New legislation offers health insurance policyholders better protection

Roseanne Murphy Harris, President of the Actuarial Society of South Africa.

New legislation impacting health insurance offers policyholders better protection by mapping out clear rules on exclusions, waiting periods, benefits and commission. Falling under the Long-Term and Short-Term Insurance Acts, the demarcation regulations affect all gap cover, hospital cash plans and primary healthcare policies entered into or renewed after 1 April this year.

Roseanne Murphy Harris, President of the Actuarial Society of South Africa, states that the primary aim of the demarcation regulations is to establish firm boundaries between medical aid schemes and the different types of health insurance products.

“Confusion over the benefits offered by health insurance policies versus medical aid schemes has unfortunately resulted in consumers inadvertently sacrificing adequate medical cover by opting for products not appropriate for their circumstances,” she says.

“This confusion also restrained medical schemes from developing a broader and more sustainable membership pool, which is crucial for the financial wellbeing of schemes.”

By introducing clear boundaries the regulations aim to prevent health insurance policies from interfering with the business of medical schemes. Product providers are also obliged to communicate clearly to policyholders that health insurance policies, especially hospital cash plans, are not a substitute for medical scheme membership.

The regulations have therefore introduced new guidelines for the benefits payable by gap cover and hospital cash plans, while primary healthcare policies are expected to transition into medical aid schemes in the next two years.

New cap on gap cover benefits

Murphy Harris notes that one of the primary changes introduced by the regulations is the new benefit cap on gap cover, which may help to counter escalating healthcare expenses.

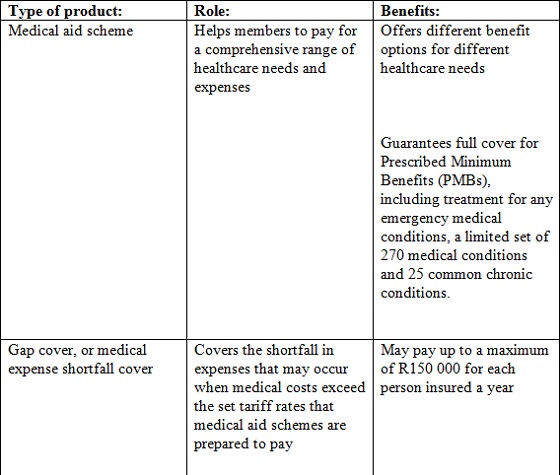

Also known as medical expense shortfall cover, gap cover is intended to address the shortfall in medical expenses that may arise when medical costs exceed what medical schemes are prepared to pay.

“Some healthcare specialists may increase their charges according to how much insurers will pay. This in turn has the effect of contributing to medical inflation,” she explains.

Gap cover has now been capped at a maximum of R150 000 for each insured person per year.

Restrictions on hospital cash plans

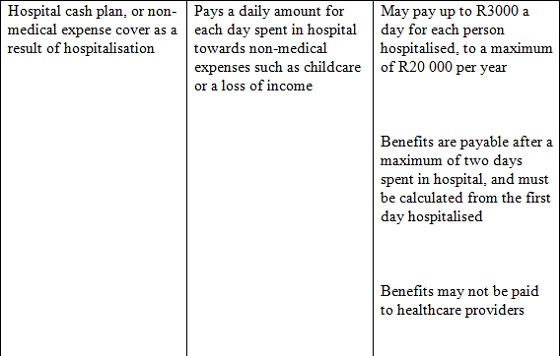

Hospital cash plans are intended to pay a daily amount towards non-medical expenses that might arise when an individual is hospitalised, such as childcare or a loss of income.

“However, these policies are often used as low-cost options by earners who mistakenly believe that the benefits will cover the costs of hospitalisation, leaving them without adequate medical protection,” says Murphy Harris.

“Moreover, many hospital cash plans only paid benefits after policyholders had spent as many as four or five days in hospital, which only happens in rare cases.”

Hospital cash plans have therefore been limited to paying up to R3 000 for each day spent hospitalised to a maximum of R20 000 a year. These benefits may not be paid or ceded to healthcare providers.

The new regulations further stipulate that benefits should be paid after a maximum of two days spent in hospital, and must be calculated from the first day hospitalised.

Transition to low cost benefit options

One of the biggest changes enacted by the demarcation regulations will see primary healthcare policies transition to medical aid schemes over the next two years, due to the fact that these products are considered to perform the business of a medical aid scheme.

Primary healthcare policies offer policyholders a limited range of healthcare benefits, such as visits to general practitioners and emergency medical care.

“However, insurers are able to apply for a two-year exemption under the regulations in order to protect the rights of policyholders, as these policies target low-income earners who are often unable to afford medical schemes,” she says.

She notes that further consultation with the Council for Medical Schemes (CMS) and the Department of Health will take place over the next two years in order to address the framework for low cost benefit options under medical schemes. This option will be used to better accommodate low-income earners at the end of the two-year period.

“The CMS published a draft framework for low cost benefit options in 2015, and although there were some issues with the structure of these options, I believe that this framework represented a good starting point for further engagement,” says Murphy Harris.

Consumer protection guidelines for all health insurance policies

Other rules introduced by the demarcation regulations for the protection of consumers include:

• Commission:

Commission payable to insurance brokers on health insurance policies has been limited in order to prevent the misselling of products.

Commission is now set according to monthly premium bands, ranging from a maximum of 20% of premiums less than R300 per month, to a maximum of 5% of premiums above R1 200 per month.

• Premiums:

Insurers are prohibited from discriminating against individuals by refusing them cover or increasing their premiums on the basis of their state of health, because they have a disability or because they are pregnant.

However, insurers may price premiums based on the age of the policyholder when taking out a contract, provided that this pricing affects all new policyholders of the same age.

• Waiting periods:

Insurers may impose a general waiting period of up to three months on policyholders before they are able to make a claim, as well as a condition-specific waiting period of up to 12 months.

This would apply to individuals that have been diagnosed with or sought treatment for an illness or condition in the year preceding the date they take out a new policy.

• Disclosure:

As part of the Treating Customers Fairly (TCF) principals adopted by the financial services industry, the terms of policies, the premiums payable, as well as any restrictions on benefits must be disclosed when taking out a policy.

Regulations may encourage innovation

Finally, Murphy Harris adds that insurers are often reluctant to offer products in an uncertain legal environment, as this uncertainty means that they may not be allowed to offer the same policies in the future.

“These regulations mean that more insurers could begin to offer healthcare policies, and we could see more competition and cheaper and more innovative products in the healthcare space.”

Comparison of medical schemes and health insurance policies: