A longer wait for rates relief

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

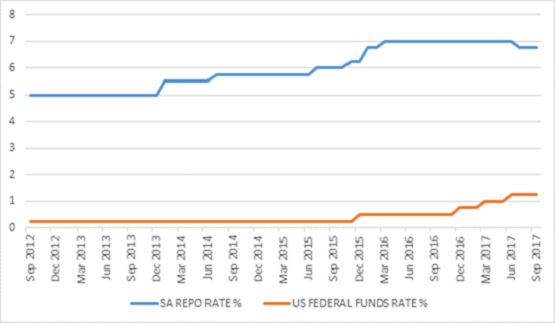

The past two weeks have been eventful, especially on the monetary policy front. The American and South African central banks held interest rate setting meetings within hours of one another. While the officials of the US Federal Reserve (the Fed) might not even have known that their South African counterparts were making an interest rate decision, the members of the Reserve Bank’s monetary policy committee (MPC) are acutely aware of what Fed chair Janet Yellen is doing.

Interest rates unchanged

Both meetings resulted in unchanged interest rates. In the case of the Fed, this was widely expected and the focus was mostly on the announcement that it would start gradually shrinking its balance sheet, starting this month. In several rounds of quantitative easing (QE) since 2008, the Fed bought trillions of dollars of bonds and mortgage-backed securities to stabilise the banking system, inject liquidity and reduce long-term interest rates. Up until now, the Fed has reinvested interest and the proceeds from maturing bonds, keeping the size of its balance sheet stable at around $4 trillion. It will now allow $10 billion a month to mature without reinvestment, and this amount will gradually rise until the balance sheet is shrinking by $50 billion a month by late next year (which means it would take seven to eight years to fully unwind the impact of QE). QE was an unprecedented monetary policy experiment, and reversing it, albeit very gradually, also comes with a set of unknown potential outcomes. However, the Fed is aware of the risks, has clearly signalled its intentions to avoid surprising the market, and can hit the pause button if at any stage it feels it needs to.

Market-derived probability of a rate hike in December has increased to almost 80% over the past two weeks, but the more important point is not the exact timing of rate increases, but the overall direction. In their so-called dot plots where Fed officials present their individual forecasts, short-term interest rates are expected to eventually peak at 2.75%. This “terminal value” has declined from about 4% in 2012 when the dot plots were first published, a remarkable decline in the assumed neutral interest rate (the interest rate that is neither too high nor too low for a normally-functioning economy). The previous five hiking cycles topped out at 6% on average.

In a separate speech last week Yellen confirmed that she was eager to raise interest rates to more normal levels, arguing that low inflation was likely temporary, and that inflation would rise to the Fed’s 2% target over the next few years. But she admitted that the Fed wasn’t entirely sure why inflation has been persistently low despite the rapid decline in unemployment. The traditional model of central banking assumes that declining unemployment pushes up wages and, eventually, prices. But this process seems to have broken down, in part due to the globalisation and technological advancements that reduce the pricing power of business and labour. As if on cue, US inflation data released on Friday once again came in below expectations (1.4% year-on-year).

US interest rates matter for the entire global economy and world markets. The process of pricing in the path of future monetary policy will cause volatility from time to time, but there is still no reason to expect interest rates to shoot up, choking off the economic recovery and derailing markets.

Another attempt at tax reform

Separately, the White House finally put some detail to its long-awaited tax reform plan, releasing a framework that includes a proposed reduction in the corporate tax rate cut from 35% to 20%. Another component would encourage US multi-nationals to bring back billions of dollars stashed abroad through a once-off levy. US equities jumped on the news. However, whether the tax plan can make its way through Congress is still debatable, despite Republican control of the legislature, as several failed attempts at repealing former president Obama’s healthcare law have demonstrated. Current budget rules dictate that tax cuts will need to be offset to avoid the deficit from increasing, and cannot be permanent. Squaring that circle will be challenging.

