MMI: Quarterly market and economic review

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of macro research at MMI Holdings.

A confluence of factors caused the rand to fall steeply during the final quarter of 2015.

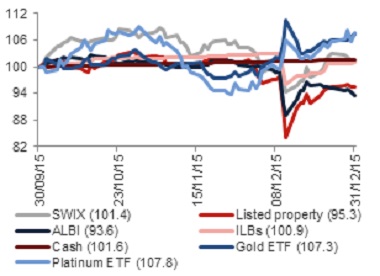

Plummeting rand driving asset class performance in 4Q15

Firstly, rising evidence of the inevitability of the first US rate hike in almost a decade, coupled with further easing measures in Europe and Japan, propelled the US dollar stronger in the quarter, with negative consequences for the currencies of commodity exporters with large current account deficits like South Africa (SA).

Furthermore, slowing domestic growth, culminating in negative credit ratings action by both Fitch and S&P in early-December, put additional pressure on the rand at the time. But the rand’s inherent vulnerability was fully exposed when SA changed finance ministers twice in the space of five days in December, derailing previous views that SA’s monetary (Reserve Bank) and fiscal (Treasury) institutions were above political meddling.

Chart 1: SA asset class performance in 4Q15 (indexed)

Source: INET BFA, Momentum Investments

The more than 10% rand decline against the US dollar during 4Q15 was clearly reflected in the relative performance of asset classes in the quarter. Unsurprisingly, the best performers were global assets, with global equities outperforming global bonds and cash. Among the local asset classes, rand weakness also assured outperformance from the gold and platinum ETFs, despite declining commodity prices during the quarter.

Domestic cash outperformed equities and ILBs during the quarter. Within equities, non-mining rand hedge shares strongly outperformed, reflected in the outperformance of Industrials (+6.6%) over Financials (-3.3%) and Resources (-19.2%). With rand weakness impacting negatively on inflation and interest rate expectations, local bonds (10-year yields up by 130 bps in the quarter) and listed property were by far the worst performers during 4Q15.

2016 again a year for full global investment exposure

We believe investors should maintain a full exposure to offshore assets in 2016, with the fundamentals and valuations of global equities looking far superior to those of global fixed income assets. Although there seems to be little to choose between developed market (DM) and emerging market (EM) equities on valuation grounds, we believe superior fundamentals for the former skew the risk-reward ratio meaningfully in favour of DM equities, particularly vis-à-vis commodity-exporting and current-account-deficit EMs. Within the DM equity space, the combination of positive macro-economic realities and preferable valuations support excess exposure to the European and Japanese equity markets, rather than to the US and UK.

Among SA asset classes, we believe the SA equity market’s valuation premium relative to its own history and other emerging markets is justified by the higher quality of its earnings base, as well as the supremacy of its management teams and corporate governance. In contrast to the opening up of a valuation discount in the SA bond market that has increased the attractiveness of this asset class, the huge valuation premium attached to local listed property constrains its prospective returns, in our view. On a risk-adjusted basis, returns from domestic cash look enticing to us in the near term.

Shallow and uneven global economic recovery

2016 is likely to be characterised by a further desynchronisation in growth and policy in major global economies. A sturdy growth outlook and stable inflation expectations will likely prompt central banks in the United States (US) and United Kingdom to nudge monetary policy rates higher from ultra-low levels, while significantly negative output gaps, fragile growth trajectories and benign inflation expectations point to the likelihood of the European Central Bank (ECB) and Bank of Japan (BoJ) maintaining an easing bias for time to come.

With US job creation averaging more than 220 000 per month in 2015 and headline unemployment dropping to 5%, a consumption-led recovery is expected to leave the world’s largest developed economy as the relative bright spot globally. This is in spite of sluggish global demand and a firm US dollar holding back a faster acceleration in export and investment growth. Domestic demand, services and residential construction have displayed resilience to weakness in global activity, suggesting that the US economy is on a firm-enough footing to gradually step away from ultra-accommodative monetary policy. Nevertheless, tighter monetary conditions from a stronger greenback, benign wage inflation and the threat of negative spillover effects from a bumpy global economic recovery suggest that US Federal Reserve (Fed) officials will move more cautiously than during past rate hiking cycles, which could keep the target federal funds rate below “normal” levels for quite some time.

