Supply side will limit the oil windfall

Alex Smith, FNB Economist.

? SA GDP growth is forecast to rebound to an average of 2.5% in 2015 ? We expect inflation to slow to an average of 3.5% in 2015 on the back of a falling fuel price and weaker food inflation ? The moderating inflation profile indicates that the SARB is likely to leave interest rates on hold for the duration of 2015, but should resume the hiking cycle in 2016 ? The current account deficit is expected to narrow in 2015 as import growth slows ? A gradual narrowing of the current account deficit implies that the Rand/US Dollar exchange rate should depreciate only modestly in 2015

Global backdrop

The divergence in prospects for the world’s major economies continues to be a key feature of the global macroeconomic landscape. There is more evidence that economic activity in the US is picking up while the outlook for Europe and Japan remains uninspiring. China’s growth rate is also under pressure. We expect the differing growth trends to remain in place for this year and next. Weak growth in Europe, Japan and China is fuelling deflationary concerns in these countries. This will force their respective central banks to keep expanding monetary policy stimulus. In contrast, the US Fed continues to communicate its intent to start lifting policy rates in 2015. We expect the diverging trend in growth and monetary policy stances amongst the world’s major economies to continue to push the US dollar stronger relative to the other major

currencies.

Weak growth in the world’s largest economies, coupled with a strengthening US dollar is weighing on commodity prices. Although this downtrend has been in place for a number of months, the oil price has suffered a marked decline in the last few weeks. The downward pressure was exacerbated by positive supply shocks - US shale production has been playing a larger role in global oil markets and oil supply in a few OPEC countries has been stronger than expected.

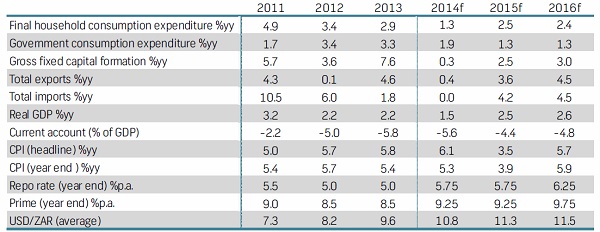

SA growth outlook

The SA economy came under significant pressure during 2014 as severe labour unrest, electricity supply shortages and weak growth in SA’s export markets weighed on output. We estimate that the SA economy grew by only 1.5% last year, its weakest performance since 2009.

Over the 2015 - 2016 forecast horizon domestic economic growth is expected to recover relative to 2014, thanks largely to a windfall from lower oil prices. This is expected to push down inflation, which will boost real disposable income of households and should allow the SARB to avoid hiking rates during 2015. Moreover, it should help to boost corporate balance sheets through margin expansion and higher sales volumes. Notwithstanding the oil windfall, GDP growth is set to remain lackluster by historical standards. This underperformance is likely to reflect

on-going electricity supply constraints, a lack of policy stimulus options as well as further labour unrest. In 2015 SA GDP is forecast to grow at a rate of 2.5%, in 2016 an acceleration to 2.6% is expected. The risks to this forecast are two sided. Upside risks may emerge if energy prices fall further or if government accelerates economic reforms. Meanwhile, risks to the downside are linked to the fragility of the global economy and the possibility that domestic

electricity and labour issues could be more severe than currently envisioned.

Figure 1: GDP growth for SA and selected regions

Source: IMF, FNB (data for 2014 is an estimate)

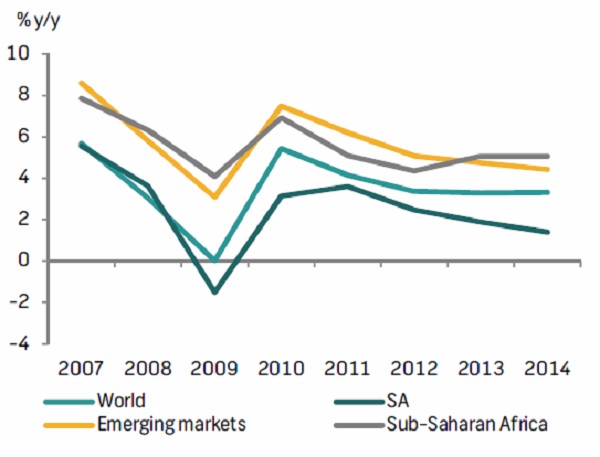

Household spending bottomed in 2014

During the first three quarters of 2014 household spending growth averaged just 1.2% year-on-year (y/y). This marks a substantial slowdown relative to the 2.9% and 3.4% growth rates recorded during 2013 and 2012 respectively. Households faced various headwinds last year as inflation remained elevated, interest rates were hiked, employment gains were muted, a significant amount of wages were lost due to strikes and credit extension slowed meaningfully.

