ECB March 10, 2016 decisions: A bigger than-expected bazooka

Weaker Euro could benefit the Rand.

On March 10, the ECB surprised financial markets by cutting its three key interest rates and expanding its quantitative easing programme (QE). More precisely, ECB decided to:

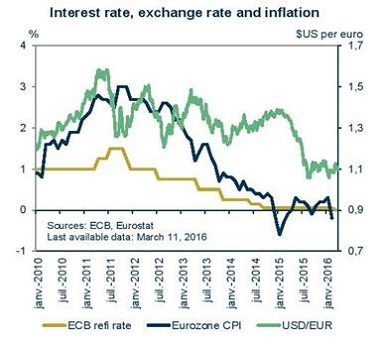

• Reduce interest rates on the main refinancing operations, on the marginal lending facility and on the deposit facility to 0.0%, 0.25% and -0.4% respectively

• Raise the monthly purchases under the asset purchase programme from €60 to €80 billion

• Include, in the list of assets that are eligible for regular purchases, investment grade euro-denominated bonds issued by non-bank corporations established in the euro area

• Launch a new series of four targeted longer-term refinancing operations (TLTRO II), each with a maturity of four years (and which will be carried out from June 2016 to March 2017)

The move came after the collapse of the oil price at the beginning of the year, the sharp decline in equity markets and more broadly, growing risk aversion. In addition, Eurostat has published statistics showing that annual inflation in the Eurozone had returned to negative territory in February 2016 (-0.2% y/y from +0.3% in January¹).

European Central Bank chief, Mario Draghi, said that inflation would remain stuck in that territory over the coming months. The ECB now expects inflation to be just 0.1% this year, from a previous estimate of 1%, and cut its growth forecast to 1.4% this year from 1.7%. He also listed a number of risks weighing on economic growth: struggling emerging economies, volatile financial markets, slow pace of structural reforms. He added that rates will stay very low for a long period of time, suggesting there would be no further cut.

The ECB move is intended to help weaken the euro, boost activity and fight the threat of deflation. Above all, it buys time with the hope that European governments will obtain more budgetary leeway and implement structural reforms.

After reacting negatively, the day of the ECB decisions, due to the suggestion that interest rate would not be cut any further, European stock markets began to recover. On March 11 the Stoxx Europe 600 index was up 2.6% and the euro down by 0.3% against the dollar.

Investors will however monitor carefully the eurozone’s credit and activity indicators. And they are awaiting the outcome of the next meeting of the US Federal Reserve, today, March 16. If US rates were raised (which is not the main scenario), the euro could depreciate further against the dollar and then help eurozone exporting companies. And to a lesser extent benefit the rand.

Negative deposit rates, which are equivalent to a tax for banks, weigh on their profitability. It will be more difficult for them to avoid a cost increase for customers.

The risk that a speculative bubble develops in the bond markets due to inflows of liquidities is increasing. In core euro area economies, government bond yields have dropped significantly while the value of the bonds has strongly increased.

It is far from certain that the ECB move will be sufficient. It cannot act on a large number of factors that affect both inflation and growth (oil market, development of new technologies and population aging). If the last monetary measures were to have little effect on the euro, economic growth and inflation², the ECB could risk running out of ammunition in the future to react to a new crisis.

¹ Energy price went down from -5.4% to -8.0% and core inflation (i. e. excluding energy, food, alcohol and tobacco) from +1.0% to +0.7%.

² For the quantitative easing, its limits and its risks, see “Did quantitative easing work?” – E. Yu - Federal Reserve Bank of Philadelphia Research Department – First quarter 2016.