Inflation puzzles

Dave Mohr, Chief Investment Strategist at at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

One of the last public acts of the acclaimed physicist Professor Stephen Hawking – who passed away last week – was to defend the concept of cosmic inflation against sceptics in an open letter. On earth, inflation has been making a muted comeback, but it too has its doubters.

New data last week showed US consumer price index (CPI) inflation at 2.2% in February, up marginally from the previous month, while core inflation, which excludes volatile food and energy prices was 1.8%. The Federal Reserve’s preferred inflation measure, based on shifting household spending patterns rather than the fixed basket of the consumer price index, was only 1.7% in January compared to the 2% inflation target.

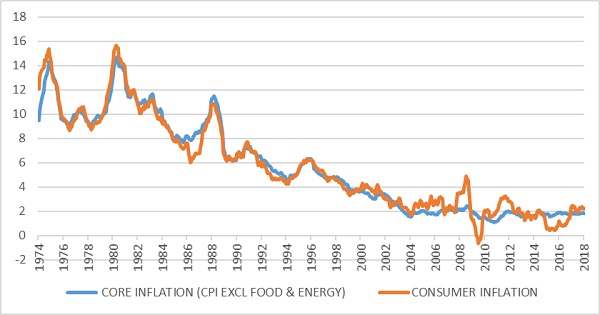

Taking a broader view, chart 1 below shows the long-term trends core and headline CPI inflation for the Organisation for Economic Cooperation and Development (OECD), a club of the most advanced economies. What is remarkable is how stable core inflation has been at around 2% from the early 2000s onwards. This was despite the epic commodity and credit boom between 2003 and 2008, the financial crisis, and the period of ultra-low (even negative) interest rates and central bank bond buying (commonly viewed as “money printing”) in the post-crisis era. Headline inflation has been more volatile due largely to oil price swings (including the peak of $150 per barrel in 2008, and the recent collapse to below $30 in January 2016). But headline inflation has also not deviated away 2% for a sustained period.

With global growth picking up strongly, you would expect inflation to also increase as available resources become scarcer and their prices are bid up. (Forecasters at the OECD last week upgraded their global growth projection for this year from 3.7% to 3.9%.) In particular, the sharp decline in unemployment rates across the developed world has given rise to the expectation that wage growth would accelerate, in turn putting upward pressure on prices. This has not happened. There are a number of theories for the absence of wage and price inflation, but the simplest is that there is still spare capacity in production and in the labour market, while global competition (outsourcing) and technological advances also put downward pressure on prices and wages. The OECD noted that price and wage inflation “are likely to strengthen gradually in the major economies as labour markets tighten … but underlying inflation remains mild”.

Why are there concerns about inflation being too low? Inflation that is too low for too long suggests an underlying lack of economic vigour. Stable, low but positive inflation is considered to be ideal (hence the adoption of a 2% inflation target in many developed markets). Stable inflation allows for businesses to plan better, but positive inflation helps to grease the wheels of commerce. From a monetary policy point of view, low but positive inflation was expected to give rise to low but positive interest rates, avoiding interest rates hitting zero. As it turned out, interest rates spent much of the past decade at or even below zero in the developed world.

Negative inflation (deflation, or falling prices) sounds great from a consumer point of view, but it can also lead to a vicious cycle of consumers postponing purchases in anticipation of even lower prices. Since workers are extremely reluctant to accept wage cuts, deflation instead leads to job losses. Especially pertinent in the current era of high debt, positive inflation erodes the real value of debt. Deflation increases the debt burden causing consumers to spend less and repay debt, leading to more job losses and a vicious downward spiralling economy.

Patient, persistent and prudent

For investors, the key question this year has been whether central banks will pull the rug from under markets and the economic recovery. A surprise jump in inflation could really unsettle markets. (We got a taste of it in February when a single data point on US wage growth prematurely signalled an acceleration.) But the real question is how central banks will respond.

In a speech last week, the European Central Bank (ECB) president Mario Draghi said he needed “further evidence” that inflation was heading towards the bank’s target of slightly below 2%. In the meantime, the ECB’s approach to monetary policy would “remain patient, persistent and prudent”. The ECB will continue to buy €30bn bonds per month until September and maintain negative interest rates beyond then. Eurozone inflation was only 1.1% in February, lower than initially thought with the strong euro (up 16% against the dollar over the past 12 months) putting some downward pressure on price increases.

