Are your employees paying too much for retirement savings?

Michelle Acton, principal consultant at Old Mutual Corporate Consultants.

How to ensure the best fee structure for your company umbrella fund.

Different umbrella funds structure, calculate and charge fees in different ways – each of which have various impacts on the retirement savings of different members.

Cost savings is one of the key reasons companies are increasingly choosing umbrella funds over managing their employees’ retirement savings themselves (in what is known as a stand-alone retirement fund). Michelle Acton, principal consultant at Old Mutual Corporate Consultants, says that employers should gain an in-depth understanding of the various umbrella funds’ benefits, fees, charges and other costs to assess the merits for and impact on employee retirement savings in the fund.

“The proliferation of umbrella funds in South Africa in recent years and the vast range of product features and fee mechanisms has made it increasingly difficult to conduct a simple like-for-like cost comparison between umbrella funds.”

She adds: “Employers need to tread carefully when assessing fees and doing comparisons as cheap is not always best. Employers should rather select the fund that best suits the company and benefit structures and provides the best chance of achieving the long term objectives of their employees.”

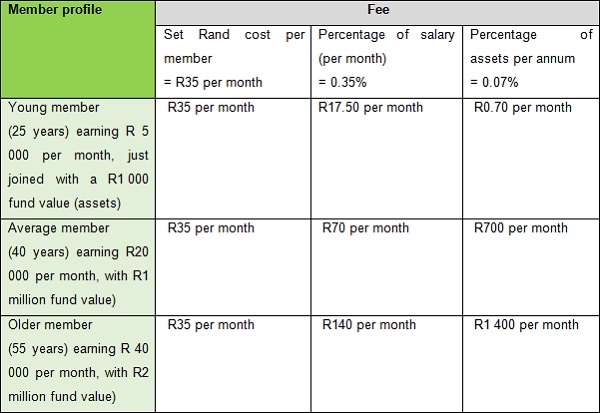

She explains the main costs involved are for administration, governance, consulting or advice and investment management, and that some of these fees can either be calculated as a percentage of assets, while others are based on a set Rand cost per member or a percentage of salary.”

She points to a simple example to illustrate the different impact of varying fee structures: “Let’s assume there are 200 members in the company fund, a total of R10 million in assets and an average salary of R10 000 per month per person. We will also assume that the umbrella fund charges R5 000 per month for administration and R2 000 per month for consulting and advice services, thereby R7 000 in total.”

Should each member be charged a fixed rand amount per month, each member would pay R35 per month for administration and consulting services (R7 000 divided by 200). If the fees were charged as a percentage of each member’s salary so that the total charges for the scheme still add up to R7 000 per month, each member would be charged a fee of 0,35% of their monthly salary (R7000/(200 x R10 000)). If however the fees are calculated as a percentage of assets, each member would have to pay 0,07% per month of their accumulated benefit (their total retirement savings in their fund)(R7000/R10 million). (Refer to Table 1)

Table 1: Different fees structures and effective monthly rand amount charged for members at different ages and earning levels

All three examples would provide the same total revenue to the umbrella fund, but the figures in the table clearly illustrate how the various charging methods impacts members differently depending on their age and earning level, says Acton.

“While charging a fixed rand fee per member per month is generally quite benign in terms of impact on retirement savings, the fees charged as a percentage of payroll are helpful to avoid lower income members from carrying a relatively heavier burden in terms of fees.

“A fund with a mixture of low and high income earners might choose to have a fee as a percentage of payroll with higher earners effectively cross subsidising lower income earners – this is quite common in South African umbrella funds.”

One of the biggest impacts on cost will be the level of flexibility and customisation within the umbrella fund, but Acton says that it isn’t uncommon to find a combination of two or more types of charging methods in an umbrella fund’s structure. “This can make cost comparisons even more difficult, but is sometimes necessary to maximise member retirement outcomes.

“While a single fee might seem appealing and simpler, it might also be more expensive for some members’ benefits. It is therefore critical to balance the level of flexibility required to meet members’ needs (for retirement) with the costs associated with that flexibility.”

Another challenge that Acton points out is that some fees are more transparent than others. “It’s vital to dig into the detail of each fee and understand exactly what is included in each fee that you are quoted on and also what fees might not be disclosed, such as investment management fees.”

Acton concludes that costs do matter and keeping them as low as possible matters too, but it’s not as simple as choosing the lowest or simplest fee. “Making a good decision that makes sense for members is always a fine balance between quality of service, flexibility of options and cost. The most important thing that an employer can do is gain a thorough understanding of the services being offered, along with their associated costs. Employers should be encouraged to speak to an experienced consultant who can help them through this process.”