Back to the budget drawing board

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Facing a R50 billion tax revenue shortfall, Minister Gigaba and the National Treasury team only had three options to choose from in preparing the Medium Term Budget Policy Statement (MTBPS). They could try to squeeze more out of a struggling tax base, cut spending despite increasing demands from various quarters, or borrow more, adding to a rapidly rising debt pile. In the end, they chose a combination that favoured the latter. Due to the missing R50 billion, the budget deficit (the difference between spending and tax revenue) will be 4.3% of GDP for the current fiscal year instead of 3.1% as projected in February. This is a massive jump and much worse than expected. The deficit will narrow somewhat to 3.9%, but this will not be enough to stabilise Government’s debt level over the MTBPS’s three year forecast period. Instead, the ratio of debt to GDP will rise towards 60% by 2021.

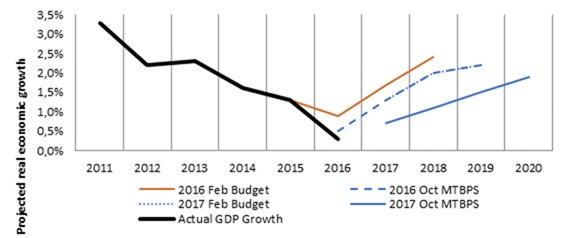

The massive revenue shortfall relative to what was projected in February is largely due to disappointing economic growth. In other words, growth expectations were too optimistic in February. But now the real GDP growth forecast for 2017 and 2018 has almost halved to 0.7% and 1.1% respectively, and growth is only expected to rise to 1.9% by 2020. This could now be too pessimistic. Importantly, since revenue and spending numbers are nominal (i.e. includes inflation), the nominal growth forecast for the next three years was cut from an average of 8% to 6.5%, implying the total size (rand value) of the economy will be smaller than previously thought by 2020. This is partly due to slower than expected inflation. Not only has nominal growth slowed, the amount by which tax revenue grows relative to nominal growth, the tax buoyancy, has also declined.

Not cutting the deficit

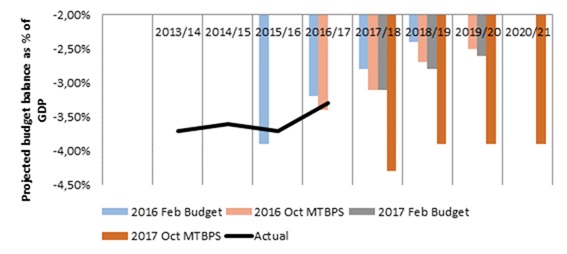

Every fiscal year since 2012, the deficit has ended up bigger than initially expected (though never as much as this year) but Treasury still projected smaller deficits in the outer years of the forecasting framework. This wasn’t just a case of being naively optimistic on its part as economic growth disappointed every year, even against the expectations of private sector economists. Projecting smaller deficits signalled a commitment to fiscal consolidation, even though delivering on it was hard. As Chart 1 shows, there was some progress in narrowing the deficit from 3.7% in 2013/14 to 3.3% in the last fiscal year.

But last week, the Minister took a very different approach. Not only will the deficit jump this year, it will end up larger in 2020 as a percentage of GDP than in 2013 – the opposite of progress. One can infer three reasons for this. Firstly, the cost of imposing fiscal discipline (tax hikes and spending cuts) is deemed too high. Secondly, Minister Gigaba took the approach of being honest and realistic about the seriousness of the situation, saying there would be no “sugar-coating” the state of the economy and Government’s finances. We hope his message was heard as clearly by his Cabinet colleagues as by the markets. Thirdly, lacking the credibility of his predecessor (whom he replaced in the infamous midnight Cabinet reshuffle in March), Minister Gigaba was not really in a position to make promises that things would get better as the market might not have believed him. By slashing expectations, the hurdle for a positive surprise in the future is now lower. And a positive surprise is not impossible given the much stronger global economy.

Debt service costs running ahead

The one lever the Minister could pull, to cut back on spending was not pulled. The stated reason is that spending cutbacks would hurt service delivery, but they are also politically difficult. The fact that the expenditure ceiling, a cornerstone of fiscal responsibility, might be breached this year due to the SAA bailout will be a red flag to ratings agencies. Though small, the breach would send the wrong message, but there is still a longer term commitment to the ceiling – in fact it was lowered slightly.

By allowing the deficit to widen compared to the previous projected path, the Minister is giving the economy some breathing room. But this comes at a cost. As a result of increasing debt, interest payments will grow by an average of 11% per year over the next three years – the fastest growing item in the budget – reaching more than R200 billion in the 2020 fiscal year.

Ratings risk derails rate cuts

In the meantime, the risk of further credit rating downgrades has increased, especially since there is very little fiscal flexibility after the contingency reserve (Government’s rainy day fund) was dipped into. S&P Global and Moody’s have ratings reviews scheduled for 24 November. Fitch already rated Government’s local and foreign currency debt as junk, but still noted its concern that the budget signalled a shift away from commitments to cut deficits and debt.