We think that a recovery in household spending is likely over the course of 2015. The most obvious reason for this is the sharp decline in the oil price which will place downward

pressure on inflation and improve consumer affordability. We also anticipate that the SARB will keep interest rates on hold and that there will be a modest recovery in household credit growth during 2015. Nevertheless, the combination of further household deleveraging, the likelihood of higher taxes over the coming two years as well as government’s commitment to contain its wage bill (which is the largest in the formal sector) implies that household spending growth is set to remain below its long term average at 2.5%. In 2016, a forecast rebound in the oil price and domestic inflation is likely to result in slightly slower household spending growth at 2.4%.

Figure 2: Household spending, real wages and non-mortgage credit growth

Source: FNB, SARB, StatsSA

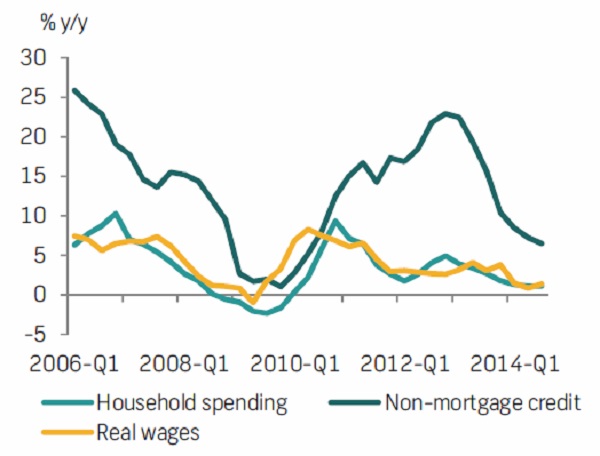

Government restraint a major priority

Government’s financial position has been deteriorating since the onset of the global financial crisis, largely as a result of persistent revenue shortfalls (relative to expectations).

However, the situation has become more serious over the past year following Standard and Poor’s (S&P) sovereign credit rating downgrade of SA to only one notch above subinvestment grade status. Finance Minister Nene’s response to the pressure from ratings agencies came in the form of a resolute commitment during the 2014 Medium Term Budget Policy Statement (MTBPS) to reduce the fiscal deficit over the coming years. A package which combines lower spending growth and increased tax revenue was proposed in the MTBPS.

Whilst we are encouraged by government’s fiscal prudence, a package of this nature does imply that the state will provide a smaller contribution to GDP growth over the medium term relative to the recent past. Adjustments to tax policy may also weigh on activity in the private sector.

It is unclear at this stage where government hopes to generate the additional tax revenue. Perhaps the most attractive option is to increase the fuel levy. This can be done against the backdrop of falling petrol prices and is therefore likely to be the most palatable option for consumers. Also, seeing as the inflation outlook has changed dramatically since the October MTBPS, government may have the ability to increase nominal spending by less than it previously forecast without adversely impacting on the amount of goods and services procured. Under those conditions government may be able to avoid hiking taxes as aggressively as previously envisioned, thereby reducing the impact of fiscal consolidation on the economy. There are various other tax and administrative reform combinations that government could use to generate the additional R27 billion in funds required over the next two fiscal years, including wealth and income taxes (which are popular due to their equity benefits). The details of any revenue or expenditure adjustments will be made available in February’s National Budget Review.

Given the projections in the 2014 MTBPS, real non-interest government spending growth is set to slow to an average of 1.3% per year during the 2015 and 2016 fiscal years. This is down from an estimated average of 2% in the prior two fiscal years. Therefore, even in the absence of tax hikes, government’s net contribution to GDP over the medium term will be lower than it has been in recent years. This fiscal consolidation is expected to result in a narrowing budget deficit over the forecast horizon from 4.1% of GDP in the 2014 fiscal year to 2.6% of GDP in the 2016 fiscal year.

Figure 3: SA Government foreign issuer credit rating (notches above subinvestment

grade)

