Global central banks re-ignite a “risk-on” environment

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Concerns over the health of the global economy have deepened. Most major regions are now expected to expand at a slower pace this year relative to the growth rates observed in 2015. Recognition of the external risks to the United States (US) economy caused a more dovish rhetoric from the US Federal Reserve (Fed), triggering a slide in the US dollar, while the European Central Bank (ECB) and Bank of Japan (BoJ) eased monetary policy further in 1Q16 amid serial disappointment on growth and inflation prospects.

Receding fears of a so-called “hard landing” in China and a recovery in commodity prices spurred “risk-on” sentiment, contributing to a sharp rebound in beleaguered emerging markets (EM). The MSCI EM Index ended the first quarter of the year 5.4% higher, outperforming the MSCI Developed Markets Index which tracked broadly sideways (-0.1%) over the corresponding period. The MSCI EM Latin America (LatAm) Index was the clear outperformer over 1Q16, surging ahead by nearly 20%, while the MSCI EM Europe Middle East and Africa (EMEA) Index posted a healthy gain of 12.1% over the same time period. JPMorgan data shows that despite EM equities experiencing significant inflows to the order of USD7.3 billion in March, partly reversing the negative trend in cumulative flows for the quarter, SA equities still suffered outflows of R24.9 billion (USD1.6 billion) in 1Q16.

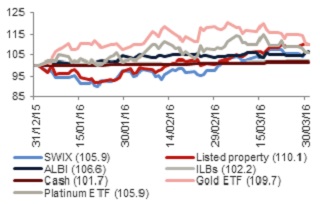

Nevertheless, the FTSE/JSE SWIX managed to end the quarter 5.9% firmer (see chart 1), led higher by gains in resource stocks (18.1%). The FTSE/JSE Financials Index benefited from rand strength despite a deteriorating macro picture (+6.2%), while the FTSE/JSE Industrials Index lost ground (-0.4%) over the same time period.

A steady rise in precious metal prices during the quarter drove gains in the platinum and gold ETFs, notwithstanding a firmer domestic currency. The rand staged a 4.8% recovery against the US dollar in 1Q16, despite depressed domestic sentiment and lingering policy uncertainty, as a weaker US dollar and easing concerns around China led to a broad-based global rally in commodity-related currencies.

Amongst the local asset classes, listed property outperformed, gaining 10.1% in the first quarter of the year. This was linked to a 65 basis points rally in ten-year domestic bond yields during 1Q16, which helped the latter to record a 6.6% return. Inflation-linked bonds (ILBs) and SA cash were the worst performers during 1Q16.

Chart 1: SA asset class performance in 1Q16 (indexed)

Source: INET BFA, Momentum Investments

Our view that the recent rand recovery would prove to be unsustainable in the coming quarters in the absence of a meaningful rally in commodity prices should provide currency support for foreign asset class returns during the remainder of 2016.

Our global preference remains for equities over fixed-income assets, while recent profit upgrades have improved the valuation underpin for the local share market. In contrast, the dear valuation of SA listed property is likely to constrain the return potential from this asset class. Meanwhile, the rising domestic rate cycle continues to support local cash returns. In tandem with the rand, domestic bonds could come under some pressure in the ensuing months as ratings agencies ponder the country’s credit status, as political uncertainty prevails and as the August municipal elections approach.

Global central banks taking a cautious approach

Despite major central banks ramping up their balance sheets to unprecedented levels and running ultra-accommodative monetary policy rates in their respective economies, growth remains relatively sluggish worldwide while lacklustre inflation persists in many key regions. Though central banks in the US, United Kingdom (UK), Eurozone and Japan have seen their balance sheets soar to 151% of GDP in 4Q15 from 49% in 4Q07 (as calculated by Goldman Sachs), policy efforts to spur on activity in struggling economies have been subject to diminishing marginal returns. More recently, the BoJ and the ECB have joined Denmark, Switzerland and Sweden by expanding their focus from traditional policy easing measures to adopting a more unorthodox approach by cutting interest rates into negative territory in an effort to prevent the economy slipping into a recession and sliding back into deflation.

The aim of negative interest rate policies (NIRP) is to punish banks that hoard cash instead of extending loans to companies and households, thereby countering a subdued inflation outlook. The problem however is that rates below zero may not reduce borrowing rates in the real economy and may instead crimp banks’ profitability and encourage undue risk-taking in search of profits. The Bank of International Settlements (BIS) warned that it would be difficult to predict how individuals or financial institutions would behave if rates were to fall further below zero or remain in negative territory for an extended period.

