How does the rand compare to other emerging and frontier market currencies?

Rami Hajjar

As anyone who has travelled to the USA, UK or Europe recently would tell you, converting rands into either of these currencies is a painful and expensive experience.

In less than five years, the rand/euro exchange rate has increased by almost 25%, the rand/dollar by approximately 33% and the rand/pound by about 28%. The question many may be asking with equal vigour around a braai or the boardroom table is, is South Africa’s rand at risk of a currency debasement?

According to Rami Hajjar, portfolio manager at Allan Gray, when looking at other emerging and frontier markets, a trend of reckless fiscal and monetary policies has led to very high inflation levels, and these have been the main drivers of the currency collapses. In South Africa, the picture is quite different.

“Our risk assessment suggests that the probability of a currency debasement in South Africa is low. We are hopeful that the action plan currently in place to solve the crucial infrastructure issues, together with successful efforts to contain the fiscus, will prompt a re-evaluation of South Africa’s investment case,” says Hajjar.

He explains that there are several important factors to consider when trying to understand what is going on with a currency, including monetary discipline, foreign exchange supply and demand and lastly, investor confidence.

“Continued monetary discipline and anchored inflation expectations will be important drivers of currency stability going forward – while recognising that monetary policy can lose its effectiveness with fiscal imprudence,” says Hajjar.

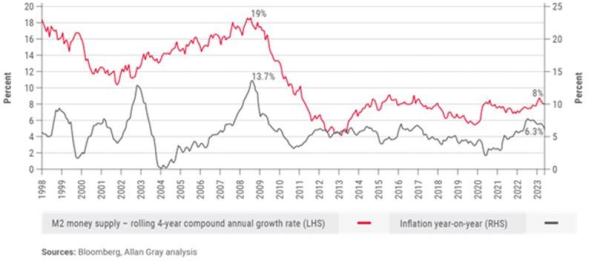

Graph 1 shows that South Africa has a good track record of monetary discipline. Hajjar says this is one benefit of having an independent central bank that respects a mandate to control inflation.

Graph 1: SA money supply and inflation

The other fundamental factor in currency stability is foreign exchange supply and demand.

“South Africa has a structural current account deficit, which means that normal economic activity results in more foreign exchange going out of the country than coming in, in any given year. But the deficit is not large, and the country fares well relative to other markets we consider, as it has an export base that is sensitive to rand weakness, and some import substitution can take place when the currency weakens a lot – a natural adjustment mechanism,” says Hajjar.

He explains that the latter factor means that the pass-through effect from the weakened currency to inflation is not very large, compared to that in a country like Egypt, for instance, where the local manufacturing base is very weak.

“But no matter how solid the fundamentals of a country are, investors losing confidence in a market can drive a run on the currency. In such a scenario, a dangerous feedback loop can kick in where negative sentiment drives currency drops, and large currency drops start to de-anchor inflation expectations, which causes further currency drops.”

Over the last year, various events have occurred that have not boded well for SA investor confidence, including the country’s greylisting in February by global financial crime watchdog the Financial Action Task Force (FATF), an investment downgrade from S&P Global in March, and the ongoing loadshedding crisis, to name but a few. Since then, the government announced a new plan to attract R2 trillion in investment into the country over the next five years.

“The government is aware of the need to prioritise foreign investment. Plans are underway to re-ignite investment in SA – notwithstanding the challenges we face,” concludes Hajjar.