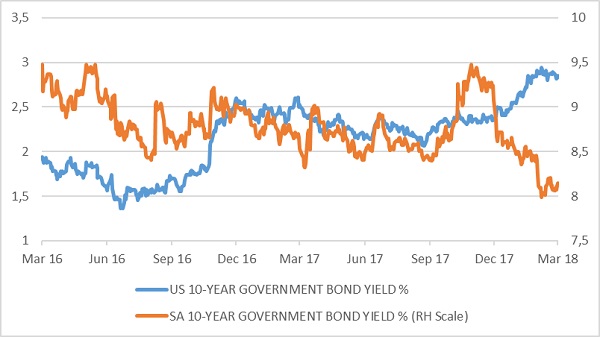

Will the US Federal Reserve be equally patient? It has stopped buying bonds and is allowing the bonds it bought to mature without replacement, and has slowly raised its policy interest rate since 2015. It is expected to raise rates again at the monetary policy meeting this week, the first under new Chair Jerome Powell’s leadership. Of more interest to the market will be the expected path of rates in the coming years. Participants in this meeting each bring a set of forecasts for key variables and these are plotted on a chart to give an indication of how officials see policy evolving. Investors will closely scrutinise whether this “dot plot” will show a steeper rise in expected interest rate increases than the December version. Since December, the last time the Fed hiked rates, 10-year US treasury yields have increased from 2.3% to 2.8%, reflecting somewhat higher inflation and interest rate expectations. But the 10-year failed to breach the 3% mark and has declined in recent days.

Higher inflation in emerging markets

Emerging markets tend to have much higher inflation than developed countries, a function of volatile exchange rates, a lack of competition in domestic markets, relatively highly unionised labour force (which renders wage-setting less responsive to shifts in economic conditions), and often, loose monetary and fiscal policy. But even in emerging markets, inflation rates have declined in a process of converging on developed market inflation rates. Episodes of central banks printing money to fund government deficits – leading to hyperinflation – were once common across emerging markets, but no more (the current example of Venezuela being an exception).

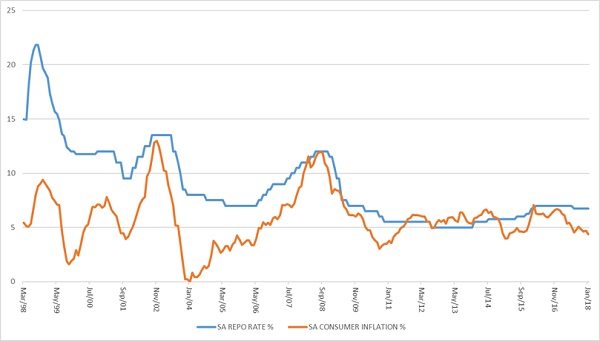

In South Africa, where the SA Reserve Bank will decide on interest rates next week, interest rates have been on the high side precisely to keep inflation in check. But even here, the global wave of disinflationary pressures is washing over. Despite exchange rate volatility, electricity tariffs tripling and oil and food price jumps, inflation remained close to 6% in the post-crisis era and has recently declined to 4.4%. This week’s data release is expected to show a further decline to 4.2%. Core inflation was at a five-year low of 4.1% in January. Chart 2 shows the longer-term decline in inflation, also converging (in fits and starts) on developed countries’ inflation rates. As a result, local interest rates have also trended lower.

This should be enough to warrant interest rate cuts, but the Reserve Bank’s thinking appears to have shifted somewhat in recent times. A recent research paper from the Reserve Bank’s economics department suggests that the neutral real interest rate – the rate where inflationary and disinflationary forces are balanced - is 2%. This seems high. Since the introduction of the inflation targeting regime in 1999, the real interest rate has been 3% whereas the average of the last 10 years is around 1%.

Since an interest rate is simply the cost of borrowing money, if it was too low there would be excessive borrowing and vice versa. Credit extension in South Africa is anaemic at around 5%, hardly indicating that rates are too low. Meanwhile, the risks that the SARB have focused on have subsided: the oil price rise has stalled with US shale output booming, further credit downgrades are less likely as fiscal consolidation moves back on track with a VAT increase and spending cuts, and despite US rates rising for more than two years the rand has appreciated over this period.

The other shift in the Reserve Bank’s thinking is to target the mid-point of the 3% to 6% target range more explicitly, rather than being comfortable with inflation slightly below the top end of the range. In other words, until inflation forecasts move down towards 4.5%, interest rate cuts appear less likely.

From a local investor point of view, the Reserve Bank’s tough stance means fixed income remains an attractive option with yields on long-dated bonds above 8%. But it does imply a somewhat weaker outlook for household spending. This could be offset if there is employment growth or if wage growth picks up, in other words if businesses expand.

The BER/RMB Business Confidence Index increased to the highest level in three years in the first quarter, as businesses express optimism over the recent political changes. However, the latest reading of 45 index points still suggests that the majority of respondents are pessimistic. This should improve in coming quarters, though, resulting in businesses expanding investment and hiring in the local economy. A rate cut next week certainly won’t hurt.

Chart 1: Consumer inflation in the advanced economies, %

Source: Datastream

Chart 2: US and South African 10-year government bond yields, %

Source: Datastream

Chart 3: South African consumer inflation and policy interest rate

Source: Datastream