It’s important to guide employees towards more suitable medical aid plans, especially in a tough economy, says GTC

Jill Larkan, head of Healthcare Consulting at GTC.

Now is the best time to conduct annual reviews of your company’s medical aid plan.

As the South African economy stumbles into a recession, everyone is feeling the added pressures of increasingly having to reign in monthly living expenses. Employers can assist their staff during these tough economic times by conducting a detailed review of the organisation’s chosen medical aid and healthcare policy, ensuring employees are guided towards plans which may be more suitable to their needs and which are most cost effective.

Latest statistics from Stats SA reveal that South Africa’s economy shrank by 0.7% in the first quarter of 2017, moving the country officially into a recession. Stats SA “technically” defines recession as a period when at least two quarters of consecutive negative growth are experienced.

“By reviewing a company’s medical aid plan, employers will be able to do a complete analysis of the existing membership, make recommendations regarding changes possible within the scheme, or even consider alternative schemes which may be more cost effective overall,” says Jill Larkan, Head: Healthcare Consulting at financial services company GTC. “Concurrently companies need to carefully consider the context of the difficult economic climate which will no doubt also affect medical aid selection criteria.”

In terms of the medical aid component of an employee benefits scheme, Larkan notes: “The process starts with a collation and review of membership usage patterns, covering aspects such as Medical Savings Accounts, Above Threshold Benefits, Chronic Illness Benefits and hospitalisation events experienced over the past 12 month period. Afterwards, an appointed healthcare consultant should be tasked with sourcing the more cost-effective and suitable cover for the employees.”

Larkan says that there are various ways to gain the most cost-effective benefit from existing medical aid plans, including:

a) Members can be downgraded to more cost effective plans, reducing levels of in hospital cover;

b) Top-up or Gap covers can be added to existing plans, extending in hospital cover levels;

c) Members can downgrade to a Network plan option; or

d) Members can be offered combinations of Hospital plans and Primary Care networks which may also be more cost effective.

The process of reviewing a company’s medical aid plan is time consuming as it requires staff intervention at many stages, such as during the initial investigation to assess satisfaction levels with the existing plans, presentations regarding alternate plans, the completion of application forms and delivery of new medical aid member cards (if required) by year end. With staff interaction a priority during this process, it’s important that the reviewing project begins typically around June or July each year. Companies which may not have started their annual reviews still have enough time to do so, because the final decision deadline to confirm the transfer of an employer group from one medical aid to another is only in September. Where there are proposed changes, staff consultation processes do need to begin as soon as possible to ensure that enough time is given to individuals to make informed decisions timeously.

Larkan adds that in order to assist employers in making the right decisions regarding medical aid comparisons, GTC Healthcare conducts an annual Medical Aid Survey which analyses and ranks every open medical aid in South Africa. Premiums and the Council for Medical Schemes’ Annual Report on performance and demographics are combined, resulting in an inclusive indicator of better performing plans per category. This information provides employers with the opportunity to “tick” the necessary boxes in their annual Employee Benefits risk management analysis, ensuring that good corporate governance is adhered to, and even more importantly employees’ interests are met.

Larkan also advises organisations to consider consulting with a qualified team of healthcare advisors when conducting this process.

“Qualified, professional advisors are integral to this important annual review as they are able to carefully guide you through this complicated and detailed investigation,” she concludes.

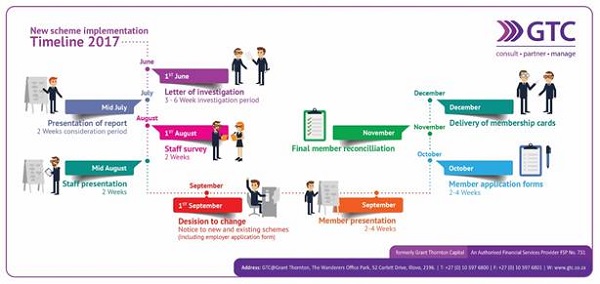

GTC’s graphic below highlights the standard turnaround time for employers to review medical aid plans and to consult with staff. If the exercise hasn’t begun, there is still time, though action is required very soon.

The above infographic describes the following timeline:

1. Letter of investigation 1 June (3 – 6 week investigation period – open plans)

2. Presentation of Report mid-July (consider report)

3. Staff survey (First 2 weeks of August – who would like to consider alternate plans / brokers)

4. Staff presentations (Last 2 weeks of August)

5. Decision to change (1 September) – Notice to existing and new plans

6. Employer application form (1 September)

7. Member presentations September (2 – 4 weeks)

8. Member application forms October (2 – 4 weeks)

9. Reconciliation of membership movements and forms (1 November)

10. Delivery of new membership packs and cards (November/December).