Global gasoline prices, recession fears and possible Eskom related downgrades

Adriaan Pask, CIO at PSG Wealth

Concerns about higher inflation, rising interest rates and a looming recession have dominated markets recently.

In the commentary below, PSG Wealth CIO, Adriaan Pask looks at the following:

- Why the decline in oil prices are mostly positive

- Interest rates continuing to pose uncertainty to investors

- Why the full-scale energy crisis is enough to tip the rating scales downwards

What this backdrop means for investors and asset allocators

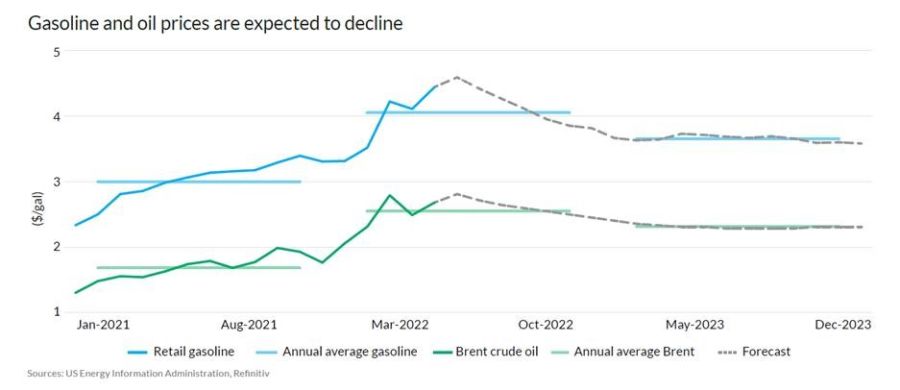

Lower oil prices create reprieve for inflation fears

The price of oil dipped below US$100 a barrel for the first time in over three months in early July 2022, prompted by fears of a looming US recession that could temper demand. While a decline in oil prices has several effects, here’s why we think it’s mostly positive:

• It lowers inflation and expectations thereof;

• Lower inflation and inflation expectations tend to slash nominal interest rates and may drive increased demand for interest rate sensitive durable goods such as automobiles and housing.

• It helps to reduce operating expenses of the transportation sector and other industries that are relatively large users of gasoline, diesel, and jet fuel.

• It creates potential for increased capital expenditure by businesses. The average price for unleaded gasoline in the US could fall by up to $0.50 in the coming weeks, the US Energy Information Administration noted.

At home, despite the recent domestic petrol price decrease of R1.32 per litre, the persistent high costs on fuel continue to batter financially strained consumers and compound the pressure on a struggling economy. Encouragingly, Government is working on several regulatory changes to address the country’s petrol crisis including:

• The introduction of a price cap.

• A proposal to stop publishing guidance on diesel prices.

• A process to review the Regulatory Accounting System (RAS), which could result in a significant decrease in fuel prices by 2028.

Higher interest rates underpin latest recession fears

The US Federal Reserve (Fed) signalled more rate hikes to come after the annual inflation rate in the US reached yet another record high, rising to 9.10% in the 12 months to June 2022 – levels last seen in 1981. Policymakers admitted that the task of reining in runaway inflation without triggering a recession would be tough. The median probability of a recession over the next 12 months is over 47%, up from 30% in June 2022, according to a recent Bloomberg survey. Decreased consumer spending is another sign of a looming recession in the US. Wells Fargo predicts that by September 2022, we will start to see significant declines in consumer spending “as more people dip into their savings to cover the growing costs of goods and services”.

The South African Reserve Bank (SARB) was the latest central bank in July to reiterate its policy tightening commitment with the hopes of taming a record-high 7.40% inflation rate - taking the local repo rate to 5.50% y/y in July. While the upwardly revised repo rate will support credit demand over the short term, it also heightens the risk of eroding the differential that makes local assets attractive to international investors.

