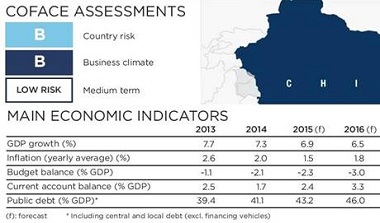

China - 2015 private sector debt accounted for 205% of GDP

Strengths

• External accounts benefiting from industrial

• competitiveness and diversification

• Sovereign risk contained: public debt mainly domestic and denominated in local currency

• Gradual move up-market

• Development of services

• Infrastructure development

Weaknesses

• High volatility in the stock market

• Social tensions linked to rising inequality

• The share of consumption in GDP remains weak: rebalancing the Chinese growth model remains a challenge in the medium term

• Aging population and gradual drying up of the pool of cheap and abundant labour

• Overcapacity in certain industries and high corporate debt

• Fragile Chinese banks (sharp increase in credit growth and deterioration of asset quality)

• Government’s strategy is ambiguous on arbitrating between reform and growth

• Environmental problems

The Chinese economy is expected to continue slowing in 2016. The authorities are implementing reforms needed to rebalance growth in favour of consumption and services. This is however hitting profits of weak companies. Despite the ongoing monetary easing since November 2014 and expansionary budget measures, investment is likely to remain limited in 2016.

As companies are heavily indebted and several sectors are facing large overcapacities, the monetary relaxation is proving ineffective and volatility in the financial markets could undermine confidence amongst investors and consumers. In this context, disposable income should rise slowly and household consumption is likely to slacken somewhat.

Due to the rapid expansion in online sales, retail sales are losing momentum. Although there has been a rise in property prices in the main cities in 2015, construction-related sectors are likely to remain flat because of high inventory levels. A collapse in the housing market is however not likely as the authorities have the capacity to intervene in the event of a severe shock.

Growth in the services sector, in particular financial, is also continuing. Exports are however expected to continue being affected due to the weakness in global demand. Nevertheless, downward pressure on the yuan could improve competitiveness.

Credit risk of companies increasing

Although the level of public debt is sustainable, that of local municipalities is high (at around a third of GDP) and remains opaque. In addition, corporates are highly indebted and the expansion of shadow banking makes it very difficult to evaluate. In September 2015, private sector debt accounted for 205% of GDP. On top of this and despite monetary policy easing, SMEs frequently have to rely on shadow banking at exorbitant rates for loans, given their difficulty in securing financing.

In this context there has been a gradual decline in the quality of banking assets which are also under-estimated because of the scale of shadow banking. The official ratio of non-performing loans reached 1.75% in the first quarter of 2016, its highest level since 2009. Together with “Special mention loans”, this ratio reached 5.76%.

Credit risk has also increased significantly, highlighted by the growing number of defaults on the Chinese bond market. While China experienced its first default in 2014, 24 companies (a third of State-owned enterprises) defaulted in the bond market during the first quarter 2016. Bankruptcy is inevitable. In the context of the economic slowdown, the solvency of more fragile borrowers will need to be monitored in 2016.

Following a rise of more than 110% between November 2014 and June 2015, the Chinese stock markets recorded a significant correction during the summer of 2015. Stock exchanges lost more than 43% in less than three months. In the beginning of 2016, the benchmark index lost 17% before stabilising. Volatility is also high in the foreign exchange market. Admittedly this market correction can be seen as a healthy development. The heavy use of margin finance (investors borrow money to buy shares) has increased credit risk and could worsen the downward spiral.

Business climate continues to have shortcomings

Whilst reaffirming the supremacy of the Chinese Communist Party (CCP), the Central Committee session of the CCP in October 2014 concluded decisions relating to improving in the state of law.

The 5th plenum of the Communist Party, which was held in October 2015, ended the one child policy and reaffirmed the desire on the part of the authorities to develop the social protection system. However, the national security reform project has caused concern among some NGOs and foreign investors.

Despite a seamless transition from the previous administration, President Xi Jinping wields unprecedented authority over the CCP, particularly following the anti-corruption campaign which targeted the highest-ranking party dignitaries. However, the Xi Jinping – Li Keqiang administration is facing both social and ethnic unrest.

The country has seen an increasing level of worker activism which caused the authorities to publish a guide on the development of “harmonious work relations”. Finally, major shortcomings in term of governance persist, particularly in relation to company balance-sheets and legal protection for creditors.