Apart from the deviation from the fiscal consolidation path, the biggest issues from a ratings point of view are the State Owned Enterprises (SOEs). The MTBPS did not shy away from the fact that weak governance was the cause of underperformance at SOEs, including Eskom. Lenders are increasingly and justifiably reluctant to roll-over debt of SOEs, and Government might have to step in with additional funding as a result, a further risk to the fiscus. The Minister was clear that Eskom posed an enormous risk to the economy, and admitting a problem is the first step towards recovery, as they say.

Encouragingly, asset disposals and private sector participation are being discussed, but the words need to be translated into action. Apart from new boards at SAA and the SABC, very few concrete measures have been implemented. But the SAA case also shows that lenders are increasingly making their voices heard and are forcing through reforms. This is also a positive development.

Global backdrop still key

There is also a global context. Low global yields have made South African bonds attractive despite our fiscal challenges. Before the MTBPS foreigners had been net buyers of R70bn worth of bonds (net selling since the speech has been around R10bn). Central banks are gradually removing stimulus, and as long as the pace is measured and well signalled, developed market bond yields are unlikely to jump much, keeping investor interest in emerging market bonds (including SA) alive. The European Central Bank embarked on the long road to monetary policy normalisation when it announced a reduction in its monthly bond purchases (known as quantitative easing or QE) to €30bn from January. However, to soften the blow, it will extend the programme until September, while also promising to keep short-term interest rates, at present negative levels, well past the end of its QE programme.

Global economic growth has picked up materially. Last week saw US economic growth accelerate to 2.25%. South Africa has historically followed the global cycle, though it underperformed the global economy over the past two years. Therefore, Treasury’s growth forecasts could be too low for once. Unless something has fundamentally changed in the relationship between growth and tax revenue – for instance, if tax compliance has deteriorated – tax revenues could surprise on the upside again.

But to reap the full benefit of stronger global growth, weak confidence needs to be addressed, but it was always unrealistic to expect too much from the MTBPS since political uncertainty and instability at the Cabinet level play such a big role in depressing the country’s growth rate. While the MTBPS laid bare the economic situation, the political context in which this MTBPS was presented is obviously not static, and can change after December.

Unfortunately, given the downgrade risks and the fact that fiscal policy will not be tightening, the SA Reserve Bank is unlikely to proceed with interest rate cuts.

Looking for silver linings

There are three silver linings. One, expectations have been considerably lowered, making an upside surprise possible. Two, there was no allocation to any nuclear power build, and Minister Gigaba was explicit in saying the country could not afford it now. Three, while the MTBPS was negative for markets, taxpayers got off fairly lightly and consumers should view it positively. Only R15bn of additional revenue is pencilled in for next year, much of it can be gathered stealthily through bracket creep.

Investment implications

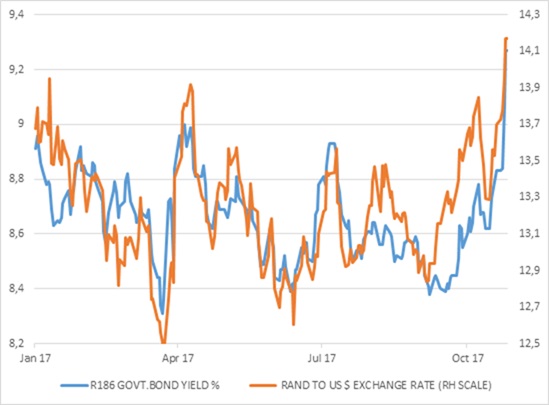

Markets are moved by surprises, and the lack of planned fiscal consolidation was a surprise (the revenue shortfall not so much). The immediate market reaction saw the rand sell-off and bond yields rise. The rand and local bonds had been weakening since mid-September due to a firmer dollar and rising US bond yields as US tax reform prospects gained momentum.

Markets have now reset expectations and further downgrades are being priced in. Investors should therefore be cautious of a knee-jerk reaction, selling out of South African assets when they have already repriced. Also remember that the JSE benefits from a weak rand, and it is still a strong month for domestic equities (5%), though financial shares were negatively impacted. Bonds have clearly had a torrid month, with the All Bond Index extending losses and down 2.6% for the month, with the return for the year now lagging cash.

There is still much uncertainty, and this calls for appropriate diversification. The sell-off in bonds means yields are even more attractive relative to other SA assets as well as global bond yields. There are clearly risks to the country’s fiscal landscape and the prospect for interest rate cuts has diminished substantially. But there are also risks to being too pessimistic (for instance by having too much rand-hedge exposure) since positive political developments could easily see the rand rally and bonds surge. More than ever, cool heads are needed, on the part of both policymakers and investors.

Chart 1: A much bigger projected budget deficit

Source: National Treasury

Chart 2: Slower projected economic growth

Source: National Treasury

Chart 3: The market reaction, bond yields up and the rand down

Source: Datastream