DFM key to helping planners meet post-COVID client demands

It may be too early to paint a clear picture of life post-COVID-19, but there's an overwhelming expectation that this 'black swan event' will result in fundamental changes to the economy.

According to Kim Rassou, Portfolio Manager at Old Mutual Wealth Tailored Fund Portfolios, the wealth management industry will not be immune, and the outbreak of COVID-19 could rewrite the books as many historical assumptions are now being questioned. "Going forward, financial planners will need to practise great fiduciary care when advising clients where and how to invest their money."

She says that the pandemic will place asset managers and financial planners under increasing scrutiny as many clients will still be reeling from steep declines. "The impact of COVID-19 can be explained only as an extremely rare event that has had severe consequences for the global and local economy, of which nobody could have predicted," says Rassou.

"South Africa was particularly vulnerable even before it went into this crisis. This, coupled with depressed confidence, the recent downgrade and high levels of government debt, means that there is much uncertainty around the impact of the virus and the long-term consequences thereof."

Relying on the past becomes almost impossible as "no financial models are available to forecast the impact of this unprecedented event — suggesting that professional asset managers will be put through their paces to make informed investment decisions based on new data," says Rassou.

"The virus brought along serious shocks to the global economy — including soaring unemployment, major manufacturing slowdown to the point of factories being shut down, consumer spending nearing to a halt due to restrictive lockdown conditions, and a crash of both equity and bond markets as investors sell off liquid assets to escape market volatility.

"Fund managers will need to find a balance around capital protection, managing risk and looking for investment opportunities when at this stage is unclear as to how long this volatility is expected to persist," says Rassou.

She says that navigating the world post-COVID-19 will stretch even the most seasoned financial planner. "Past performance is never a predictor of success, but this is without doubt true post-COVID-19.”

“To match investment risk to a client objective, control of the asset allocation is key. Because retail fund managers are only required to make their holdings available in arrears, this results in the planner making decisions based on stale information and therefore not being able to make timeous and accurate decisions if they wish to be actively involved in the process," says Rassou.

Extreme market volatility and uncertainty means that financial planners can no longer rely on their own investment process or look only to past performance to make portfolio recommendations. "Portfolios are usually linked to a specific, expected real return and a minimum investment period to create a portfolio, suitable asset classes must be selected, and long-term strategic asset allocation should be developed," says Rassou.

She says that by using a professional Discretionary Fund Manager(DFM), financial planners can make informed real-time investment decisions in a better attempt to position the portfolio based on prevailing current market conditions.

"Financial planners can rely on the expertise, experience and data available to their DFM to make informed decisions on how to position the overall client portfolio to best meet the client's investment objective, mitigate risk and seek out opportunities to add value to the portfolio when most markets are trading at a 20% discount," says Rassou.

With experience in manager research, selection and asset allocation based on a building block approach, a DFM will keep financial planners informed and understand precisely what risks and opportunities their portfolios are exposed to as they receive direct feedback from the asset manager.

"In addition, short-term tactical asset allocation can reduce investment risk and enhance returns if performed skillfully. Through using a well-resourced DFM, you can combine fundamental valuation research with economic insights to derive suitable tactical weights for your portfolios in an ever-changing environment.

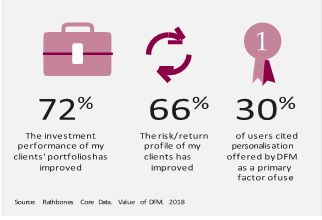

We expect South Africa to closely follow the trend of adoption of the DFM model as in the UK. According to a UK based company, Rathbone Investment Management report, in 2018, 72% of financial planners saw an improvement in overall investment performance and 66% noticed an improved risk/return profile for clients after working with a DFM.

Rassou says that Old Mutual Wealth's DFM capability is built on this specialist multi-manager approach: planners have access to portfolios that incorporate both active and passive management strategies and instruments that "provide a packaged model portfolio solution tailored to the client's investment objective while controlling overall risks and costs," says Rassou.

The added advantage for advisors is that they can leverage Old Mutual Wealth's scale and reach to lower overall management costs.

According to Rassou, the increasing use of DFMs in the retail space in the UK has driven down fund manager fees. This symbiotic relationship between them and advisors is having the added effect of raising financial planners' reputation.

With the introduction of RDR, planners are required to continually understand and interpret investment markets, which means that soon they would have to do investment research to make relevant recommendations to clients before they can give investment advice.

"These industry changes have been happening for some time now, but I think the COVID-19 crisis is going to accelerate the rate of change and challenge the way the industry has functioned to date. Everyone will have felt the impact of the global shutdown, and the subsequent collapse in markets will showcase the value of having the backing of a DFM as I have little doubt that every client will be reviewing their investment portfolio," Rassou concludes.