Greece: A ‘No’ vote means difficult negotiations ahead

Greek voters delivered a resounding ‘No’ at the July 5 referendum, with 61.3% rejecting the reform proposals in exchange for loans of the bailout creditors. The Greek Prime Minister will ask to foreign lenders for a new financing programme including debt restructuring. The Greek finance minister resigned yesterday in order to facilitate the resumption of negotiations.

What are the next steps?

A deal is unlikely to be reached in the coming days. A compromise will be difficult to reach, all the more Germany's position on a debt relief remains unclear (unlike the IMF).

The German government signalled a tough line towards the country on Monday July 6, saying it saw no basis for new bailout negotiations and insisting it was up to Athens to move swiftly if it wanted to preserve its place in the Eurozone.

Despite the outcome of the referendum, the ECB will likely continue to provide liquidity to Greek banks as long as there are negotiations but this will remain capped to its current ceiling (€89-billion).

Risks in Greece

A) A deal needs to be negotiated before July 20, when the country must pay back €3.5-billion of Greek government bonds. Moreover, it is not clear whether Greek banks will be able to hold out until that date without receiving additional liquidity. If negotiations resume and a compromise is found by July 20 (i.e. two conditions), business confidence should bounce back and a gradual recovery process could resume. Fiscal revenues and bank deposits would stop falling. But, in the meantime, if banks reopen, capital controls are likely to last and could even be strengthen (for instance, the Greek central bank could levy a tax on deposits).

B) If there is no agreement and the Greek government defaults once again on its debt (in a widely expected step, Greece did not make its €1.5-billion payment to the IMF on June 30), the ECB will stop providing Greek banks with liquidity. A fortiori, capital controls would persist. In a context of a sharp liquidity squeeze, the Greek government would have no other choice than to print a new currency for domestic payments, thereby exiting de facto from the Eurozone.

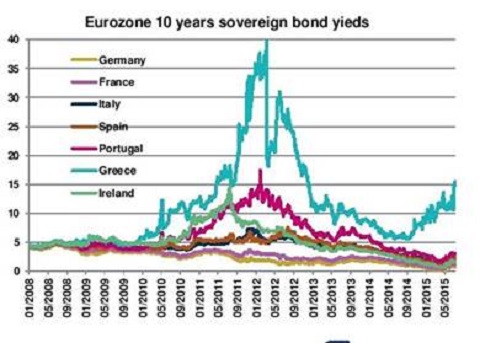

Risks in the Eurozone

Shares fell, the euro stumbled and yields on weaker Eurozone economies' bonds rose after Greece voted ‘No’ at the referendum, but contagion was limited on Monday July 6. This can be explained in part by the fact that the rest of the Eurozone is much less linked to Greece than it was in 2011-2012, as the private sector (especially banks) is not exposed to the Greek public debt anymore.

If needed, the ECB could buy more government bonds to help the more vulnerable countries of the area by ramping up its quantitative easing (QE) programme or by implementing its Outright Monetary Transactions (OMT) Programme. However, as regards the latter, the recipient country needs to be in a full or precautionary EFSF/ESM programme.

Nevertheless, markets have probably ‘not spoken their last word’ and business confidence could take a hit. Besides, the euro is likely to depreciate further. All in all this clearly still poses downside risks to our “weak but gradual recovery scenario” in the Eurozone.