Missiles, hurricanes and other distracting headlines

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Hurricane Harvey slammed into Houston dumping an unimaginable amount of water on the Texan city. Apart from the unfolding human tragedy, the hurricane is expected to have a devastating impact on the region’s economy. The Houston metropolitan area is the fourth largest in the US, and its massive economy is even larger than South Africa’s. It is at the heart of the American oil and gas industry, and almost half the refining capacity in the US is located on the Gulf Coast. The city is also a key port for exports of other commodities, such as cotton and wheat.

Early estimates of the cost are in the region of $50 billion and likely to exceed that of most previous natural disasters. Rebuilding efforts after the flood will at least lead to a bump in spending and activity, but both the destruction and reconstruction impact needs to be seen in the context of a US economy that generates $18 trillion in output a year. There is no reason to believe that Hurricane Harvey will have a longer-term influence on overall US economic growth, which has been chugging along at around 2% per year. While this is one of the longest expansions on record at 32 quarters, it is also one of the slowest. There is no obvious sign of overheating anywhere, with inflation low (too low actually at 1.4%), wage growth steady at 2.5% and borrowing activity subdued. Interest rates should therefore remain benign - even as the debate rages as to whether the Federal Reserve will hike twice or three times this year – and the expansion can be sustained for longer.

In contrast, when Hurricane Katrina (still the most costly natural disaster in US history) hit in August 2005, the US housing market was close to peaking after a multi-year boom. The subsequent decline in house prices bankrupted hundreds of thousands of over-borrowed households, while the collapse in homebuilding activity cost almost two million jobs. But even more devastating was the entire industry of financial products built upon US mortgages, sliced and diced, repackaged and stuffed into portfolios worldwide. By 2007, these products and their derivatives had turned toxic and threatened to take down large parts of the global financial system. The economic toll was many times greater and more widespread than any natural disaster.

Storms of a different kind in Washington

Meanwhile, President Trump has revived three of his favourite positions, two of which would likely have negative consequences for markets. Firstly, the White House is making a renewed push for tax reform. This should be positive for company profits, but investors are no longer as enthusiastic about the prospect for speedy implementation. Secondly, he has threatened to veto the spending bill that Congress needs to pass before the end of the month, unless it contains funding for a wall on the Mexican border. A veto would shut down the Federal government and complicate negotiations around raising the debt ceiling. Thirdly, he has revived a push for import tariffs to protect American industry which, in a worst-case scenario, could lead to a trade war.

North Korea’s sabre rattling

Even worse than a trade war is an actual war. North Korea, seemingly worried that the world had forgotten about it amid the flooding in Texas and the latest White House controversies, fired a missile that flew over Japan and crashed into the Northern Pacific. Over the weekend it also tested a nuclear bomb. This rattled markets and sent safe-haven assets – the yen, gold and US Treasuries – higher. The US dollar, however, continues to weaken. The euro rose above $1.20 for the first time since early 2015. The strength of the euro has been the notable surprise of the year, given that many forecasts at the start of 2017 saw it heading in the other direction towards parity with the dollar. Instead, the euro has appreciated against the dollar by 13% since January. The main reason is that the European economy has picked up speed after years in the doldrums. But even here inflation and borrowing remains low. Meanwhile, European Central Bank President Mario Draghi’s comments at the recent Jackson Hole summit of central bankers were not seen to be sufficiently dovish to talk down the euro. The market clearly thinks that the ECB will pare back stimulus earlier than previously expected, while the US hiking cycle will be more gradual than expected. Both Draghi and Fed Chair Yellen, focused their Jackson Hole speeches on the importance of financial regulation rather than on monetary policy matters – precisely to prevent the sort of reckless lending that fuelled the financial crisis. While united on this matter, the move in the euro/dollar exchange rate creates a headache for Draghi, as it will suppress inflation while it will be cautiously welcomed by Yellen.

Soft dollar improves local interest rate outlook

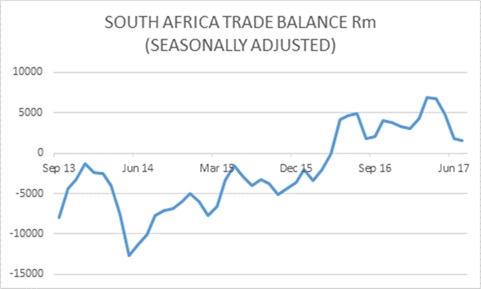

The softer dollar and firmer gold and platinum prices have seen the rand head back towards R13 per dollar. Since most of our imports are typically priced in dollars (especially oil and petroleum), it contains imported inflation (while a weaker rand against the euro should help exports to Europe and tourism from Europe). This should give our own central bank comfort that they can continue cutting interest rates. Producer inflation declined to 3.6% in July, while the economy posted another trade surplus in July, and the R36 billion surplus for the first seven months of the year, compared to a R4.7 billion deficit for the same period last year. This should help contain the current account deficit, one of the risk factors for the exchange rate. The economy certainly needs lower interest rates. Total bank lending growth slowed sharply to 5.3% in July, while it was growing by almost 9% at the start of the year.

Patience paying off for local investors

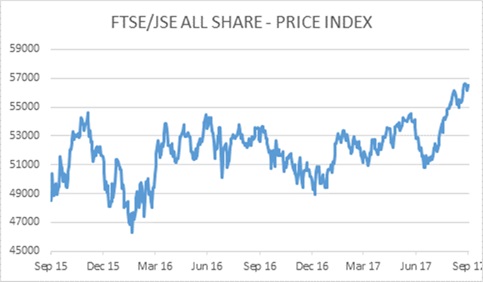

Largely shrugging off the developments in the US and North Korea, local markets had another solid month in August. The local market also outperformed global markets in the month: while the S&P 500 lost 1% in August, the FTSE/JSE All Share Index returned 2.6% in rand and more than 3% in US dollars.

Resources led the charge on the JSE, unsurprisingly, given gains in precious metals prices. The gold and platinum mining indices returned around 9% but the diversified heavyweights, Anglo American, Glencore and BHP Billiton, also performed well.

Financials returned 2% in August, with banks gaining 4% amid a rosier interest rate outlook. The big rand-hedge industrials were mixed in August. Richemont gained 3% and Naspers 1%, but British American Tobacco lost 1%, while Steinhoff, hit by fraud allegations, lost 4%.

Local bonds also had a good month, with the ALBI returning 1%. Listed property was basically flat in August and cash returned 0.5%.

With eight months of the year now over, 2017 returns are certainly much better than last year’s. Declining inflation means real returns are increasing. Local equity returns are in double digits, bonds and property are ahead of cash and global equity returns exceed the extent of rand appreciation (i.e. positive for local investors). This is despite all the political uncertainty, conflict and negative headlines both at home and abroad, showing once again that it pays to keep a cool head when investing.

Chart 1: FTSE/JSE All Share – Price Index

Chart 2: Gold Price $/OZ

Chart 3: South Africa trade balance RM (Seasonally adjusted)

Source: Datastream