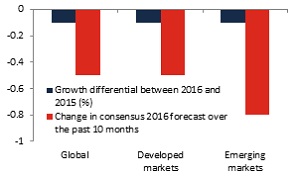

The latest Bloomberg consensus estimates for March 2016 place real GDP growth prospects at only 3.0% this year from 3.5% in May 2015. While the slowdown in emerging countries was anticipated, economic surprises in this region have still been to the downside. Moreover, developed market (DM) growth prospects have dimmed somewhat too (see chart 2) on the back of disappointing activity.

Chart 2: Shallower global growth recovery expected (%)

Source: Bloomberg, Momentum Investments

In the United States, softer growth momentum has raised a more cautious approach to near-term monetary policy, but a more promising outlook on inflation suggests that two more interest rate increases (of 25 basis points each) by the Fed this year cannot be ruled out.

In addition to firm jobs growth, healthy savings, positive real wages (thanks to low oil prices) and robust US household net wealth metrics should support further growth in household consumption, which increased close to 3% in real terms in the final quarter of 2015. Though a further tightening in the US labour market has been less successful in stirring up higher wage inflation, at the same pace that has been the case historically, nominal earnings growth is slowly ticking higher. Survey indications of higher wage expectations by consumers and higher wages to be awarded by employers will likely further drive inflation measures higher over the course of the year, while the disinflationary impact of lower oil prices and a weaker US dollar abate.

Though the short-term growth and inflation impact of the US November 2016 election is likely to be limited, market volatility could spike in the months leading up to the presidential race.

Over in the UK, political mayhem could unfold as the UK’s relationship with the European Union (EU) comes into the spotlight. The debate over a possible UK exit from the EU has been hotting up with immigration laws and employment opportunities ranking high on the agenda for the “leave” camp, while the likely negative economic repercussions of a so-called “Brexit” continue to concern the “stay” camp.

In the event of a Brexit (which is not our base case), we would expect a reasonably large drag on investment, a sharp increase in financial market volatility and a likely increase in political tensions. Household consumption should weaken on higher inflation and negative employment effects. A reduction in capital inflows and slow labour force growth would reduce potential growth in the long run, while the region would have less favourable trading relations with the EU.

With exit negotiations likely to be drawn out under a Brexit scenario, an actual exit could be extended to early 2019 resulting in protracted economic uncertainty. The reaction function of the Bank of England (BoE) would also likely be different under a Brexit scenario. Although policy could stay on hold initially, a weaker currency and higher inflation would prompt a faster pace of rate hikes than under a scenario where the UK remains.

Meanwhile, growth fears and paltry inflation prints are likely to keep monetary policy in easing mode at the ECB and BoJ. The ECB injected yet another dose of stimulus into their still-fragile economy earlier this year, while the BoJ struggled to boost inflation expectations and growth prospects even after cutting interest rates to below zero.

Dispersion across emerging nations persists

EM risk appetite has improved markedly following the Fed’s communication that fewer rate hikes and a more protracted interest rate cycle was likely to take place given growth and financial market stability concerns. Nevertheless, growth fundamentals remain weak. The degree of commodity reliance and the sensitivity to rising US rates as well as to US dollar movements continues to drive a divergence in economic outcomes across EM.

Stagflationary pressures (high inflation accompanied by low growth) are expected to persist in the commodity-exporting bloc as currency weakness keeps inflation elevated, while countries within Emerging Asia and Eastern Europe are likely to ease policy rates further on low inflation pressures thanks to subdued oil prices. Net commodity exporters are also facing increasing budgetary constraints leading to lower credit worthiness scores, particularly those with a low growth trajectory (and no implementation of a growth plan), an increased vulnerability to commodity prices and low policy predictability.

To a large extent EM underperformance can be attributed to China’s plan to eliminate overcapacity in its traditional growth sectors as it transitions to a more services-related economy while re-focusing exports on higher-value add products. The Chinese authority’s 13th five-year growth plan aims to shrink China’s bloated steel and coal industries, reduce government’s role in business and better enable operating conditions for setting up new firms. We expect steady growth in the household and services sectors of the economy, while heavy industry zones are likely to remain depressed with a limited spillover to the rest of the economy. We expect targeted stimulus to continue to maintain growth rates in line with the country’s five-year plan. This is likely to include further fiscal stimulus, lower interest rates to encourage households to borrow more and lower reserve requirement ratios to buoy the property market.

