Interest rate uncertainty

Traditionally, central banks have been thought of as staid, conservative institutions while most people found monetary policy, to be frank, a very boring topic.

However, not anymore. The billionaire Murdoch family, inspiration for the hit TV series Succession, recently announced a deal that effectively ended its own succession battle with oldest son Lachlan taking over control of News Corp and Fox. Perhaps the next boardroom TV drama will be set in the Federal Reserve’s headquarters.

Just days before last week’s scheduled meeting of its monetary policy body, the FOMC, it was still unclear who would attend. Governor Lisa Cook was fired by President Trump for allegedly being dishonest on a mortgage application, but she challenged the dismissal and a court ruled that she must remain in her role for now. Meanwhile, the senate confirmation process was rushed to get Stephen Miran, a Trump adviser, on the board just in time for him to vote. Trump has been pushing aggressively for the Fed to lower borrowing costs. In the end the drama was unnecessary. Cook joined the rest of the committee in voting for a 25-basis points rate cut. Miran voted for a 50-basis points reduction. However, Trump has applied to the Supreme Court to remove Cook. It seems unlikely that this appeal will succeed, but if it does, other Fed officials could also face removal. Regardless, Fed Chair Jerome Powell’s term expires in May and the race to replace him could be one of the most consequential in recent history.

Cut!

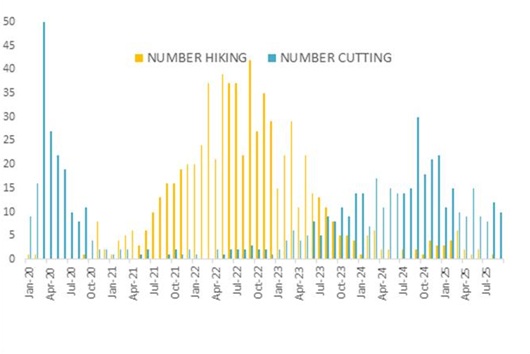

The 25-basis point reduction in the fed funds rate was expected and means the Fed joins many other central banks in resuming its cutting cycle. The bigger question is how far and how deep this cycle goes. It will have implications for investors all over the world, since the Fed is still the most important central bank.

Chart 1: Number of central banks cutting or hiking each month

Source: cbrates.com

Central banks can lower interest rates for good or bad reasons. A “good” cut would be when inflation is falling or is expected to fall and high interest rates are no longer needed. This is sometimes characterised as a soft landing since the economy did not buckle under the weight of high interest rates but can now benefit from lower borrowing costs. This scenario is normally beneficial to bond and equity markets. A “bad” reason is when the economy is headed for recession and in need of emergency support. Such emergency rate cuts would help bonds but usually not equities, as investors would worry about the impact of a recession on profits. Indeed, equity bear markets usually coincide with recessions.

If we take recent US interest rate cycles as an example, the 2019 pivot was a “good” cut, while the plunge in rates in 2020 was “bad” since it was a response to the Covid economic shutdown. The 2024 reductions fall into the good camp again, since inflation had come way down while the economy remained resilient - a soft landing. Last week’s rate cut falls in between, making it less straightforward to interpret. Even Chair Powell acknowledged this in the press conference, noting that it’s “challenging to know what to do”. Part of the problem is that the Fed, unlike most other central banks, has a dual mandate: stable prices and maximum employment. The twin objectives are pulling in different directions.

Inflation has been rising recently, moving away from the 2% target. Some of this is due to import tariffs and is likely to be once off. However, there are signs of sticky inflation in areas where tariffs should have no direct impact, such as non-housing services. The last thing the Fed wants to see is unaffected companies raising prices and blaming it on tariffs.

Moderating growth

On the other hand, economic growth has moderated and job creation is stalling. This too is partly tariff related, with the massive uncertainty around trade policies probably resulting in firms postponing hiring decisions. Companies could also be experimenting with artificial intelligence to see if they can get away without adding staff. The unemployment rate remains low at 4.5%, however, partly due to the fact that labour supply has shrunk, with more than a million immigrant workers leaving the workforce since the start of the year.

Click here to read more...