From crisis to crisis

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

In the coming weeks, the world will mark the tenth anniversary of the most acute phase of the global financial crisis, the bankruptcy of Lehmann Brothers and the crazy days that followed. Many books have been written on the causes of the crisis, tracing its origins from lax lending standards in the booming American property market to the packaging and repackaging of these mortgages into complex financial instruments that entered the global banking system and spread the excessive use of leverage.

Moreover, the shock to the financial system was transmitted with frightening speed to the real economy. As credit markets froze, real economic output slumped at a faster pace than in the first months of the 1930s Great Depression.

Also expect much commentary and opinion in the coming weeks on the true lessons of the crisis and its aftermath. There’s no doubt this will include discussion on whether the actions of the US Federal Reserve and other central banks were enough. Some say it was too little; some too much.

These stimulus measures, including quantitative easing (QE) and zero interest rates, are only now being gradually unwound by the Federal Reserve – with the European Central Bank (ECB) lagging much further behind. Another much-discussed feature was the failure among economists, bankers and regulators to foresee the crisis. In truth, many did anticipate one or two elements of the crisis, but almost nobody could imagine how the various shocks – including $150 per barrel of oil on the eve of the meltdown – would reinforce each other, turning ripples into a financial tsunami.

Worry when no one is worrying

One investment lesson is particularly relevant to our current uncertain times: the time to worry is when things are going well. When the news is objectively terrible, as in the heat of the crisis, it is often a great time to invest. Consider what things were like a year or so before. Growth was strong, commodity prices high, markets were rallying and surging house prices led to a boom in building activity. Credit was flowing fast and freely. The rand was strong. President Mbeki seemed to be a safe pair of hands on the tiller. Emerging markets were the flavour of the month, led by China’s astonishing growth, and capital flows were bountiful.

In contrast, today we face policy uncertainty at home and abroad (including land reform and global trade tensions). In fact, it turns out that uncertainty has a certain value. The long-forgotten economist Hyman Minsky and his “financial instability hypothesis” returned to prominence after the crisis. His thesis was that long periods of stability sow the seeds of crisis as investors, consumers and business people ramp up risk-taking behaviour. In more volatile and uncertain times, a build-up of debt-fuelled imbalances is much less likely, as is a heedless pursuit of risk.

Stuffed turkey

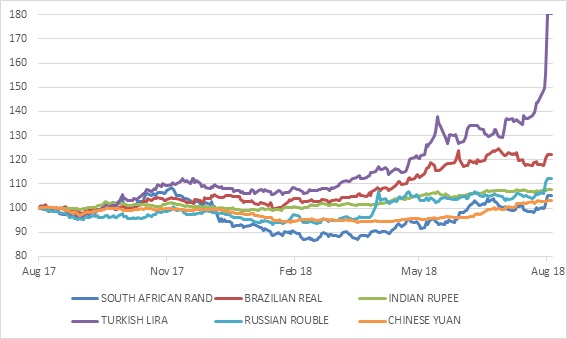

Specifically, last week shone the light on two further sources of uncertainty: Turkey and the weak domestic economy. Turkey’s financial woes have escalated into a full-blown crisis, with other emerging markets, including South Africa, suffering some collateral damage. Turkey faces challenges on a number of fronts. It is in an unstable neighbourhood and runs a large current account deficit, which means it is highly reliant on foreign capital inflows. Fiscal stimulus has fuelled in rapid growth, but also inflation, which currency weakness has only worsened.

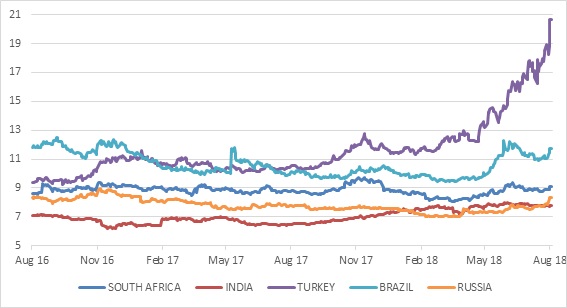

However, President Tayyip Erdogan has strong-armed the central bank into not responding with sufficient interest rate increases. Turkey also has one of the largest dollar and euro-denominated debt loads among emerging markets, and as the lira falls, the debt burden grows. The ECB last week warned that certain European banks could be at risk from their exposure to Turkey. And then the straw that broke the camel’s back came with sanctions imposed by the US and the threats of doubling tariffs on Turkish steel imports. The lira, which fell from 3.5 to 4.9 to the US dollar between January and end July, crashed to 6.7, including a 16% fall on Friday, and another 5% on Monday morning. Turkish 10-year bond yields spiked above 20%. Such stiflingly high borrowing costs could do serious damage to the economy and the banking sector in particular. Promises by the finance minister – Erdogan’s son-in-law – of a more sustainable and balanced growth model were ignored by the markets. Put simply, investors have lost faith in Turkey’s governing institutions and things could get worse before they get better.