SA politics undermining structural reform momentum

China’s phenomenal growth rate, averaging 10.8% between 2000 and 2007, funded excessive consumption in South Africa (SA) over the same time period against a favourable backdrop of rising global growth, improving investor risk appetite and abundant cheap capital originating from stimulus packages in key DMs which poured into emerging countries.

The commodity cycle has however turned on the back of China’s growth transition. The Bloomberg commodity price index slid by 55% from its 2Q11 peak, leading to a 10.3% decline in SA’s terms-of-trade (a measure of SA’s export prices relative to import prices).

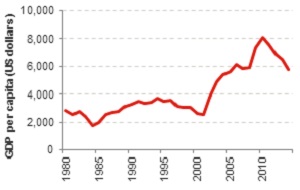

GDP per capita (in US dollars) followed the upward direction of SA’s terms-of-trade during the commodity boom up to 2011 and has since tapered off (see chart 3), hinting at a non-trivial relationship between average living standards and natural resource rents in SA. With commodity prices likely to remain subdued well into 2017 on the back of an oversupply in global stocks and modest demand, the outlook for consumption spend in SA remains muted for at least the next two years.

Chart 3: Average living standards have declined since

Source: IMF, Momentum Investments, data up to 2015

SA’s failure to capitalise on the proceeds of the commodity boom has led to growth occurring predominantly in the non-tradeable goods sectors of the economy which has further exacerbated the unemployment crisis given a slowdown in labour-intensive growth sectors. As a result, SA’s export of tradable goods has become relatively cost uncompetitive. As global risk appetite has waned, EM currencies have come under pressure, but a high cost base and a number of structural rigidities have prevented SA’s exporting firms from responding fully to the exchange rate depreciation, further hindering growth prospects.

The SA Reserve Bank (SARB) is likely to react to slowing growth and a rising inflation trajectory by hiking interest rates by a further two rounds of 25 basis points each, taking the repo rate to 7.5% over the next twelve months in an effort to contain inflation expectations which remain clustered around the ceiling of the inflation target band, even on a five-year forward-looking basis. In reference to the real interest rate, the SARB has noted that monetary policy remains accommodative and as such we are looking for real rates to recover close to an average of 1% over the next two years. In the absence of substantial foreign direct investment into SA, SA’s still-sizeable current account deficit will remain heavily reliant on higher real interest rates to attract foreign portfolio flows in a potential “risk-off” environment where commodity prices are likely to remain under pressure, limiting gains on SA’s terms-of-trade.

Against the backdrop of a low growth trajectory (with little progress on the country’s economic development plan), low policy predictability and continued vulnerability to commodity prices, SA remains at risk of losing its investment grade rating by year end. Standard and Poor’s (S&P) rating agency currently has SA’s foreign debt rating on the lowest investment rung and placed SA on a negative outlook in December 2015.

Of the metrics that SA is scored against, we are most at risk of losing ground on the economic assessment score. S&P downgraded the economic assessment metric from “neutral” to “weakness” between June and December 2015. A low growth environment will likely restrict SA’s ability to raise taxes or cut expenditure limiting the ability of fiscal authorities to respond to economic shocks.

According to SBG Securities, although S&P rates SA’s debt burden as “neutral”, the size of our government interest bill relative to government revenues has increased to a worrisome 13%. Risks from contingent liabilities, currently accounting for 14% of GDP (10% when stripping out the state-owned enterprises with stronger balance sheets) further reduces SA’s fiscal flexibility.

S&P still scores SA as neutral on the institutional and governance effectiveness score (measuring the resilience of the economy, the strength and stability of civil institutions and the effectiveness of policy-making), but a highly polarised political landscape makes future policy responses difficult to predict and jeopardises the momentum of structural reform in the country. Areas such as labour market reforms (including the prevention of prolonged and violent strikes and implementing a secret strike ballot to prevent worker intimidation), black economic empowerment and mining policies need to be addressed urgently to promote structural growth in the economy for SA to earn its spot amongst its investment-grade rated peers. Without sufficient momentum on the structural reform agenda to benefit longer-term growth, SA is facing the prospect of junk status by at least one of the main rating agencies (S&P) by year end.