Gap cover claims grow in shortfall quantum during 2020

Musculoskeletal, connective tissue and circulatory conditions were some of the key drivers of mega gap claims in 2020

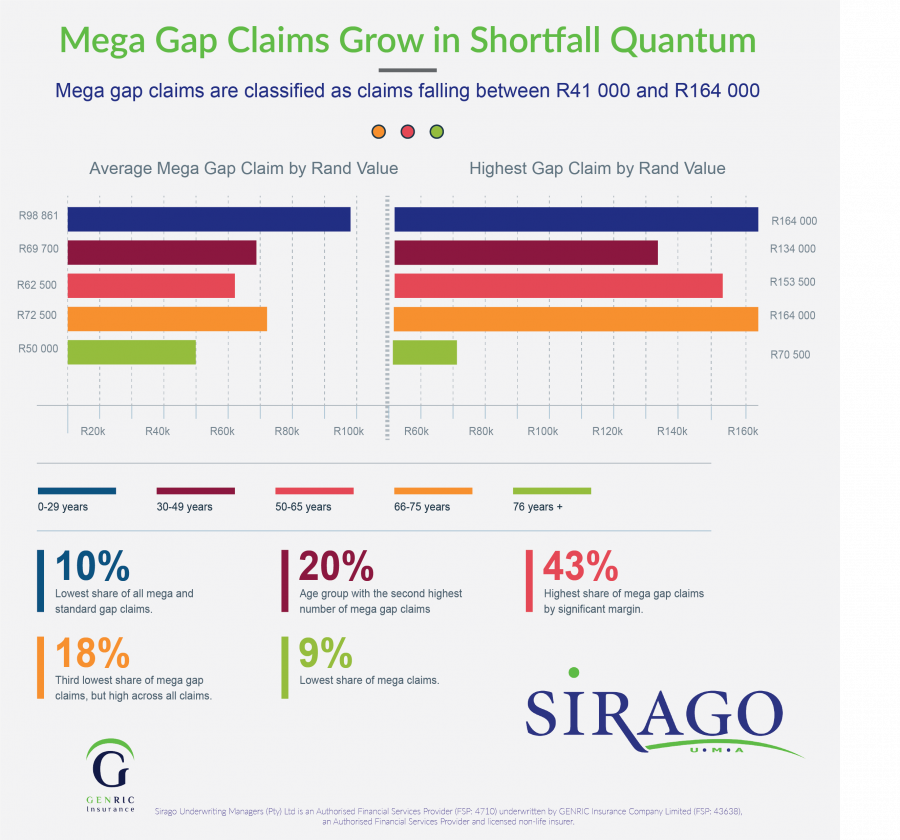

An analysis of gap insurance claims paid by Sirago Underwriting Managers during 2020 shows that not only are average gap claims values rising, but large or mega gap claims are also increasing in frequency, with large shortfalls ranging between R41 000 and R164 000 for in-hospital treatments not paid by medical schemes. Of the thousands of claims processed in 2020, Sirago paid in excess of 100 mega claims – internally classified as upwards of R40k per claim – totalling some R5.1 million in shortfalls not covered by policy holders’ medical scheme options for these mega claims alone.

At an average of just over R50 000 per claim and measured against an average premium of R450pm per policy, it means these policy holders have claimed approximately 9,2 years’ worth of premiums paid or still to be collected – demonstrating the crucial role that Gap Cover plays in healthcare financial planning and protecting policyholders from large and unexpected costs which they would need to self-fund if they did not have gap cover in place.

Gap insurance covers the difference that arises from the rate that healthcare specialists charge for in-hospital procedures versus what a medical scheme pays.

An analysis of ‘mega’ claims (R40k-R164k) paid by Sirago during 2020 shows notable trends:

• The age band with the highest average mega gap claim at R98 861 is 0-29 years old. Claims causes related to congenital malformations and chromosomal abnormalities (birth-related conditions), circulatory system and musculoskeletal conditions. The largest claim was R164 000 and all claimants in this age band were males. While this is the largest average claim cost, it is the smallest percentage of claims in the mega claims category.

• The age band with the second highest average gap claim at R72 500 is 66-75 years old. Claims relate predominantly to musculoskeletal and connective tissue conditions. The highest claim was R164 000 and in terms of gender, the split is 50/50.

• The third highest average gap claim value of R69 700 is in the age band 30-49 years with claims mostly relating to musculoskeletal and connective tissue conditions. The highest claim in this age band was R134 000. In this category, 67% of gap claimants were male.

