Nigerian economy hurt by slump in oil price and political challenges

M Buhari, elected as the new Nigerian president in April 2015, announced in June that the nomination of his cabinet will be delayed until September 2015. Hopes created by the change at the head of the country earlier this year could be dashed by the postponing of decisions and actions.

A clear policy and quick measures are needed to tackle the consequences of lower oil prices. The Nigerian economy is driven by the oil sector (about 10% of GDP) and oil accounts for 70% of fiscal and 90% of exports revenues. The fall in the oil price represents a loss of revenues for the budget and foreign currency earnings. To preserve its reserves, the central bank (CBN) put in place restrictions in June on access to foreign currencies for the import of a limited number of goods.

This may prove insufficient if downward pressures on the naira continue, which may be reinforced by political uncertainties. The top priority of M. Buhari is the fight against corruption. One of his first decisions as a president was to dissolve the board of the national oil company (NNPC) under suspicions of financial misappropriation.

The main argument for postponing the appointment of a new government was to ensure the credibility and integrity of ministers. But concerns are growing regarding M. Buhari’s ability to deal with the current economic difficulties and also enforce quick structural reforms.

Risks

The new president is facing a difficult and deteriorating economic environment and needs to deal with major short-term and medium-long term challenges, which need prompt decisions and rapid enforcement.

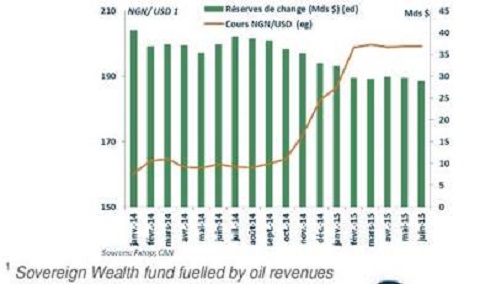

Short term economic challenges: high pressure on the naira exchange rate and on foreign reserves.

• The naira has depreciated nearly 20% in a year. The government devaluated the currency in November 2014 and February 2015 but downward pressures on the currency remains high. The gap between the official rate (197 NGN/ $) and the non-official one (242 NGN/$) in mid-July 2015 remains high. An additional devaluation cannot be excluded.

• Due to low oil prices, foreign currency reserves (including the Excess Crude Account1-ECA) are down by more than 20% in the year to July 2015, to $29-billion (about four months of import).

In order to limit the decrease in external reserves and stabilise the naira (and also encourage local production), the CBN took measures in June preventing access to foreign-exchange market for importers of some 40 goods and services (including rice, cement, textiles, furniture and the purchase of Eurobonds, foreign-currency bonds and shares). Imports of those items paid on importers’ funds, without resorting to foreign-exchange markets, remain possible.

However, restrictions on buying hard currencies may make it difficult for some companies to pay their foreign suppliers. Lack of commodities on the Nigerian market may also fuel inflation and weigh on consumer demand and growth.

A tight budget situation: fiscal revenues are declining while spending cuts are difficult.

• The stagnation of production and the slump in the oil price is limiting revenues for the government.

• The decrease in fuel subsidies, eased by the context of lower oil price, could be a way to cut spending. But the Nigerian government announced early July that fuel subsidies will be maintained, at least for Q3 2015.

• Part of the ECA assets (about $2- billion) will be used by the federal government, state and local governments, to cover their debts.

This will reduce the already relatively thin financial cushion of foreign exchange reserves. Both budget deficit (2.5% of GDP forecasted for 2015) and public debt (11% of GDP) remain sustainable, but public finances constraints cast uncertainty over the financial ability of the government to make necessary investments to go on with reforms aiming at diversifying export and fiscal revenues.

Infrastructure investments (the country suffers from major disruptions in power and energy supply) are also needed, but public financing will be limited by budget spending restrictions while private financing may be discouraged by persistent political uncertainties and security instability in the North of the country.

Lack of clear policy and the postponement of economic or political decisions would be a major source of uncertainty for foreign investors, as for Nigerian ones.

The lack of responsiveness of the new president may disappoint both foreign investors and the Nigerian population after hopes arising after his election. G. Jonathan, the former president was blamed for his poor results in terms of economic growth, unemployment, the fight against corruption and his inability to deal with attacks of Boko Haram. M. Buhari’s challenges are the same in a deteriorating economic context, decreasing fiscal revenues, making it more difficult to tackle structural reforms.