Inflation: down but not quite out

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Equity markets were choppy last week, with the on-again-off-again summit between President Trump and North Korean leader Kim Jong-Un and the backing away from the trade agreement with China causing sentiment to swing. Since it is not even clear that there is agreement within the White House over the goals of the US, geopolitical uncertainty is something we’ll have to live with. So let’s rather focus on the more important drivers of the investment outlook, inflation and how interest rates respond to it.

Dovish minutes

The minutes from the Federal Reserve’s (Fed’s) previous monetary policy meeting emphasised that the 2% inflation target is symmetric, confirming that investors should not be spooked if inflation overshoots 2% for a while as expected. In fact, the Fed sees such a development as ‘helpful’ in anchoring expectations around 2%, given that inflation has been running below target for most of the past decade. The minutes also indicated that interest rate increases would be gradual to sustain a strong economy and labour market. The market interpreted the minutes as “dovish” and scaled back interest rate expectations. (In central bank speak, the hawks fear inflation and are in favour of higher interest rates, while the doves tend to favour lower interest rates to support growth.) The yield on the 10-year Treasury fell back below 3% as bonds rallied. Simply put, the Fed is increasing its policy interest rate to return to a more “normal” level (it is still negative in real terms) and not because it is scared of runaway inflation.

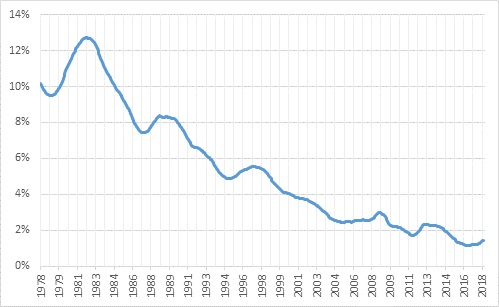

In the 1970s and early 1980s, inflation was persistently in double digits in the US and other developed markets. The Fed aggressively hiked interest rates (all the way up to 19% in 1981), causing a deep recession, but it succeeded in breaking the back of inflation. Deregulation of the economy, technological advances and globalisation then combined to structurally drive inflation down in the coming years. From the early 1990s onwards, the vast armies of workers in India, the former Soviet Bloc and, most significantly, China joined the global labour market. The cost of producing almost anything has increased very slowly and declined in many cases. While most services can only be consumed locally (like getting a haircut), many can be outsourced to cheaper locations (such as call centres).

Chart 1 shows the decline in inflation rates in the developed world over the past 40 years. There are still cycles, partly influenced by commodity prices and currency movements, but the long-term trajectory has been lower. Currently, inflation is picking up on a cyclical basis across the developed world (unevenly, with the US in the lead), but there is no reason to expect a sustained increase in average inflation rates even in the US where the unemployment rate has plunged to 3.9% and the economic cycle is about to go into the ninth year, the second-longest since World War 2. Even during the epic commodity and credit booms of 2003 to 2008 inflation in developed markets picked up only marginally.

Better late than never

South Africa was late to the lower inflation party, but the trend here has also been downward since the 1990s. The country also re-joined the global economy in the early 1990s by dismantling many of the tariffs, subsidies and regulations that protected producers at the expense of consumers. Over this period, local unions have been extremely successful in forcing real wage increases and this is one of the reasons why inflation has taken longer to decline structurally here. But the bargaining power of unions seems to be declining, as indicated by the preliminary recent public sector wage agreement. While the increase for 2018 is still generous, for the subsequent years state employees will get increases exceeding inflation by at most 1%.

The latest data from StatsSA show consumer inflation rising to 4.5% in April from 3.8% in March, reflecting the higher Value Added Tax rate, the introduction of the sugar tax and a higher petrol price. However, the increase in inflation was again less than expected, with the consensus forecast at 4.7%.

The oil impact

The combination of a weaker exchange rate this month and higher global petroleum prices means that there is currently an 82 cents per litre under-recovery which is likely to translate into a similarly-sized petrol price increase early next month. Petrol inflation was reported as 9% in April, and May’s number will be similar. June’s petrol inflation could therefore jump to 16%. Core inflation, which excludes volatile food and fuel prices, also increased to 4.5% but has been within the Reserve Bank’s 3% to 6% target range since January 2010.

