Global economies showing signs of a grand go-around

Resilient global economies may surprise on the upside in a grand go-around - aviation speak for an aborted landing in which a descending aircraft changes course prior to landing and returns to cruising altitude.

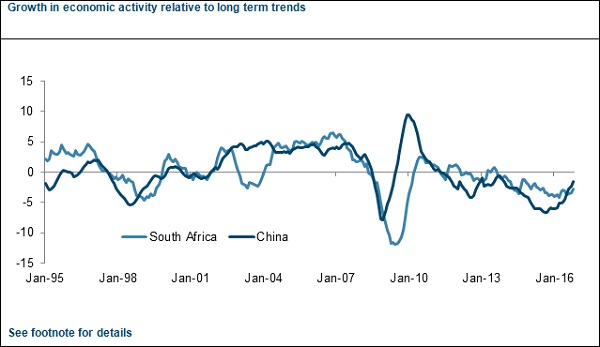

According to Raphael Nkomo, Chief Investment Officer at Prescient Investment Management, recent data suggests that the deceleration in Chinese economic activity between 2013 and 2016 may be about to rebound, providing a much-needed boost to the South African and global economy.

Also encouraging is that global reflation, the first phase of economic recovery after a period of contraction, is not entirely dependent on China.

“After the recent US presidential election, we have been told to expect a vast round of infrastructure spending and corporate tax cuts. Historically, such fiscal injections have been effective methods for reinvigorating growth,” Nkomo said.

From Prescient’s research, it’s evident that South African and US economic activity closely mirror developments in China. The US economy spent most of 2016 at below average growth, but recent data indicates a recovery.

Similarly, South African economic activity has decelerated since 2013 but shows modest signs of turning around. However, domestic GDP growth is close to zero and more data is needed to confirm that a recession has been averted.

Haakon Kavli, Portfolio Manager and Analyst at Prescient Investment Management, commented: “The signal from China is undeniably strong and that’s important. Historically, most contractions in our economy have been halted by a pick-up in demand for exports, mainly commodities to faster growing economies like China.”

On the correlation between Chinese and South African economic activity, he said South African exports are important inputs in industrial production and infrastructure development.

“As long as South African commodity production is free from political interference and structural constraints, the country is perfectly placed to benefit from a pick-up in global growth.

“If the US implements the promised $1 trillion infrastructure investment program, this will cause a significant spike in demand for the kind of commodities South Africa produces. The US could therefore become a catalyst for SA economic expansion. At the industry level, the beneficiary sectors would include construction materials and engineering, metals and mining and machinery,” Kavli said.

While the US economy is not in need of aggressive fiscal stimulus, South Africa is growing well below potential and would benefit from increased demand. Unfortunately, the South African treasury does not have the fiscal space to implement its own round of stimulus.

Nkomo added that the Republican clean sweep appears to be pro-growth for equities and bearish for bonds in the short- to medium-term. “Our expectation is centred on decreased regulation, favourable tax reform, increased fiscal spending and less congressional gridlock. The combined effect should drive stronger revenue growth and higher net income margins, which are positive for equities.

“We expect value and small cap stocks to outperform in South Africa. This is typical of early cycle rallies, and motivated by the fact that value and, more recently, small cap stocks have been disproportionately penalised in the recent past and are trading at attractive discounts.”

Footnote: The figures plot the Prescient Economic Activity index for China and South Africa. A number below zero suggests below average growth in economic activity. A positive number suggests growth is faster than its long run average. (A negative number does not necessarily imply negative growth). The numbers are derived using a statistical method that draws the common trend from a large set of roughly 100 variables including consumer spending, industrial production, employment, transportation, energy consumption, survey data, etc.