Resigning from your job to get your hands on your retirement savings - short term gain and long term pain

Desperate times call for desperate measures. When money is tight and debt is high, people will think of any reason to get their hands on their retirement fund benefits, even before they are actually supposed to start drawing on it. It is not surprising that many people see resigning from their employers as the solution to their cash-strapped dilemma when they heard the rumour that Government is going to stop them from accessing their retirement fund benefits before their actual retirement. Add to this the other rumour that Government is going to nationalise retirement funds, and you suddenly see all the signs pointing towards your early exit from your retirement fund. How else can we as members of retirement funds make sure that our money remain ours? Where else can he get money to settle our debts now? Forget about saving for “one day”; the only thing that matters now is “today”.

It is this short term focus that lands members in the murky waters of debt and eventually being unable to retire comfortably. South Africans are notoriously poor at saving. The Minister of Finance, Nhlanhla Nene, shared some horrific statistics in his parliamentary statement on retirement reforms and rumours on 4 September 2014. In 2013, South African households’ savings rate was a mere 1.7% of Gross Domestic Product (GDP), while our household debt is currently around 75% of our disposable income. In the early 2000s it was 50%. Further to this, less than 10% of South African workers will be able to retire comfortably.

According to various web references, Chancellor Otto Von Bismarck of Germany, designed the first-of-its-kind social insurance program with a defined retirement age of 70 in the early 1880s, after which the retirement age was reduced to 65. Back then most people died in their 40’s. Thanks to the ongoing improvements in nutrition, public health and medical technology, we now live longer. If we use the same logic as Von Bismarck, the retirement age should now be around 103. Yet we are moving in the opposite direction.

Most recent industry surveys show that the average retirement age for new employees is 63, with the retirement age for many corporate employers being as low as 60. As attractive as it sounds to retire at an age when one can still enjoy life, the fact is that we will in all likelihood not be able to do so due to financial constraints. Only 29% of retirees are able to maintain their standard of living in retirement. Instead of being able to do all those things planned for “one day when I retire”, of the more than 300 pensioners surveyed, 1 in 5 works part-time to supplement their retirement income. Increasingly, after their retirement, pensioners also have to maintain more than just themselves and their partners. More and more pensioners have to financially support their children and in some cases, even their grandchildren as a result of unemployment and HIV/Aids. Some are also taking care of their parents. The survey showed that 12.4% of the retirees surveyed have adult dependants other than their spouse and 21.6% have child dependants. No wonder then that South Africans experience a shortfall between their income and expenses in retirement.

Members of retirement funds need to save as much as they can during their working life in preparation for what awaits them after retirement. It begs no argument then that allowing them to get access to their retirement fund benefits before their actual retirement should be strongly discouraged. The following example illustrates the impact of preserving one’s retirement benefits versus taking it in cash when you resign before retirement.

When the member of the retirement fund preserves his retirement benefit when he changes jobs

Member starts working at age 25.

His retirement age is 65.

His pensionable salary is R200 000p.a.

His initial contribution rate is 12%.

Salary inflation is 6% p.a.

Investment return is 10% p.a.

His retirement benefit at his normal retirement age is R22 008 333.

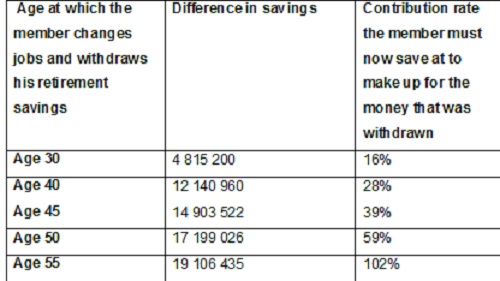

When the member withdraws his retirement benefit when he changes jobs

If the member, for example, resigns at age 45, takes his withdrawal benefit in cash and starts contributing from scratch again, he will have to contribute at a rate of 39% to make up for the R14 903 522 in savings that he lost as a result of the withdrawal. He would also incur a tax liability of R644 513, which could have accumulated to R4 335 961 at retirement. Put differently, if the member contributes at the same initial rate of 12%, his expected retirement benefit at age 65 will be R7 104 811. This is less than one third of the R22 008 333 which he would have received had he not made the withdrawal.

Many people have caught onto this reality and less people are taking their full withdrawal benefit in cash when they changed jobs. This came down from 70.4% in 2011 to 62.4% in 2013 and 54% in 2014. Although this is a move in the right direction but it is not enough. Government will have to step in. And they will do so. This much is clear from the documents published by National Treasury around retirement reform.

But, and this Nene made very clear, as much as “Government would like to see members preserve their retirement benefits until they retire, Government has not changed the law to force members to preserve until retirement”. This rumour is just not true. It was also confirmed that when preservation does become law, whatever the member has saved in his retirement fund up to that point, he will still be able to get full access to if he resigns. It will only be the contributions after the date that preservation does become law that will be subject to the preservation rules. Members should therefore not use this as the excuse to resign with the intention of prematurely getting their hands on their retirement benefits. Resigning from your job to do so not only means that you use money that should have been saved towards your retirement, but also that you leave the safety net of having a job and a steady income in favour of joining the ever-increasing unemployment line. Is it really worth giving all of that up just to sort out your current cash-flow problem?