More political shocks

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Some 50 years ago, British Prime Minister Harold Wilson coined the expression ‘a week is a long time in politics’. Faced with chaotic Brexit negotiations, backstabbing Tories and two Cabinet ministers resigning amid this scandal, current British Prime Minister Theresa May no doubt feels the same. In Zimbabwe, where the political situation under Robert Mugabe seemed immovable for so long, change has been unfolding rapidly since the army seized control last week. Unlike in 2000, when the troubles in our northern neighbour exerted strong pressure on the currency, the rand barely moved on the news of this ‘coup’.

But political uncertainty remains elevated in South Africa too, and the weeks leading up to and following the ANC’s December conference might well feel like a lifetime. The uncertainty may unfortunately persist long after the conference if, for instance, the outcome is challenged in court, or different factions end up leading the party and the state.

Fiscal credibility at risk

The resignation of Treasury’s budget chief, who reportedly baulked at being forced to find additional funds for free university education, was a shock for markets. While a noble goal, introducing free higher education now would be at odds with the Heher Commission’s findings. It would also occur outside the normal budgeting process that has gained Treasury international credibility over the past two decades.

Eskom’s precarious financial position is also troubling. Apart from the fact that the economy cannot function without electricity, Government’s guarantee of Eskom’s debt means taxpayers are ultimately on the hook. Eskom is too big to fail, but it might be too big to bail out too. The ratings agencies have long fretted about this, and South Africa’s investment grade rating on local currency debt hangs by a thin thread. Adding pressure is the apparent decline in tax compliance as a result of leadership shuffles and allegations of corrupt activities at SARS, one of the country’s key economic institutions. Ideally, the agencies would wait to assess the outcome of the December conference – leadership and policy changes could be significant – before deciding, but that is unlikely. In other words, downgrade announcements by S&P Global and Moody’s on Friday will come as no surprise.

Markets are moved by surprises, and a potential drop to junk status should therefore already be largely priced in. Since it will lead to exclusion from the two main global bond indices, funds that track these indices will have to sell government bonds within a predetermined period, but the size of the likely outflow is not clear. There is still a huge pool of capital willing to buy junk status sovereign bonds if the price is right, and they could step in. South African pension funds have also held historically low bond allocations and could increase exposure. The immediate risk is therefore not that Government will be unable to fund itself, but rather that the cost of funding increases will hurt investors. (Bond prices and yields move in opposite directions.)

Global conditions are key

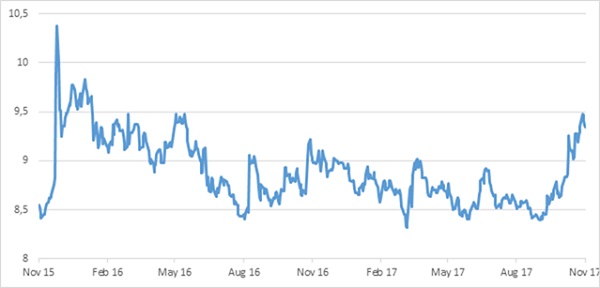

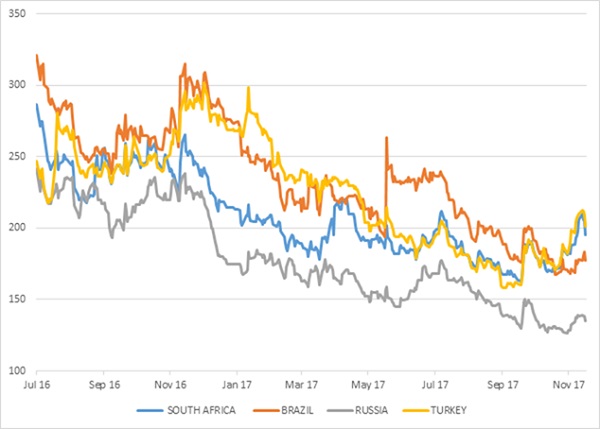

The latest political uncertainty occurred with emerging market assets still under pressure from the firming of the US dollar since September and the rise in US bond yields in anticipation of both higher interest rates and a boost to the economy from planned tax cuts. Along with South Africa, Brazil and Turkey have also seen bond yields rise. South African bonds offer long-term investors attractive value at these levels, but the short-term outlook is very uncertain. Credit default swaps (insurance against defaults on dollar debt, with higher value indicating higher risk) increased sharply since September, but remain lower than at the start of the year. South Africa’s relative position and our CDS have increased to be on par with Turkey, which is two notches into junk status. The market no longer sees us as investment grade, regardless of what the ratings agencies decide.

But the overall backdrop remains favourable for emerging markets, including South Africa. The world economy finally seems to be firing on all cylinders and forecasts are being upgraded, not downgraded. The biggest risk to the synchronised global expansion is probably from two sources:

If central banks, especially the Federal Reserve, overreact to signs of rising inflation and hike interest rates too quickly, it could spook markets and hurt growth. But it is more likely that interest rates will raise gradually as inflation remains well behaved.

The other main risk, especially for emerging markets, is that China’s economy experiences a sharp slowdown in growth. Last week’s economic activity numbers disappointed markets, especially commodities, but growth remains robust. Here too the key word is gradual. It is widely expected that China’s breakneck growth rate cannot continue indefinitely, and will slow over time as the economy shifts from a production to consumption focus. The problem is that the vast amount of debt that has been propping up growth rates could destabilise the economy. But even as overall economic growth cools, some sectors can still accelerate. Tencent reported 61% revenue growth over the 12 months to the end of September, a staggering growth rate for what is already a massive company.

Emerging market economies are also in better shape, generally speaking, especially those countries that were hammered by declining commodity prices and ran huge current account deficits. Commodity prices are off their 2015 lows, deficits have been narrowed, currencies have stabilised and inflation has come down.

Oil and rand double whammy

The weakening rand over the past two months, combined with higher global oil prices, will result in another steep petrol price hike in December. OPEC producers have been unusually good at sticking to agreed production cuts, while American shale producers are increasingly focusing on maintaining profitability rather than increasing output at all costs. Saudi Arabia has also had its share of political intrigue, with the arrest of several prominent politicians and businessmen. The petrol price increase will raise the inflation profile somewhat, with petrol being 4.6% of the consumer price index. But overall inflation remains subdued, providing support to consumers.

Retail sales rose 5.4% in real terms from a year ago in September, and 2% during the third quarter. Like mining and manufacturing, retail should contribute positively to third quarter economic growth, which looks like it might be in the region of 2%. Part of the explanation for decent real growth is that the inflation rate at retailers has halved since the start of the year to 3.5% in September. (Remember that the consumer price index covers services, housing and transport in addition to the goods we purchase at shops, hence the discrepancy with retail inflation.) But in nominal terms, retail sales have also picked up to 8.7% year-on-year.

This is the good news. The bad news is that the Reserve Bank has probably missed its window to cut rates again, and therefore consumers should not expect further relief on this front. Despite inflation being within its target range – and expected to remain there - it is very unlikely to move next week, or at all, given the fiscal, ratings, political and external risks. Forward rate agreements (FRAs) are pricing in rate hikes instead of cuts within the next nine months, but this is probably overdoing it. It does, however, show how quickly market conditions can change and in turn influence the real economy. As with the rapid political changes, these can often not be foreseen. Therefore it is important to appropriately diversify your portfolio so that returns are not dependent only on the outcome of unpredictable events.

Chart 1: South African 10-year government bond yield, %

Source: Datastream

Chart 2: 5-year US dollar credit default swaps for selected emerging markets

Source: Datastream