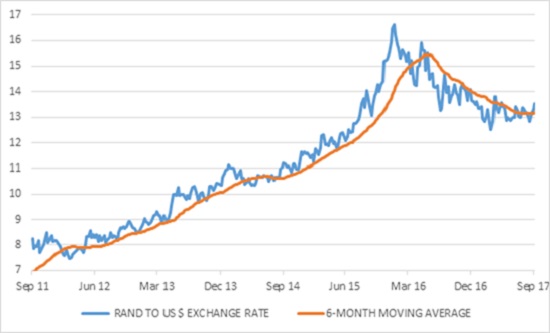

The slightly more hawkish Fed and the tax proposals gave some support to the dollar, which has been struggling this year, hurting gold and other commodities in the process. (Central bankers that favour rate hikes are termed “hawks” by financial commentators, while “doves” are those in favour of lower rates.) The euro also weakened, following the strong showing of the far-right AFD party in Germany’s election, while the unofficial Catalan independence vote in Spain also caused uncertainty. This has seen the rand weaken to around R13.50 per dollar, but it is still within the broad trading range of the past year. In other words, while volatile, the rand has essentially been moving sideways for a year. One consequence is that currency appreciation is not wiping out the gains from offshore investments for local investors.

No rates relief from the Reserve Bank

In contrast to the Fed, the MPC surprised by not cutting. Three members were in favour of a cut and three against. (Although we don’t know which members favoured cuts, the eventual outcome suggests that Governor Kganyago was against cutting.)

The case for a rate cut was strong. Inflation is within the target range (and expected to remain there). Headline consumer inflation was 4.8% in August, slightly higher due to the petrol price hike, but core inflation (excluding fuel, food and electricity prices) fell to 4.6%, the lowest level in five years. While meat inflation is still rising at the shops, it has peaked at the farm level and will eventually filter through to consumers. The final estimate of the 2017 maize crop was increased last week to a record 16.7 million tonnes, more than double that of last year’s drought-hit harvest. Import prices, excluding oil, declined by 11% year-on-year in July (the latest month for which we have data), another disinflationary force. Finally, South Africans’ assessment of future inflation is also declining. A survey of expected inflation in five years’ time by the Bureau for Economic Research fell to 5.6%, the lowest level since the survey started in 2011. Meanwhile, the economy is still weak and beleaguered consumers need all the help they can get. Consumer borrowing grew by a mere 3.4% year-on-year in August.

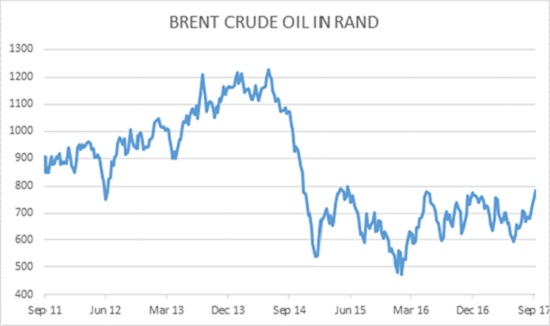

The Reserve Bank’s own forecast of inflation was unchanged, but the MPC instead focused on everything that could go wrong: oil, meat prices, Eskom’s application for a 20% tariff increase and of course, uncertainty on the path of US rates. The oil price jumped further after the MPC meeting on geopolitical concerns and is now at the highest level in a year in rand terms. While this will put some upward pressure on the consumer price index, it is still well below where it was three years ago (chart 3).

The risk of further downgrades amid political uncertainty and an unhealthy fiscal picture also appears to weigh heavily on the cautious MPC. Simply put, the MPC seems to fear another rand blow-out that will lead to galloping inflation. This ignores the fact that the exchange rate has a much smaller influence on inflation than in the past. It also ignores the fact that the rand is more or less fairly valued against the dollar now, while it was overvalued when its five-year collapse started in 2011. Similarly, the dollar remains historically expensive, so its upside is surely limited.

Further rate cuts are unlikely to spur a consumption boom. Consumer confidence is still low and households probably wouldn’t use lower rates to borrow much more. But it will relieve some pressure on households and increase optimism levels, especially since the tax burden is likely to rise over the next year.

Chart 1: US and South African policy interest rates %

Source: Datastream

Chart 2: The rand-dollar exchange rate

Source: Datastream

Chart 3: Brent crude oil price in rand

Source: Datastream