Inflation slows towards top end of target band

Sanisha Packirisamy, Economist at Momentum.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Sanisha Packirisamy, Economist, and Herman van Papendorp, Head of Asset Allocation at Momentum discuss the country’s inflation in relation to targets.

Headline inflation broadly in line with expectations

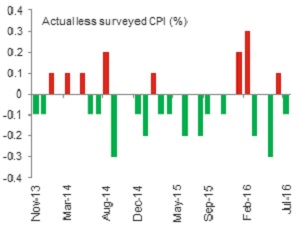

Headline consumer price inflation (CPI) dipped to 6.0% y/y in July 2016 from 6.3% y/y in June, in line with our own estimate and marginally lower than the Bloomberg median expectation (see chart 1). The 0.8% monthly rise in inflation was largely the result of an increase in water/municipal rates and electricity tariffs which rose by 8.1% m/m and 7.4% m/m, respectively.

Chart 1: Headline CPI broadly in line with market expectations

Source: Stats SA, Bloomberg, Momentum Investments

Aside from electricity and municipal (including water, assessment rates, refuse collection and sewerage collection) tariffs being surveyed this time around (accounting for 15% of the consumer basket), an additional 21% of the basket is surveyed every July. Although building and household content insurance is surveyed in July, the monthly figures show a slight decline in insurance costs for the month.

Relative to our own forecasts, prices of alcohol, tobacco, household appliances and vehicles surprised marginally to the upside, while personal care, funeral costs and electricity prices (Eskom had previously been granted a 9.4% increase) increased by less than expected.

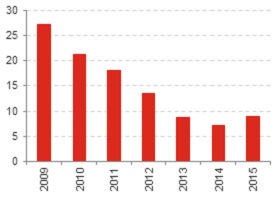

Court overturns energy regulator’s decision on Eskom tariff hikes

The High Court in Johannesburg recently set aside the National Energy Regulator of SA’s (Nersa) decision to grant Eskom an effective 9.4% tariff increase for 2016. The ruling was based on Eskom failing to follow the correct methodology when requesting the tariff increase for 2016 based on the Revenue Clearing Account (RCA), including submitting late and not submitting quarterly reports.

According to RMB Morgan Stanley, this results in customers being overcharged by around 6%. Options include adjusting tariffs lower this year or a downward adjustment to their 2017 application given that the increase was already implemented and surveyed by Stats SA in the July 2016 print. RMB Morgan Stanley estimates that a 10% (upward) adjustment to electricity prices adds 0.35% to annual CPI and reduces overall GDP growth by around 0.2%. Macquarie highlights that a likely appeal form either Nersa or Eskom could lead to the tariff increase been reinstated next year, in addition to the tariff increase that would come about in response to the RCA application that Eskom still needs to put forward later this year.

Chart 2: Recent annual electricity increases (% y/y)

Source: Stats SA, Global Insight, Momentum Investments

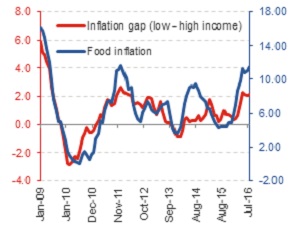

High food prices still behind the sizeable gap in inflation between low- and high-income earners

Since 2009, the inflation gap between high-income earners (classified as earning over R79 153 p.a. by Stats SA) and low-income earners (earning up to R14 564 p.a.) has averaged 0.8%. This is likely partly owing to food inflation averaging 6.6% over the same time period (see chart 3). Given that low-income earners spend over 35% of their consumer basket on food, high food prices impacts this end of the income-earning spectrum far more than higher-income earners who spend less than 10% of their basket on food costs. The recent rise in food inflation to 11.5% y/y in July has led to the inflation differential between these two income-earning categories remaining sizeable.

Chart 3: Elevated food prices drive inflation higher for low-income earners

Source: Stats SA, Global Insight, Momentum Investments

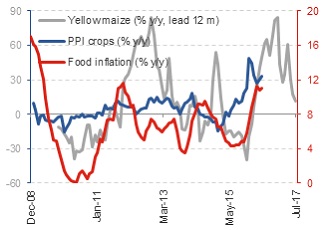

Within the food category, bread/cereal and meat prices saw the steepest increase in July (3.8% m/m and 2.1% m/m, respectively), followed by vegetable prices (1.8% y/y). Live animal prices tracked at the producer price level increased to 7.2% y/y in June from 5.5% y/y in May, indicating that meat prices could lift further in upcoming months.

Although crop prices at the producer level remained elevated at 33.3% y/y (June print), the recent sharp pullback in (rand) yellow maize prices (see chart 4) suggests a meaningful reversal in food inflation in 2017, alleviating pressure on lower-income earners.

Chart 4: Expecting a reversal in food inflation in 2017

Source: Stats SA, Global Insight, Momentum Investments (food inflation = right axis)

Petrol prices to dip in next two inflation readings

A 99c/l drop in the Gauteng 95 petrol price in August and the current 41c/l over-recovery in the petrol price for September should see annual private transport inflation (including petrol) remain in negative territory for the next two inflation readings. We expect a gradual drift higher in international oil prices from an estimated average of USD45/bbl in 2016 to USD55/bbl in 2017 and a c.2% appreciation in the rand (against the US dollar) over the same time period to lead to a meaningful increase in private transport inflation from around 2% on average in 2016 to c.10% in 2017.

Until recently, the notion of interest rates remaining low for longer in developed markets led to gains across emerging market assets including the rand. However, an instruction from the Hawks for Finance Minister Pravin Gordhan (and others) to present themselves at a meeting investigating allegations of a SARS rogue unit has sent the rand tumbling again as investors contemplate the possibility of a reshuffling of key positions in cabinet. As such, the currency remains as a key upside risk to the inflation forecast.

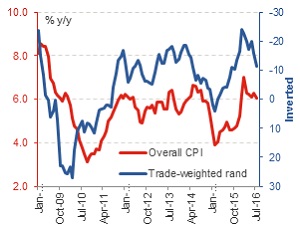

Core inflation inches higher in July

Core inflation (headline measure excluding the impact of food, non-alcoholic beverages, petrol and energy) increased by 0.6% m/m in July, leaving the year-on-year rate at 5.7%. Nevertheless, we expect core inflation to remain below the upper band of the 3% - 6% inflation target band as muted domestic demand prevents a larger pass-through from rising input costs.

Chart 5: Weak domestic demand has limited currency pass-through to date

Source: Stats SA, Momentum Investments

Reserve Bank likely to hold interest rates steady at September 2016 Monetary Policy Committee (MPC) meeting

We view the recent dip in inflation as temporary and still expect the headline print to increase close to 6.5% by the end of the year partly owing to higher food prices in reaction to the drought. Despite the recent retracement in the currency, inflation expectations have remained stubbornly anchored at the top end of the inflation target, threatening the outlook for a further second-round impact on headline inflation.

Moreover, SA’s current account deficit has remained extended despite a narrowing in the trade deficit (exports less imports) as coupon and dividend payments to foreign owners of SA bonds and equities continued to exceed payments received. This leaves SA’s external imbalance vulnerable to a shift in risk sentiment. As such, we expect the SA Reserve Bank to maintain a hawkish tone on monetary policy notwithstanding a fragile growth environment. While we cannot rule out the possibility of a further interest rate increase before the end of the year, a moderation in nominal unit labour costs, recent currency strength (prior to the negative news regarding the finance minister) and downtrodden consumer and business confidence have reduced the chances of further interest rate hikes in the current rate hiking cycle.