Employers apprehensive about the imminent rise in their healthcare costs

2015 Medical Scheme Increases: For the employer - It is about the spread of the employees

- “Low” and “High” cost medical scheme options to be hit hardest by medical scheme contribution increases

- Even a single digit increase for employees could be a difficult pill to swallow given lower salary increases

- Employers with bulk of members on High Cost (i.e. comprehensive) and Low Cost income options may see some double digit increases

Employers across South Africa are apprehensive about the annual increase announcements from the Medical Schemes, due in October. According to Toska Kouskos, Head of Healthcare Consulting at NMG Benefits; “Most medical schemes will probably aim for single digit increases of approximately 8-9%.”

“However, even a single digit increase could be scant relief for employers especially with salaries growing at a lesser rate. Employers should really be considering the mix of options and plans they offer employees. This will determine the average increase in their healthcare budget, ignoring the 3-4% of members who buy up or down each year.”

Most open medical schemes offer a basket of benefit options catering for the distinct needs of different segments of society and the employee base. Comprehensive plans are generally aimed at those needing “richer” benefits, whilst lower priced plans cater for people on lower incomes.

The details matter says Kouskos; “In this case we must consider the effect that loss ratios have on the decisions taken by medical schemes. A medical scheme may announce an average increase but in reality the loss ratios at the top and bottom benefit plans are typically higher than the middle options. The situation is of course made worse when the majority of employees are placed on the top and bottom options of a medical scheme. These employers will feel the pinch most of all.”

A loss ratio is the difference between the claims of a member against the contributions that a member pays to the medical scheme. If a poor loss ratio for a benefit option is ignored one year then it must be corrected by the medical scheme eventually. “We have seen corrective action in the past from schemes where income categories on lower cost options have been amended to cater for this risk”, says Kouskos.

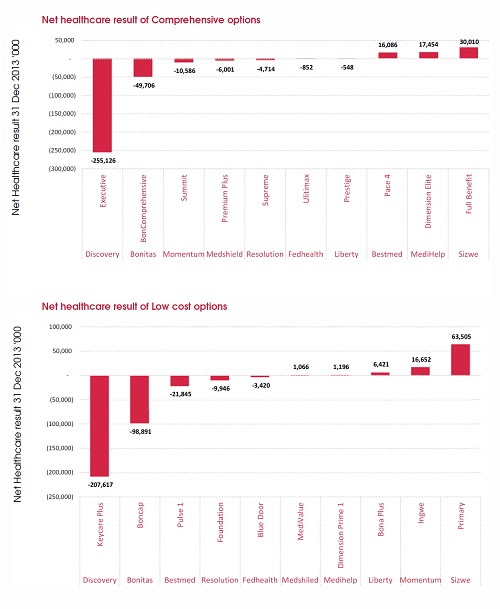

Data from the Council for Medical Schemes (CMS) Report released earlier this week reveals a gloomy picture with regard to the net healthcare result of the comprehensive options and lower cost options in 2013.(see attached)

GRAPH

“We can expect that schemes will respond to their loss ratios on the top and bottom options; either through changes in contributions or through modification in benefits. Some may rely on their provider networks and managed care arrangements to assist managing this risk.”

“Not all schemes differentiate between the different options when they introduce increases. However, schemes that do differentiate will cost accordingly. Employers with the bulk of members on comprehensive or low income options may see some double digit increases,” concludes Kouskos.