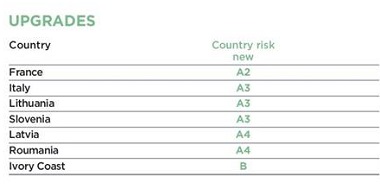

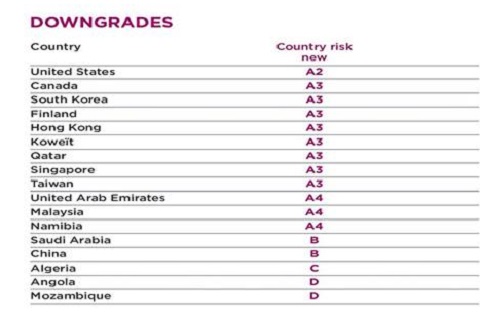

Coface announces 7 country upgrades and 17 downgrades

Good growth figures in Europe, a rebound in many emerging currencies and in oil prices indicate improving economic signs. But the world’s two largest economies, the United States and China, whose country ratings have been downgraded to A2 and B respectively, illustrate the ongoing level of credit risk.

In China, the most widely followed economic indicators such as GDP growth, retail sales and industrial production, show that growth is stabilising, But company insolvencies are growing sharply. In the United States, hidden behind a continuous fall in the unemployment rate, there are companies whose profitability is being eroded and are investing less.

In China, companies are experiencing overcapacity and excessive debt, which will take time to reduce. In the United States, companies' problems are more cyclical than structural. Six years after the beginning of the recovery process from the economic crisis, 2016 has seen a rise in insolvencies for the first time since 2010.

If we add Japan (downgraded to A2 in March), then the world’s three largest economies are experiencing an increase in company credit risk. Unsurprisingly, Asian countries are being negatively affected by the Chinese slowdown, hence the downgrading of South Korea, Hong Kong, Singapore and Taiwan.

Before the British referendum, Europe was the herald of good news. The country assessments of France and Italy have been revised upwards to A2 and A3 respectively, under the effect of falling insolvencies, earnings that have stopped declining and more favourable lending conditions.

Central and Eastern Europe is benefiting from the euro-zone recovery and Romania, Slovenia, Lithuania and Latvia have been reclassified upwards.

In Europe, Coface expects companies to keep their positive growth momentum over the next few months unless the consequences of the British referendum and other numerous political uncertainties intervene.