In contrast, fresh ECB action in December 2015 was deemed necessary to spur price pressures and drive export growth higher in the Eurozone. Yet, even with this level of unprecedented easing, stimulus efforts only amount to roughly 15% of Eurozone GDP, much lower than the 25% of GDP stimulus previously induced by the likes of the Fed or the Bank of England (BoE). As a result, further easing measures may have to be announced in 2016 in the event of further disappointments in growth and inflation prints. Though GDP likely expanded at a reasonable 1.5% for the region as a whole in 2015, outside of Spain, activity remained disappointing in Germany and continued to lag in France and Italy. We expect a mild expansion in Eurozone growth to be carried by domestic demand in 2016 as low oil prices, a slow recovery in credit growth and easy monetary policy boost consumption spend, while a weaker euro continues to keep peripheral economies competitive. Near-term growth could also benefit from a rise in public expenditure in response to the rising number of asylum seekers, but intensified geopolitical risks remain a threat to trend growth in the longer run.

Whereas the recovery in developed markets continued to gain traction over 2015 (thanks to healing labour and credit markets and still-accommodative fiscal and monetary policy settings which supported firmer domestic demand), a deceleration in capital flows, pressured commodity prices and tepid growth in global trade drove a continued deceleration in growth in emerging economies to its lowest level since the global financial crisis. At an estimated 4.3%, 2015 growth in EMs printed well below the average observed over the early 2000s.

While rapid growth in the so-called BRIC nations (Brazil, Russia, India and China) had previously shored up global growth, given its sizeable c.30% contribution to world GDP, its synchronous deceleration since 2010 (with India being the exception due to robust investor sentiment and buoyant growth in real incomes) has contributed to the slowdown in other emerging economies. In a recent report, the World Bank highlighted the possible adverse effects on global GDP from a growth slowdown in BRIC. A 1% sustained decline in growth in BRIC could reduce economic activity in other EMs by around 0.8% and could shave nearly 0.4% off from overall global growth.

Lingering EM vulnerabilities suggest that challenging growth conditions are likely to persist. Domestically, depleted fiscal buffers, rising private sector leverage and waning productivity growth could limit the recovery in EMs in 2016, particularly as less favourable external financing conditions (see chart 2), a poor business climate and domestic policy tightening in key markets have reinforced obstacles to higher investment and growth.

Chart 2: Sharp slowdown in capital flows to EM ex-China

Source: Capital Economics, Momentum Investments

Rising interest rate prospects for the US imply tighter monetary conditions for emerging economies, particularly those running extended current account deficits and/or those sporting hefty dollar-debt burdens. While rising domestic interest rates on the back of potential currency weakness may attempt to partly negate the effect of declining portfolio flows, a weak growth backdrop may limit the extent of EM rate hikes, while higher inflation could push real rates lower.

Natural resource producers and economies with strong trade linkages to China have endured the hardest hit on growth. The latest (official) GDP data indicates that growth in the Asian behemoth lost momentum from the average 9.8% rate observed since 1980, to 6.9% more recently in 3Q15. The deceleration in growth proved to be most visible in sectors with considerable overcapacity, namely manufacturing and real estate, while activity in the consumption and services-related sectors held up reasonably well. Growth in China is likely to slow further over the next five years as Chinese officials implement their plan to reorient GDP to a more sustainable and balanced model. In an environment where China re-aligns its growth profile away from infrastructure and export-led GDP towards less trade-intensive consumption and services, we are unlikely to see commodity prices staging a sharp recovery. An overhang in the global supply of key commodities further points to little support for a significant reacceleration in commodity prices in the coming years.

Though there is a potential for India to take up China’s mantle as possibly the next dominant player in world commodity demand in the future, growth in India’s commodity consumption over the next ten years is unlikely to replicate the positive demand shock created by China over the past decade and a half. India’s current contribution to global commodity consumption remains a fraction of that of China’s. Furthermore, India’s democratic rule of law hinders a faster acceleration in the rollout of commodity-intensive infrastructure projects, thereby capping demand.

In this context, net commodity-exporting countries, particularly those facing large external imbalances, are likely to face a less favourable terms-of-trade trajectory, suppressing economic growth prospects over the next while. Furthermore, growth is likely to be least resilient to any negative shocks in those developing nations that have failed to address shortfalls in governance and labour markets through the implementation of structural reforms.

