A Grexit and its impact

Rafiq Taylor from Sanlam’s multi-manager business.

Greece’s debt continues to be its Achilles heel, as it attempts to escape an economic slump.

What happened on Monday?

Greece’s debt continues to be its Achilles heel, as it attempts to escape an economic slump. This has been exacerbated by this weekend’s events which saw Greek Prime Minister Tsipras not being able to negotiate terms with its major creditors: the IMF, the European Central Bank and the European Union. Tsipras has called for a referendum on 5 July and Greece missed its 30 June debt obligation, after not reaching agreement on new terms for funding needed by Greek banks. The banking system has subsequently shut down, with customers limited to withdrawals of €60 per day.

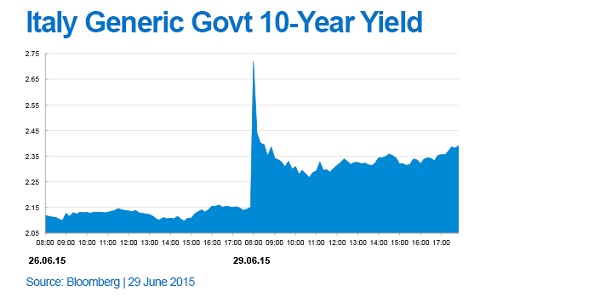

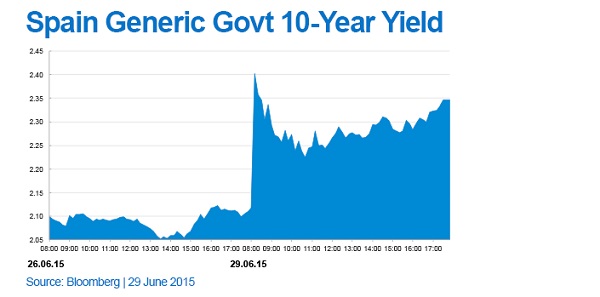

This has created anxiety not only for the EU region, but also for Greece’s creditors’ and global capital markets. Across the board, markets opened down on Monday, with the Euro Stoxx 50 index being hardest hit, losing more than 3%, but the S&P 500 limiting losses to 0.70%. Natural safe havens, such as developed market bonds (German bonds in particular), as well the US dollar and gold, were popular investment destinations given the volatility that accompanied this weekend’s news. Subsequently the contagion has spread to other EU countries, such as Spain and Italy, where lending rates have increased, given their debt burden.

Closer to home, the All Share Index opened 2% down and bonds yields rose marginally by 0.1%. The rand remained resilient at around R12.20 against the dollar and did not move much throughout the day. SA equity ended the day 1.27% down, which displayed some investors buying into weakness.

What would a Greek exit mean for investors?

In short, the turmoil of the last week is largely a storm in a teacup. One needs a bit of perspective here. Had this been 2011, this would certainly have been a much bigger issue and the contagion would have been much more drastic than the limited downside we saw on Monday. A Greek exit would surely be more severe for Greece than for the European economy as a collective, with Greece contributing a mere 2% to European GDP.

It is in these times that sticking to our investment philosophy (being longer term in nature) and our considered process is key to managing short-term volatility, however unpleasant these paper losses may be. This market “correction” provides underlying managers with the opportunities needed to create long-term wealth for you and we remain convinced that we have the right strategy for each portfolio we manage on behalf of our clients. We continuously review the portfolios and research the fund management landscape for new ideas and fund managers with significant talent and skill. This we believe should ensure we meet your objectives over the time horizon pertinent to you.