Behind the headlines

If you’ve followed the news recently, you’d probably say that South Africa is falling apart. The fight against organised crime and corruption seems to be going backwards.

However, if you look at local financial markets, there is an upward trajectory. What gives?

Bad news sells

Firstly, we are very lucky in South Africa to have a free press and dedicated investigative journalists working on exposing truths. Many corrupt schemes have been cracked open by brave reporters, and often it is the media that pushes government agencies into action. However, the news doesn’t give the full picture. Negative or shocking headlines will always grab more attention, and attention sells newspapers. You will never see a headline along the lines of “things were fine today”. Yet many things still work well every day in a R7 trillion per year economy of 60 million people. People go to work, children go to school, families celebrate and mourn together, communities gather in churches and mosques and so on. Millions of daily interactions and transactions go unreported because they are unremarkable, but they are also the bedrock of the economy and society.

Secondly, financial markets also do not reflect the full picture. It is only the largest companies that list on the JSE, and sometimes the strong get stronger in tough economic conditions as weaker players fall by the wayside. Good companies don’t need a robust economic environment to be profitable, but smaller firms often do. Moreover, few JSE-listed companies are reliant only on the South African business climate. For instance, the announced merger of Anglo American and Teck Resources will pull Anglo further from its South African roots to being a Canadian headquartered global mining giant. But it will retain its listing in Johannesburg. Of the top 10 companies by market value on the JSE, only Capitec and FirstRand really count as local companies if we consider where most revenues are generated. The biggest property company on the JSE by market value, NEPI, runs an Eastern European real estate portfolio.

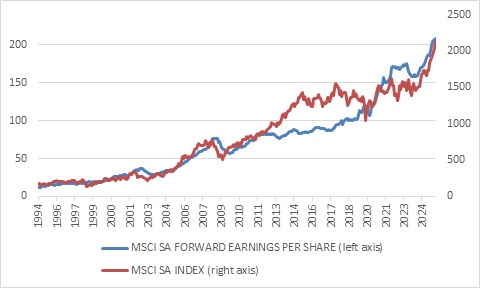

Chart 1: SA equity price and earnings

Source: LSEG Datastream

The hodge podge of local and international firms listed on the JSE is collectively growing profits at a steady pace despite a lacklustre South African economy (more on this below). The surge in precious metal prices clearly helps, with gold up 38% year-to-date and platinum 50%. The gains in local equities this year have been on the back of strong earnings growth, and the bottom-up analyst consensus view is that this continues next year. It means that despite the rally, the local market still trades on an attractive forward price: earnings ratio of around 10x, a starting point that has historically delivered solid long-term real returns.

Bond boost

The bond market, on the other hand, is very much SA-focused since it is dominated by government issuance. The 10% year-to-date return from the All-Bond Index suggests that there is some good news locally. Traditionally, a rally in bonds is not always a good omen, since investors often pile into bonds when the economy weakens and they expect interest rate cuts. This is what has happened to US bonds over the past few days, as weak employment growth numbers point to the Federal Reserve resuming its rate cutting cycle this week. However, riskier investment destinations like South Africa face a different dynamic, especially if they have high levels of government debt. Investors demand compensation for the perceived risk, and that can increase at times of economic weakness when government tax revenues come under pressure. It is a particular curse of emerging economies that interest rates must sometimes rise when there is a crisis to prevent capital flight even if domestic conditions demand lower borrowing costs. The alternative is a disorderly depreciation of the currency.

That is clearly not what has happened in the local bond market. The Reserve Bank has cut interest rates 50 basis points this year, pulling down the short end of the yield curve, while the longer-end of the yield curve has benefited from a broad decline in risk premia across emerging markets as measured by credit default swaps. These credit default swaps spreads do not yet suggest that South Africa’s rating has improved substantially relative to other emerging markets. For this to happen, we’ll need faster economic growth and more evidence of progress on fiscal consolidation.

Click here to read more...