“National Savings Month” and your medical scheme

Brian Watson, Genesis Medical Scheme.

“National Savings Month” is an awareness campaign run by the South African Savings Institute (SASI). July is always the month in which the national savings awareness campaign is run. It was first launched in 2001 by the then Finance Minister, Trevor Manuel. SASI aims to cultivate an environment of savings among all South Africans.

July is National Savings Month

With such a large portion of the average person’s income that is used to service debt, savings can be problematic if you spend more than you earn and in order to “make ends meet”, you use an overdraft facility or credit card, which charges high interest rates.

Just how can you save during these difficult times?

A lot of families are struggling financially. Property rates have increased, electricity (when it works) has increased and is likely to carry on increasing with the weak rand and interest rates are going to increase – not “if, but “when”.

Being a consumer is a tough business to run.

Medical cost savings

Doctors are permitted to charge patients whatever they like. They are running a business and they can do that.

Medical schemes, on the other hand, are also running a business of sorts. Their job is to reimburse claims according to a tariff, or scale of benefits (we won’t go near PMB for purposes of this article). All too often, the medical schemes reimbursement does not cover what the doctor charges and the patient/member must cover the shortfall.

This situation often leads to great unhappiness.

For those that are fortunate enough to belong to a medical scheme (and battling to pay the monthly contributions), the following two tips may be worth your while to consider. Not only can it increase your monthly disposable income, but it will at the same time ensure that you are covered for the “big ticket” events such as big accident, hospitalisation or major illness and disease.

1. Opt for a hospital plan

Irrespective whether you are on a basic hospital plan, or on a very expensive executive option with generous out-of-hospital benefits, most medical aid scheme benefit options will usually cover your hospital and related accounts in full.

Using your medical aid benefit option to fund your day-to-day medical expenses such as doctors consultations or medication, is a very expensive way of using your own money (via a savings account that your medical scheme administers on your behalf) to fund these type of expenses. Irrespective your benefit option, your scheme will fund your in-hospital expenses once approved; so why pay more to occupy the same bed in hospital?

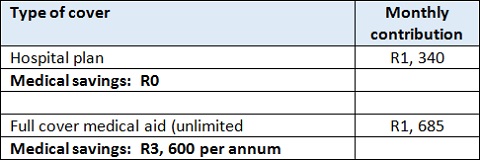

An example:

The following table demonstrates the cost vs savings benefits of a “hospital plan” compared to a “full cover medical aid”, per single adult member, on Genesis Medical Scheme.

The in-hospital cover and other risk benefits for both above benefit options are exactly the same. The only difference is in the amount of day-to-day benefits (savings). Opting for the hospital plan will cost R345 per month, or R4, 140 per annum, less. So by having the exact same “risk benefits” you would have R345 x 12 = R4, 140 per annum to save, or to use for your day-to-day expenses, as opposed the R3, 600 if your scheme has to administer your savings.

It therefore makes a lot of sense to select a good hospital plan and let your scheme carry the risk of insuring the “big ticket” expense items, while you fund your day-to-day expenses on an as and when basis.

2. Negotiate discounts

Many doctors, in order to avoid the costly hassle of dealing with the medical schemes, offer patients a discount if the account is paid at the time or within 30 days.

Most members ignore this offer because “my medical aid will pay for it”. The problem is that the medical scheme is not aware that this discount is being offered despite the fact that it has to by law settle accounts within 30 days of receipt.

The result? The member may be left with a larger than necessary co-payment.

An example

Take the case of a prominent gynaecologist who charged R3, 080 for a hysteroscopy and D&C (dilation and curettage of the cervix). Genesis Medical Scheme, that reimburse claims on its 3 top option at a generous 200% of scale of benefits, would reimburse the claim for a total of R1, 353. The shortfall that is payable by the member is R1, 727.

Now, unbeknown to Genesis, the doctor offered the member a settlement discount price of R2, 580 (R500 or 16%) if the account was settled within 30 days.

Look at the math:

Amount that Genesis will pay = R1 353

Amount charged by doctor = R3 080

Shortfall for member to pay = R1727

However, if the member settles the account herself, she will reduce the co-payment or shortfall by R500. The answer is to settle the account yourself and then submit proof of payment to your medical scheme that will then reimburse you. That way you will have saved R500 by being pro-active.

It is your choice

It is clear from the above example that this particular doctor is charging patients 225% more than the Scheme tariff. Put differently, the doctor charges almost 5 times more than the old National Health Reference Price List (“medical aid rate”) adjusted for inflation each year.

Sound too high for you? Well, you have the freedom of choice to consult with any doctor that you choose. But, if you consult an expensive doctor and/or you do not negotiate his tariff, you will probably be in for high co-payments. That said, by being pro-active you can take advantage of any discounts offered to help you save.