• The age band 50-65 has the highest number of mega claims by a significant margin, with an average gap claim of R62 500 and claims relating to musculoskeletal and connective tissue conditions, neoplasms (cancer), circulatory system and digestive system conditions. The highest claim was R153 500 and the gender split was 50/50.

• The age band with the “lowest average” of R50 000 but still registering as a mega claim, is 76+ years. Claims causes relate predominantly to musculoskeletal/connective tissues and circulatory conditions and gender split is 50/50. The highest claim in the age band was R70 500. In terms of overall claims ratio however, this is still the largest claiming group across all claims, including mega claims in terms of ratio of policyholders to claims value.

The age bands are ranked as follows in terms of total mega claims frequency and value:

|

Age band |

Number of mega claims (as % of the 100 mega claims in 2020) |

Average Claim Amount |

% of total Rand value of mega claims paid in 2020 |

|

0-29 |

6% |

R98 861 |

10% |

|

30-49 |

20% |

R69 700 |

20% |

|

50-65 |

45% |

R62 500 |

43% |

|

66-75 |

17% |

R72 500 |

18% |

|

76+ |

12% |

R50 000 |

9% |

“Notable trends include the increase in the number of mega claims registering anywhere between R40k to R164k during 2020. Until recently, claims of this magnitude were the exception, but are now becoming more common. If you consider that when gap cover was first introduced as a financial solution to medical scheme shortfalls, gap claims averaged between R2000 to R8000. However, in the last 24-36 months, large claims of R40k+ are increasingly a daily occurrence,” explains Martin Rimmer, CEO of Sirago Underwriting Managers, a gap insurance provider underwritten by GENRIC Insurance Company Limited.

“It also seems that the knock-on effect of delaying other elective surgeries and preventative health checks in the first half of 2020 were marked, with doctors and patients playing ‘catch-up’ in the latter half of 2020 when they realised the pandemic was going nowhere and they could no longer delay the required medical interventions. In some instances, these delays have meant more costly treatments as prognoses worsened due to delayed health interventions,” adds Rimmer.

What should be of significant concern is the relatively young age of most mega gap claimants, both in volume and claim value. Combined, the two age bands between 30-65 represent 65% of claims volume and 63% in terms of total mega claims value paid. When compared to the premium age bands as contained within the portfolio, this is however representative of the population.

“And it is certainly not only members on lower benefit options that are facing these shortfalls – even on comprehensive, top of the range medical scheme options, members are facing onerous tariff shortfalls for in-hospital procedures. This is also driven by affordability issues as a direct result of the pandemic – many members have been forced to downgrade medical scheme benefits to more affordable options and then take up gap cover to protect themselves from shortfalls for in-hospital procedures,” says Rimmer.

It is evident that Gap Cover is a non-negotiable part of any individual and or employer’s healthcare strategy, regardless of age. A single gap claim of R60k would be the equivalent of around 11 years of gap premium payments at 2021 premium rates, and not too many households can afford a major financial knock like this due to a health crisis in the current environment. Most notable is that while medical scheme contributions increase every year, the benefits are in some instances actually decreasing, while healthcare costs are increasing by much more than inflation annually. This places a double burden on consumers who not only will be forking out more for the same or less medical scheme cover, but will also shell out for greater out-of-pocket healthcare expenditure than ever before.

On a closing note, Rimmer advises consumers to always negotiate the pricing of any planned surgery with healthcare providers before and ask for a formal quote from all the medical role players – from the surgeon to the anaesthetist. That way there are no surprises or unexpected costs creeping in after the fact, unless there were specific complications during the procedure. “Given the fact that most elective surgeries were put on hold for a few months due to COVID-19, impacting the incomes of many healthcare providers, there are valid concerns from the insurance sector that overcharging may heighten in the coming months as a means to make up for lost, or delayed income. Be wary of providers asking you upfront whether you have gap cover or not – changing of billing protocols based on a client’s insurance portfolio is a growing practice by some unscrupulous medical providers looking to capitalise on the patient’s insurance cover by overcharging, knowing that the patient has the insurance to cover the inflated price, ultimately having a serious impact on the long-term affordability of Gap Cover solutions,” concludes Rimmer.

Sirago Underwriting Managers (Pty) Ltd is an Authorised Financial Services Provider (FSP: 4710) underwritten by GENRIC Insurance Company Limited (FSP: 43638), an Authorised Financial Services Provider and licensed non-life insurer.

Apr 2021 - Mega claims stats Infographic