We have no option but to import oil for fuel and have no control over the oil price. If the oil price surges, as it has in recent weeks, it has a direct impact on inflation since petrol is 4.5% of the CPI basket. However, the true impact of a jump in the oil price depends on whether companies push up their selling prices to compensate for the fact that their input costs have increased. This is the “second round” impact of an oil price increase and will determine how the Reserve Bank responds. If workers demand higher wages in response to the increase in the fuel prices, that would be a significant input cost for most companies that they will in turn attempt to pass on to their consumers. Therefore, it could result in a “wage-price” spiral: workers demand higher wages, firms respond with higher selling prices, which in turn cause workers to demand still higher wages. However, in a highly competitive and flexible economy, where firms have limited pricing power and workers limited bargaining power, a wage-price spiral will struggle to get going. This is increasingly the case in South Africa, while in the US and elsewhere in the developed world, this is the key difference between today and the 1970s. In this way, a more competitive economy is more resilient to external shocks such as an oil price spike or exchange rate slump.

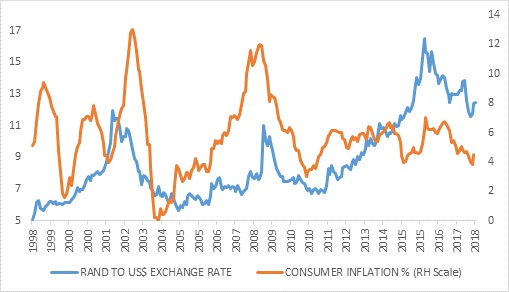

While the rand is still volatile, its impact on inflation has declined. Between 2011 and 2015, the rand depreciated by around 20% per year, without a sustained jump in inflation. In contrast, when the rand blew out in 2001, going from R7.50 per dollar to R12.50 per dollar, inflation tripled from 4% to 12% the next year. The period since 2011 has also seen electricity tariffs triple, a drought-induced food price shock and substantial oil price volatility. Despite all that, inflation has averaged 5.5% over this period. Compare this with average inflation of 14% in the 1980s and 9% in the 1990s.

Interest rates on hold

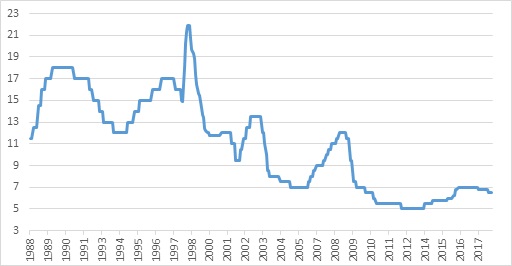

The major benefit of lower and less volatile inflation has been that interest rate cycles have become much milder, as seen on Chart 3. The SA Reserve Bank’s (SARB’s) Monetary Policy Committee (MPC) left the repo rate unchanged at 6.5% last week, as expected. While its own inflation forecast was largely unchanged, it noted that the risks were now tiled to the upside, due to the higher oil price, stronger US dollar and the recent bout of capital flight from emerging markets. Though the rand weakened by 6% against the US dollar between the March and May MPC meeting, it has held up very well given the swings in global market sentiment. The SARB expects inflation to peak at 5.5% in the first quarter of next year, after which the impact of the VAT increase will roll out of the year-on-year numbers. Despite disappointing first quarter growth data, the SARB still expects the local economy to grow by 1.7% this year, while next year’s forecast was raised slightly.

While inflation is within the 3% to 6% target range, the SARB does not see its job as done yet. It has succeeded in getting South Africans to believe that future inflation will on average fall within its target range, but most people see 6% as being the de facto target, rather than being the upper-end of the range. The SARB instead wants South Africans to anchor their future expectations of inflation on the mid-point of the range, and is only likely to cut rates again if its own forecasts show inflation close to 4.5% over the medium term. Further rate cuts are therefore unlikely.

Real returns matter

The declining trend in inflation over the past three decades is good news all round, but investors shouldn’t be complacent. Even at low rates of inflation, price increases compound over time. At 4.5% inflation, the price level will double every 17 years; conversely, your real purchasing power will halve every 17 years. From an investment point of view, fixed income is the asset class that is most vulnerable to inflation (because it pays out fixed amounts whose value can be eroded by inflation) and therefore a structural decline in inflation is good for bonds. Also good for bonds is therefore the Reserve Bank’s independence and determination to contain inflation, a point highlighted by S&P Global Ratings over the weekend when it maintained South Africa’s current credit rating with a stable outlook. The asset class that best protects against inflation over time is equities. And since inflation in South Africa is influenced by the exchange rate (albeit less so than in the past), owning rand-hedge assets is also important. You can see where we’re going with this. The strategies we manage for our clients are diversified across all these asset classes, with weights depending on market conditions and the return goal of each fund. And all strategy funds have an explicit real return target, since beating inflation is crucial to building wealth.

Chart 1: Consumer inflation in the developed economies, three-year moving average

Source: OECD

Chart 2: Rand-dollar exchange rate and local inflation

Source: Thomson Reuters Datastream

Chart 3: South Africa repo rate, %

Source: SARB