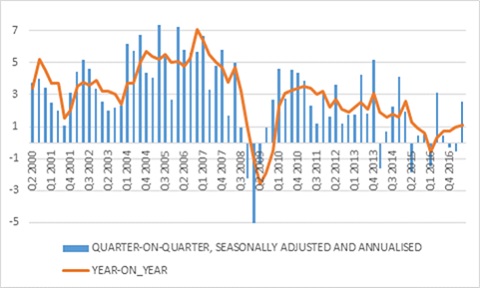

It appears that the worst is over for the domestic economy, barring any new shocks (such as another midnight Cabinet reshuffle, or more importantly, a substantial shift in global markets). Quarterly growth numbers can be volatile, so looking at annual numbers (i.e. comparing the second quarter of 2017 with the same quarter in 2016) can smooth the picture a bit. Year-on-year growth in real terms fell to -0.6% in the last quarter of 2016, the first decline since the 2009 global recession (see chart 1). This has now rebounded to 1.1% in the latest quarter and is still very disappointing in absolute terms, but an improvement nonetheless.

On sector level, the relatively small agricultural sector contributed 0.7% of the 2.5% growth, while finance and business services, the largest sector, contributed 0.5%. Since the substantial growth in agriculture is a rebound from the drought, it is not likely to be a repeatable performance. The biggest detractor in the previous quarter, the trade sector (wholesale, retail, vehicles, catering and accommodation) made a positive contribution in the second quarter.

Outlook for households

The economy-wide wage bill (which captures the number of employed times their earnings) grew by 7% year-on-year. With inflation now below 5%, this means that the household sector is enjoying fairly decent real income growth (wages account for around 70% of total household disposable income according to Reserve Bank data, with the remainder mostly made up of social grants, interest and dividend income). Since household borrowing growth is anaemic, real spending growth depends mostly on income growth and inflation. Real household consumption spending growth fell to 0.7% year-on-year in the first quarter, but improved to 1.5% in the second quarter.

Modestly lower interest rates also mean that a slightly smaller portion of income will have to be set aside for servicing debt. Households currently spend 9.5% per year of after-tax income on interest payments (these are averages for the entire economy, so the picture will clearly be different for each income segment and for individual households). Household consumption accounts for around 60% of domestic economic activity, and therefore a moderate improvement should support economic growth in the coming quarters.

Fixed investment contraction

The two main negatives from the GDP report relate to falling fixed investment spending and slow nominal growth. Fixed investment (technically known as gross fixed capital formation) declined by 1% in real terms compared to the second quarter of last year. About 60% of fixed investment spending is done by the private sector, with government and state-owned enterprises each responsible for roughly 20%. Government fixed investment spending – items like roads, clinics and schools – has accelerated, but spending by public corporations has declined off a high base. Private investment peaked in the final quarter of 2014 and has declined relentlessly since.

For private businesses to make a long-term investment decision - whether it is building a factory, buying new machinery, upgrading software or expanding their fleet of vehicles – requires a level of confidence in the future. Optimistic assumptions about future revenue growth can justify outlays, but with negative assumptions about the future, it makes sense to do something else with shareholders’ money. South African businesses have increasingly chosen to invest abroad, while investment in the domestic economy has contracted. When there is uncertainty over how government policy might evolve over time, this is also a huge hindrance to investment. A firm will not invest large amounts of money now only for the rules to change in a few years (the local mining sector in particular has been hobbled by regulatory uncertainty).

Slower nominal growth a worry for the Budget

The second negative is slower nominal growth. While real growth has accelerated from negative levels to 1.1% on an annual basis over the past couple of quarters, nominal growth averaged 7.5% from 2013 to 2016, but only 6% this year. Seen from this point of view, the improvement in real growth was due mostly to lower inflation, rather than a big jump in economic activity. Economists usually focus on real growth (i.e. growth after inflation) as this is a better indicator of whether living standards are rising. Similarly, individuals should think of investment returns in real terms, since growth in purchasing power is what counts. But sometimes nominal (i.e. before inflation) variables are important. Notably, government’s budget and tax collection is measured in nominal terms. In other words, the government doesn’t mind a bit of inflation as it can increase tax revenue (though it usually compensates individual tax payers for the impact of higher inflation by giving relief for bracket creep).

In its February Budget forecast, National Treasury assumed nominal GDP growth would average 8% over the next three years. In other words, growth is likely to be much lower than expected, and therefore tax revenue will probably undershoot its target materially. The Budget set out an aim of reducing the deficit from 3.4% to 2.8% of GDP over the next three years. The new Finance Minister will have to pull out all the stops to prevent the deficit from rising in the current year, and then to still decline in the outer years. If taxes are increased too aggressively (or spending cuts too sharply), it risks hurting economic growth, which will make matters worse. It will therefore require a very delicate balancing act and great emphasis on making sure every rand is spent exactly as intended.

External environment still supportive

Lifting economic growth on a sustained basis will require structural changes in the economy (more competition, more flexible labour markets, less red tape, tackling infrastructure bottlenecks) and greater certainty on policy. Investors will look to Finance Minister Gigaba to make announcements on this score in the October mini-Budget, but expectations are low. In the meantime, the economy should benefit on a cyclical basis from a supportive external environment, with firm global growth and low inflation (for instance, the European Central Bank last week upgraded its growth forecast but reduced its inflation forecast for the next three years).

In particular, the softer US dollar - which fell to the lowest level since January 2015 on a trade-weighted basis - benefits emerging markets and supports commodity prices. Gold is at the best level in almost a year and platinum moved above $1000/oz for the first time since March. Firmer commodity prices in turn help the local mining industry and also the country’s balance of payments. The weaker dollar reduces the risk of holding emerging market bonds (such as South Africa’s) while low global yields, which reflect a subdued inflation and interest rate outlook, make high yielding emerging market bonds attractive (the 10-year US Treasury yield fell to almost 2% last week, the lowest level since the November elections). As a result, foreigners are still enthusiastic buyers of our bonds, keeping local yields in check despite the credit ratings downgrades and political uncertainty.

Chart 1: South African real gross domestic product growth,%

Source: StatsSA

Chart 2: Gold, platinum and iron ore prices

Source: Datastream

Chart 3: Trade-weighted US dollar

Source: Datastream