Navigating the 2024 medical scheme hikes for the gap cover business

As we approach the new year, South African medical scheme members are confronted with the imminent changes in contributions and benefits set to take effect on January 1, 2024.

The escalating costs of healthcare in the country pose challenges for both medical schemes and their members, necessitating innovative solutions for managing affordability without compromising on quality care.

Understanding the landscape

In the face of the 2024 medical scheme contribution increases, it is crucial for intermediaries to guide clients through the intricacies of healthcare financing. The diverse drivers of these increases, as illustrated below, demand a strategic approach to balance solvency, financial requirements, and member needs.

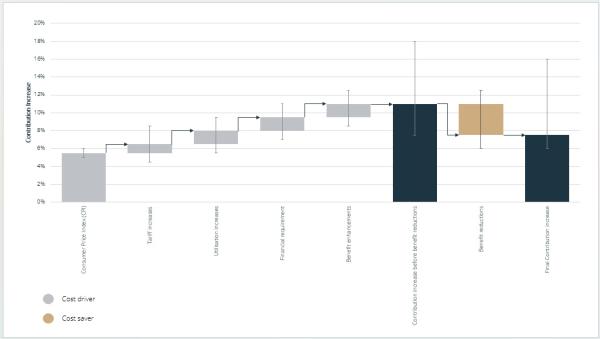

The graph above shows the following:

• The starting point for medical schemes is the Consumer Price Index (CPI) to serve as the basis for inflation. While being an apparent metric to start off with, the determination thereof is not so clear. The Council for Medical Schemes published a recommended 5.0%, but each medical scheme can take a different approach, whether considering backward-looking CPI or forecasting forward-looking CPI. As a result, we have seen medical schemes using a CPI assumption in the range of 5.0% to 6.0%.

• Tariff increases are in most cases negotiated and we have seen these ranging from 1% to 3% above CPI, depending on the negotiation strength of the medical scheme and the healthcare service providers.

• Utilisation increases must be incorporated in the medical scheme contribution increases, adding an increase of 2% to 3%, to allow for the additional healthcare demand as the membership profile ages.

• Contribution increases are also influenced by financial requirements, adding an additional 1% to 3% to the contribution increase, to cater for solvency adherence, loss-making benefit options and/or historically insufficient contribution increases.

• When medical schemes introduce new benefits, the associated cost is allowed for in the contribution increase, and we have seen a few schemes enhancing their benefit packages, contributing to an additional 1% to 3% increase.

• Although a rare occurrence, medical schemes can reduce benefits to soften the blow on the contribution increase and this particular year we have seen medical savings account allowances reduced, eroding the value for money.

Addressing affordability challenges

With industry-average contribution increases ranging from 7.5% to 16.0%, members are grappling with affordability concerns, prompting potential downgrades and benefit limitations. These limitations, such as sub-limits and network restrictions, lead to inevitable out-of-pocket expenses for members.

In response to these challenges, gap cover has emerged as a practical solution to restore the value of members' money. Businesses that provide gap cover services must provide a comprehensive safety net, offering benefits such as coverage for approved admissions, shortfalls for specialist consultations, and access to a wide network of facilities.

Financial intermediaries' role

Recognising the challenging economic climate, financial intermediaries play a pivotal role in advising medical scheme clients. Rather than abandoning or switching schemes due to affordability constraints, the recommended approach is to supplement medical aid with gap cover. This strategic move ensures uninterrupted coverage with no waiting periods or breaks in cover.

Despite the rising cost of healthcare, maintaining coverage is paramount. Intermediaries are instrumental in helping clients strike the right balance between affordability and comprehensive coverage. By staying informed about healthcare funding market developments and working closely with clients, intermediaries ensure their clients remain healthy and financially secure.