Higher inflation has also forced the European Central Bank (ECB) to raise its interest rate for the first time in more than a decade. The ECB raised its key interest rate by 50 bps in July 2022, with a further normalisation of interest rates deemed to be appropriate for each of the remaining monetary policy meetings in 2022. Lower confidence levels and higher commodity prices, together with pandemic-related disruptions in China and gas shortages due to the war in Ukraine, have worsened existing supply chain pressures. These factors pose a risk to the economic recovery of the Eurozone with the central bank projecting real GDP to grow by 2.80% on average in 2022 and by 2.10% in both 2023 and 2024. Headline inflation is expected to remain at a high of 6.80% for the remainder of the year before easing in 2023. Price pressures will also remain elevated in the near term, due to higher oil and gas prices and increases in basic food prices.

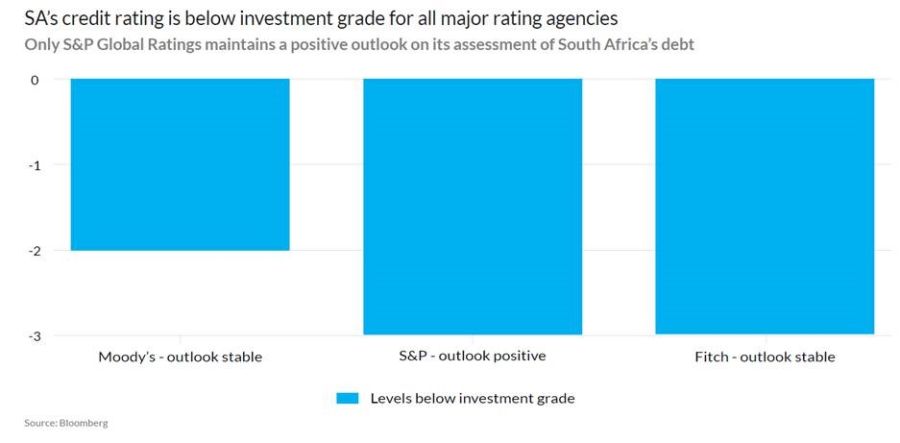

Eskom stage 6 sounded alarm for possible ratings downgrades

Economists have warned that SA’s energy crisis and subsequent load shedding continue to pose a significant risk to the economy, putting the possibility of rating downgrades back on the cards. Economists estimate that power cuts are costing the country over R700 million per stage, per day. On a provincial basis, this translates into R75 million per stage, per day. Adding to a range

of other socio-economic issues, such as high unemployment and poverty, the illegal protests that were behind the previous round of power cuts are seen to be a microcosm of the disgruntlement at rising costs and the waning purchasing power of SA households. Over the longer term, Eskom’s woes are underpinned by a lack of investment and maintenance.

Now that labour unrest and sabotage have been introduced to the equation, the full-scale energy crisis is enough to tip the rating scales downwards and make the case for a negative outlook. While SA has managed to avoid rating downgrades so far this year, Fitch Ratings warned of risks posed by the poor finances of many public entities. “Electricity shortages weigh heavily on growth, and this could worsen before new supply, mostly in the form of independent power producer (IPP) projects, comes on line,” Fitch said. “While the government is making progress with its reform agenda, the scale of measures (beyond electricity) is too limited to make a significant difference to potential growth in the medium term.”

Current assessments of SA’s debt from the three major rating firms are the lowest they’ve been since 1994.

What this means for investors and asset allocators:

With the current tough market backdrop, a state of affairs that is only heightened by the continued uncertainty around multiple factors such as inflation, rising rates, the conflict in Ukraine, we think it is critical to stay focussed on your investment plan and not get side tracked by market noise. Unfortunately, emotion can have a big impact on investment decision-making, and this is highlighted by the angst and pain experienced in market downturns. While acute at the time, over the long term, these downturns (and the subsequent emotions) are likely a blip on the radar over the timeframe of most investor’s horizon.

While we can rest assured that this will not be the last time markets are challenged as experienced over the past few months, we can be confident that this too shall pass, and markets will recover. We cannot predict the timing and degree of the recovery, but we remain committed to positioning our solutions in a balanced manner that can both navigate stormy seas and benefit from the recovery when the tide turns.

Do not keep your head in the sand, be aware of what is dominating current market dynamics, but also remain true to your investment plan and hold the course, staying invested in times like this is when real growth is realised in the long term.