Could a rise in global manufacturing production signal easing supply chain snarls?

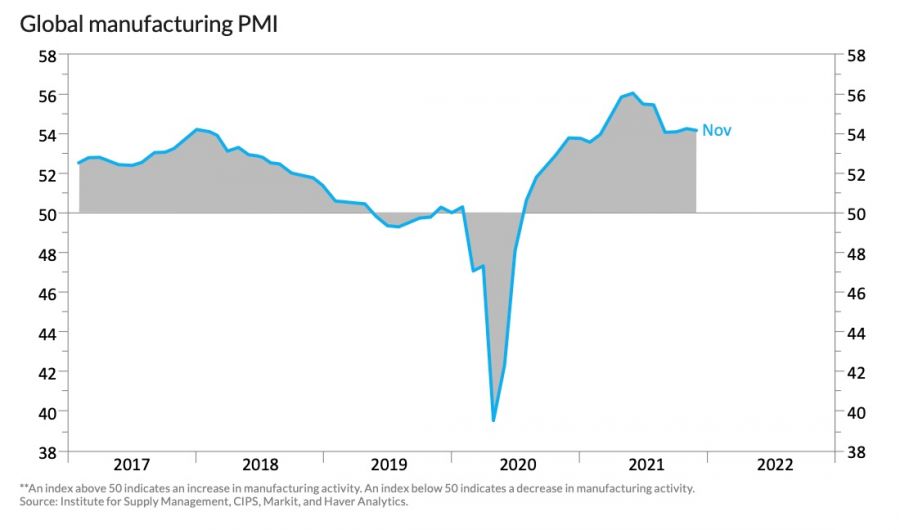

Although the J.P. Morgan global manufacturing PMI compiled by IHS Markit was little changed from 54.3 to 54.2 index points in November 2021, it beckoned a steady growth trend in manufacturing sector business conditions and restored hopes that supply shortages would soon abate.

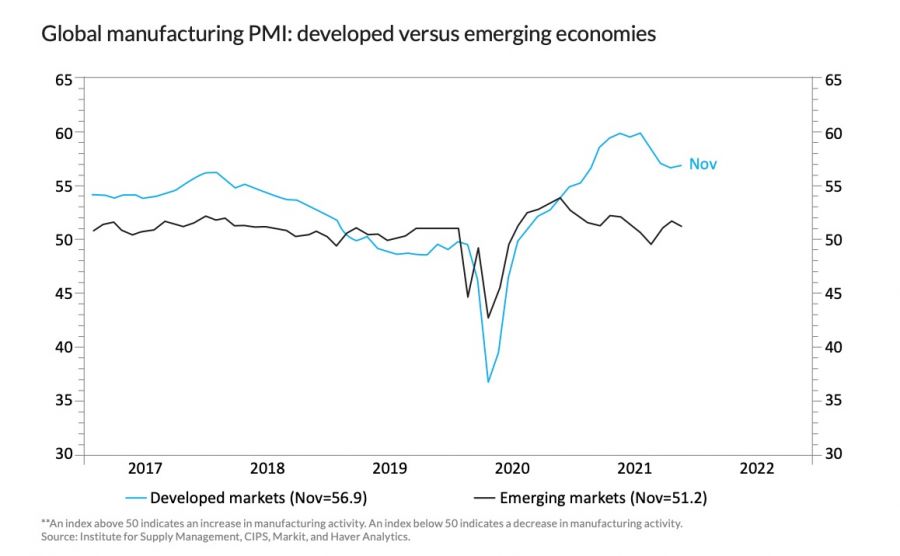

The global output index also rose to 52.6 points in November 2021 - the highest level in more than a quarter as manufacturing activity in most first-world countries continued to improve. According to data from the Institute for Supply Management (ISM), the US manufacturing PMI rose by 0.3 percentage points to 61.10% in November 2021, pointing to a strong expansion in the overall economy since the last contraction was recorded in April 2020. Global Sector PMI data from IHS Markit also depicted an equally encouraging picture as it showed that business activity in most detailed sectors monitored in the US rose in November 2021.

Similarly, Britain’s manufacturing PMI rose from 57.8 to 58.1 in November 2021, defying supply chain disruptions and soaring input prices. Production in emerging Asia remained in expansionary territory over the month, with Japan’s production rising to the highest level in seven months, amid improved demand and export order books. Production in China stabilised, following two consecutive months of output declines. China’s manufacturing PMI came in at 50.1 in November 2021, up from 49.2 in the previous month, data from the National Bureau of Statistics showed.

For the broader Asian region, output grew at the fastest pace in two quarters while manufacturing production staged an impressive recovery from Delta-wave lockdown restrictions in the ASEAN region in November 2021 – pointing to the second- strongest level of output in a little short of 10 years.

In South Africa, the seasonally adjusted Absa PMI rose from 53.6 to 57.2 over the month in focus, signaling a robust expansion in manufacturing activity that was the strongest in five months.

The Bureau for Economic Research (BER) reported that: “Both business activity and new orders rebounded after being severely affected by a prolonged strike action in the steel sector and load- shedding in October.”

The latest Global Economics Update from Capital Economics shows that some companies reported a rise in backlogs of orders and longer supplier turnaround times in November, going into December 2021, suggesting that there may have been some easing in supply disruptions over this period. However, the emergence of the new Omicron variant poses a renewed risk to the outlook for manufacturers, as it could aggravate the existing supply-demand disparity within global manufacturing sectors.

Although we have seen solid economic recovery and growth, there is still a lot of uncertainty in the market, namely, inflation and the Omicron variant. This new Covid-19 mutation has now been found in most countries worldwide, and as the virus spreads, the “noise” surrounding it increases, leaving us with no clear indication of what. to expect. Hence, we look to PMIs.

These are good indicators of the direction of economic trends and conditions. As long as they remain above 50 points, we are still comfortable, even if they do decrease somewhat.