Lacklustre growth in SA faces mounting headwinds

Trend growth in SA has tumbled from its longer-term historical rate of above 3% to below 2% as the private sector refrains from embarking on substantial new fixed investment in light of muted global and domestic economic activity, binding energy constraints and heightened investor unease over domestic economic policy direction. Rising fiscal pressures, a dismal employment outlook and a dip in real wages are likely to inhibit a faster acceleration in consumption spend in 2016, while the export benefit of a weaker rand is likely to be curbed somewhat by fragile global trade activity and rising input costs.

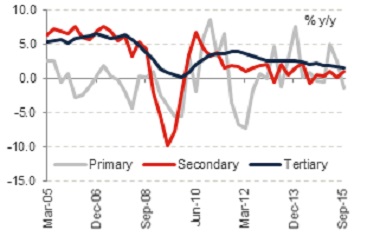

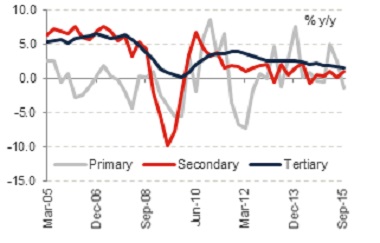

Consequently, real growth in SA is likely to continue underperforming our estimate of potential growth in 2016, expanding at a rate only marginally higher than 1.0%. Growth rates in SA’s primary and secondary sectors have been punctured by soft global commodity prices and subdued demand both globally and locally (see chart 3). Dry and hot weather conditions further threaten to shave off between 0.5% and 1.0% from GDP this year should agricultural volumes be hit in excess of 20%. Morgan Stanley estimates that the negative impact of the drought could further trim SA exports by around USD9.5 billion. As a result of lower domestic agricultural output, higher food imports are expected to partly negate the impact of slowing import demand as weak local demand and a higher rand price of foreign-produced goods curb consumer imports.

Chart 3: GDP headwinds intensifying outside tertiary sector

Source: Stats SA, Global Insight, Momentum Investments

Global investors withdrew USD52 billion from EM equity and bond funds in 3Q15 on rising risk aversion, registering the largest quarterly outflow on record. This has led to an increase in currency pressures for commodity exporters with large external deficits in particular, while idiosyncratic political and sovereign downgrade risks have aggravated SA currency moves.

Significant currency depreciation (and volatility) intensifies the possibility of an extended inflation breach despite the weaker currency pass-through observed in SA to date. The SA Reserve Bank (SARB) has warned that the recent convergence in medium-term inflation expectations (by analysts, firms and trade unions) at close to the upper end of the 3% - 6% inflation target band further threatens higher price setting in the economy. With inflation threatening to breach the upper target of 6% on average this year, we expect 75 basis points worth of rate rises over the course of 2016 to keep inflation expectations anchored and real policy rates in positive territory, particularly against the backdrop of further interest rate hikes by the Fed in response to firmer US growth.

A more benign structural growth outlook and shrinking fiscal buffers leave SA’s fiscal authorities with less room to manoeuver, jeopardising Treasury’s fiscal consolidation timeline and medium-term debt stabilisation plan. The nature of SA’s fiscal expenses remains highly structural. An escalating public service wage bill and rising debt-servicing costs have crowded out other forms of more beneficial growth-enhancing spend and remain a trigger for further negative sovereign ratings action towards sub-investment grade status.

Doubts around the direction of economic policy have discouraged inward investment. This limits trend growth and hence revenue collections on a more sustainable basis, restricting SA’s ability to grow its way out of a potential debt crisis in the absence of another commodity super-cycle.

Earlier student protests, the recent finance ministry debacle and inaction to reduce maladministration in SA’s state-owned corporations have raised concerns over government’s ability to deal with socio-political and economic challenges. Endorsing policy measures that could damage the investment climate could further taint SA’s investment grade status. If government does not react to growing fiscal risks in time, further expected cuts to longer-term capital expenditure in favour of current spend will exacerbate benign domestic growth projections, eventually forcing government debt ratios even higher. A larger debt burden, reduced sovereign creditworthiness and lower inward investment would perpetuate a poor growth environment, fuelling a weak growth-high debt spiral.