It is worth briefly reiterating how South Africa’s situation is different to Turkey’s and why, even though the rand slumped along with the lira on Friday and again on Monday morning, investors should differentiate them. (The fact that the rand did not fall nearly as much as the lira suggests they are.) It is true that South Africa also runs a current account deficit, but fiscal policy is aimed at gradually narrowing the budget deficit.

South Africa’s deep and liquid capital markets and well-capitalised banking system means that most borrowing is done locally, and therefore a weaker rand should not lead to a debt crisis. In fact, a weaker rand tends to be good for the economy and certainly benefits most investment portfolios.

Finally, rather than being too accommodative, the SA Reserve Bank fiercely guards its independence and is determined to maintain inflation within its target range. (Turkey’s inflation rate is 16%, compared to 4.6% in South Africa.) But South Africa is an emerging market and anything that upsets investor sentiment towards emerging markets will influence domestic markets.

Going nowhere slowly

Explaining South Africa’s slow growth despite an upturn in the global economy since mid-2016 is tricky. South Africa is a small open economy and usually follows the global cycle, albeit with a lag. However, we are not a major exporter of manufactured goods and we punch below our weight in terms of our participation in global supply chains.

South African manufacturing has not followed global manufacturing over the past year or so, as the latter posted a notable upswing. In fact, manufacturing output was negative in the first quarter of this year and the latest data from StatsSA show that it was also marginally negative in the second quarter. This increases the odds that the economy as a whole is in a technical recession – defined as two consecutive quarterly contractions in real gross domestic product. This news would not only be a blow to the fragile confidence in the country and what still remains of the “New Dawn” narrative, but it would also seem incongruous given positive growth in other major economies.

The channels through which South Africans should normally benefit from a strong global economy are commodity prices and capital flows. Capital flows are very dependent on sentiment towards emerging markets and expectations of where US interest rates are headed. The strong global economy has not helped the former much this year, while the Federal Reserve remains on a gradual rate hiking path. Clearly investors are very nervous about emerging markets at the moment.

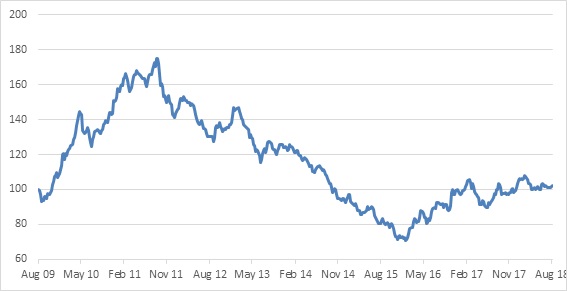

In terms of commodities, the prices of our main commodity exports have picked up since early 2016, but not convincingly, and certainly nowhere near to the levels of a few years ago. The price of our main import, oil, has increased sharply. At the same time, costs for miners – especially labour and electricity – have continued to rise. Hence the recent announcement by Impala Platinum of up to 13 000 job losses. Impala’s share price peaked at R354 in May 2008, a few months before the crisis when the platinum price was above $2000 per ounce. Platinum has more than halved to $800, but the Impala share price is R18, 95% lower.

It seems ironic that the resources sector is the best performing sector on the JSE, but this is due to the dual-listed heavyweights Anglo American and BHP Billiton. These companies have substantially reduced exposure to South Africa over the years. This is yet another example of how the JSE no longer represents the local economy. Therefore, as much as we all need to worry about the prospects for the local economy in our capacity as citizens and taxpayers, there is less need to worry in our capacity as investors.

Investing in uncertain times

In summary, volatility on markets is never pleasant to experience, but it does tend to shake out some of the worst excesses, hopefully making the overall financial system more robust in the process. It also creates opportunities for long-term investors to buy assets that are undervalued due to shifts in sentiment. However, things are almost never certain. Sitting on the side-lines until the “dust settles” requires investors to get the timing right twice: on exiting and on re-entering the market. This is near impossible. As an investment strategy, it is very unlikely to beat an appropriately diversified portfolio willing to ride out the bumps along the way.

Chart 1: Emerging market currencies against the US dollar, indexed to 100

Source: Thomson Reuters Datastream

Chart 2: Emerging market 10-year government bond yields, %

Source: Thomson Reuters Datastream

Chart 3: Index of South Africa’s main commodity prices (gold, platinum, coal and iron ore), $

Source: Thomson Reuters Datastream