Private Healthcare: the widening gap between what you think you're covered for and what you're actually covered for

Why gap cover is an essential shield against financial devastation in South Africa's private healthcare system

“You may think that my use of the term ’devastation’ is overly emotional or exaggerated. I can assure you, it is not. I have witnessed firsthand the financial devastation some medical scheme members have been subjected to due to inadequate, inappropriate and sometimes unaffordable healthcare cover.” Martin Rimmer, CEO of Sirago Underwriting Managers.

Every year, thousands of South African medical scheme members walk out of private hospitals with something they did not expect: a serious bill not covered or only partially covered by their medical scheme benefits based on their specific option, from the specialists who treated them.

In most instances, specialist doctors charge rates well above what the medical scheme benefit pays for in-hospital treatment. The result is a tariff shortfall, also referred to as the medical scheme tariff/rate, that the member must fund personally.

This is the reality of private healthcare in South Africa, and it is precisely why gap cover exists. Claims data from Sirago Underwriting Managers shows just how significant these shortfalls are and why, regardless of your medical scheme option, gap cover should be considered an indispensable part of your private healthcare funding strategy.

The Regulatory Framework: Why Gaps Exist at All

South Africa's private healthcare system is governed primarily by the Medical Schemes Act, overseen by the Council for Medical Schemes (CMS). The Act requires all registered medical schemes to fund a defined basket of Prescribed Minimum Benefits (PMBs) - a set of serious conditions and emergency events, at cost, meaning the scheme must cover the full cost of treatment, regardless of what the healthcare provider charges. PMB management is incredibly complex, as the rules, while universal, are applied differently by the medical schemes.

Whether a condition qualifies as a PMB, how the scheme interprets its protocols, whether a Designated Service Provider (DSP) is involved, and whether the treating specialist has a tariff agreement with the scheme all affect the amount actually paid.

The payment rift lies in specialist tariffs. Unlike the pharmaceutical sector, where medicine prices are regulated under the Single Exit Price mechanism, there is no regulatory ceiling on what a healthcare specialist may charge in South Africa. Specialists are free to set their own fees, and in a market characterised by acute skills shortages and growing demand, many charge rates that are 200% to 500% higher than what medical schemes reimburse. There are even some outliers where the tariff rates are 800% higher than the scheme payment.

The scheme will only ever pay its contracted rate. The specialist charges their preferred rate, even if they are contracted with the schemes. The difference is the tariff shortfall, and it lands in the member's lap.

Medical Scheme Membership Is Not Full Cover

There is a widely held and potentially very costly misconception that belonging to a medical scheme means your in-hospital treatment is fully covered. It is not. Most medical scheme options reimburse in-hospital specialist fees at a fixed percentage of a reference tariff, commonly referred to as the Scheme Rate or Scheme Tariff. But these benchmarks have not kept pace with actual market charges, and a specialist billing at 500% of tariff will leave even a member on a 300% reimbursement option facing a 200% shortfall on their own account.

Beyond tariff shortfalls, medical schemes can/also impose:

• Co-payments: Fixed amounts a member must pay for certain procedures.

• Sub-limits: Annual caps on specific benefits, after which the member funds further treatment.

• Benefit exclusions: Certain treatments or procedures that schemes do not cover at all.

• PMB interpretation gaps: Where a diagnosed condition is not recognised by the scheme as a PMB under their protocols, even if it is clinically serious.

Gap cover is a short-term insurance product regulated under the Short-Term Insurance Act, specifically designed to bridge the shortfall between scheme reimbursements and actual healthcare provider charges for in-hospital events. It does not replace a medical scheme but works alongside it as supplementary cover.

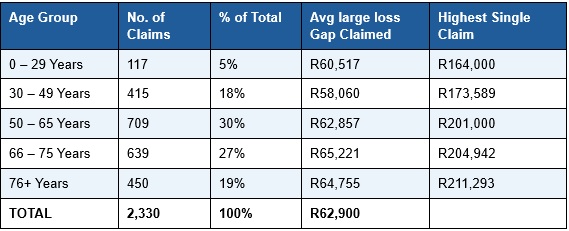

A Snapshot of Real Gap Claims

To understand just how severe these shortfalls can be, consider the following analysis of gap cover claims paid by Sirago Underwriting Managers across a representative sample of 2330 large loss claims between 2020-2025. (A large loss claim is defined as R50 000+).

23% of all large loss gap claims are from members aged 49 and under - people who statistically believe themselves to be young and healthy.

In almost half of Sirago’s large-loss gap claims in 2024, gap cover paid out more than the medical scheme did. In one case, gap cover paid R126,771 while the medical scheme paid only R27,573 - just 18% of the total treatment bill. The member's medical scheme premium was R8,000 a month. Their gap cover premium was R450. Without that gap policy, they would have been personally liable for R126,771.

Click here to read more...