Taking the mystery out of Prescribed Minimum Benefits

Gail Gibson, CFP®, Financial Services and Compliance Specialist and FPI Health Competency Committee Member.

Prescribed Minimum Benefits (PMBs) is one of the key areas that could cause conflict for the medical scheme, medical scheme advisor and member with the consequence of consumers removing business from brokerages and insurance houses annually.

Why PMBs matter to you?

As a financial advisor, you should not give medical advice to your clients, but you do need to know what should be covered by the medical scheme.

Underwriting and PMBs

The highest rate of expense with any disease or disorder is normally at the investigation stage followed by the subsequent stabilisation of the PMB condition. Measures are in place to protect schemes from opportunistic behaviour such as a member joining the scheme only to treat such a health occurrence.

Schemes may protect themselves from covering a PMB for a new member by imposing general waiting periods of three months and a condition-specific 12 months waiting period. A late joiner penalty for new members over 35 years of age may also be applied. The legislation does not force schemes to apply waiting periods or late joiner penalties, but they must have a policy which can be shown to treat all members fairly.

A medical scheme can make a benefit conditional on the member obtaining pre-authorisation or joining a benefit management programme. This is an additional way for the scheme to manage costs and normally provides a better level of care for the patient, who additionally learns to manage the problem.

Digging deeper into a PMB

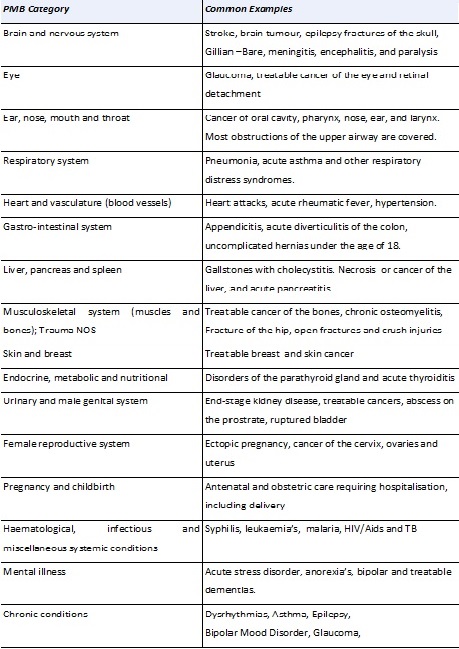

PMBs can be roughly divided into 15 different categories consisting of more than 270 conditions (table 1 below) that qualify for cover. These are diagnosis-specific; however, the medical scheme does not have to pay for diagnostic tests that establish that a person is not suffering from a PMB condition. This means the member may well have to cover the cost of such test in their personal capacity. PMB diagnosis, treatment and care can be received wherever it is most appropriate, including a hospital, clinic, and outpatient setting or even at home.

The importance of diagnosis and PMBs

When dealing with PMBs, medical schemes are most concerned about the diagnosis, and not on how the condition came about. For example: a patient contracts septicaemia after cosmetic surgery, the scheme has to provide healthcare cover for the septicaemia part because septicaemia is a PMB. The cosmetic surgery itself will remain an exclusion.

Reimbursement for a PMB condition

The International Classification of Diseases and Related Health Problems (10th revision) or ICD 10 codes are of prime importance with regard to PMBs for re-imbursement by the schemes. These codes provide information on the condition diagnosed and enable the medical scheme to determine what benefits the member is entitled to and how these benefits could be paid.

Regulation 8 (1) states the scheme payment must make full provision for the treatment of a PMB and the requirement for that payment is from risk benefits only, not from the member’s day-to-day account. This regulation exposes the scheme to risk where the service provider will charge excessively for PMB services or up-code.

The scheme appointment of designated service providers (DSPs) and managed care protocols, is to mitigate the risk of this “blank” cheque practice by some healthcare providers. Financial advisors should ensure that their clients understand the scheme can charge member co-payments if they do not comply with such provisions when it comes to the supply of chronic medication and choice of provider.

What is an emergency?

Emergency treatments are defined as a sudden, and at the time unexpected, onset of a health condition that requires immediate medical or surgical treatment. The failure to provide such treatment would result in serious impairment to bodily functions or serious dysfunction of a bodily organ or would place a person’s life in serious jeopardy.

If doctors suspect that the patient suffers from a condition that is covered by PMBs, the medical scheme has to approve treatment. Schemes may request that the diagnosis be confirmed with supporting evidence within a reasonable period of time.

Legislation and future developments

The following issues are presently in discussion:

• The legislation is not very well written, giving rise to much confusion in this area.

• Some industry experts believe the PMBs cover the wrong benefits.

• There is concern that the process of discrimination on the basis of diagnosis is unconstitutional.

• ICD 10 codes are not considered to be accurate enough to determine if a treatment should be a PMB classification and medical providers use them to guarantee payment from the schemes increasing the downside risk which schemes face from members.

• Lower income medical schemes benefits are being specified in terms of services rather than with diseases in the PMB package.

How can this work for the financial advisor?

The astute financial advisor can view ongoing medical scheme education in PMBs as a marketing and relationship building tool which would add value to your clients and your practice. For example, the financial advisor could have an article encouraging the use of “Designated Service Providers” (DSP) contracted into render PMB services by explaining that this usage will not prematurely exhaust day-to-day savings on their websites.

When clients receive good health care on an ongoing basis their general wellness improves, resulting in fewer serious conditions that has shown to improve health and longevity. This correlates to a long term beneficial client relationship.

References:

https://www.medicalschemes.com/medical_schemes_pmb/objectives.htm

Health Care in South Africa by Liz Still 2009 ISBN 062034516-X

Health Care in South Africa by Liz Still 2011 ISBN 062034516-X