Source: Thomson Reuters

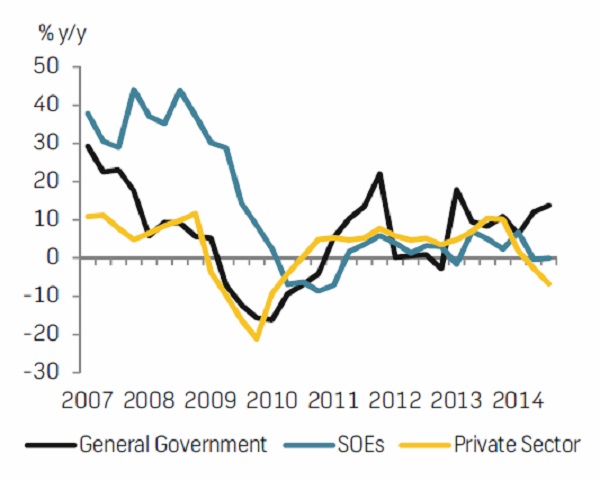

Fixed investment growth under pressure

Private sector fixed investment growth averaged –2.5% y/y during the first three quarters of 2014 as weak demand, low business confidence and labour unrest saw firms cut capital spending. This weakness was most pronounced in the manufacturing, finance and logistics sectors. Over the same period general government fixed investment growth was buoyant at 10.7% y/y, while public corporations grew capital spending by 2.1% y/y. Given the importance of the private sector in total fixed investment (accounting for about two thirds), there was virtually no growth in aggregate during the first three quarters of last year. We expect some recovery in 4Q, such that 2014 economy wide fixed investment growth moves to 0.3%. With Eskom introducing load shedding late in 2014 and the risk of labour unrest high, we anticipate that faster economic growth will only boost private sector fixed investment modestly in 2015.

Based on National Treasury’s latest estimates investment spend by general government and public enterprises is set to slow slightly in the 2015 fiscal year. This is indicative of the tight expenditure caps imposed by National Treasury. The combination of slower public sector investment and slightly faster private sector investment growth suggests that total capital outlays are set to rise in a muted fashion over the coming year. We expect growth of 2.5% in 2015, advancing to 3.0% in 2016.

Figure 4: Fixed investment growth by type of organisation

Source: StatsSA

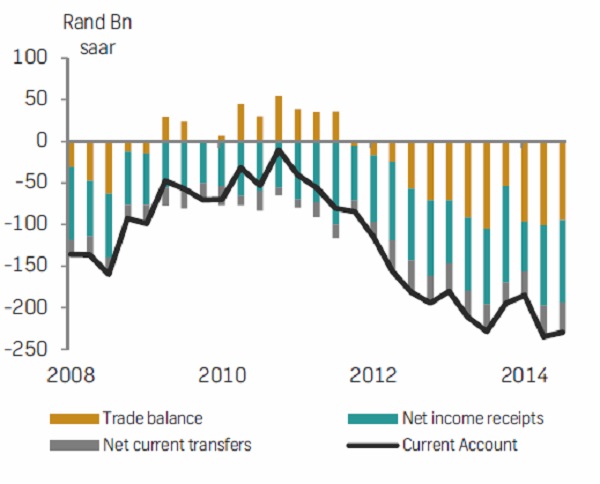

Trade balance set to improve

Despite experiencing a substantial and consistent currency depreciation since 2011, SA has run persistently large current account (CA) deficits over the past three years. The three main

causes of these CA deficits have been: consumption led GDP growth, a deteriorating terms of trade (import prices rising faster than export prices) and supply side weaknesses which

have inhibited domestic production and competitiveness. Whilst the recent labour and electricity supply issues highlight that the supply side weakness is likely to persist in 2015, we are encouraged to note that domestic consumption growth has moderated and SA’s terms of trade have begun to improve on the back of a lower oil price. These two factors are likely to see the trade balance improve in 2015, which is ultimately expected to result in a narrowing of SA’s large CA deficit. From a forecast -5.5% of GDP in 2013, we see the CA deficit moving to -4.4% of GDP in 2015. However, it is expected to widen slightly in 2016 to –4.8% of GDP. This is

premised on our view that export constraints will persist, and that a gradual oil price recovery will take place.

Figure 5: SA Current account breakdown

Source: StatsSA

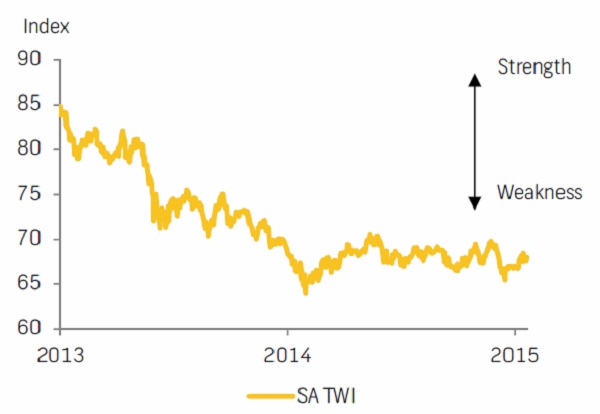

Rand: Weak vs Dollar, firmer on a trade weighted basis

The significant divergence in monetary policy across the world’s major economies is creating large currency moves. With the US Federal Reserve reducing monetary stimulus and gearing up for interest rate hikes, the Dollar has become more attractive for investors and has been on a strengthening trend. This is being supported by strong economic growth and a narrowing trade deficit. Meanwhile, Japan and the Eurozone have adopted an increasingly easy monetary policy stance. This has seen the Yen and Euro depreciate significantly in recent months.

With SA’s economic fundamentals likely to improve in 2015 - as the CA deficit narrows, growth improves and inflation falls - the Rand looks set to appreciate on a trade weighted basis.

The Rand’s appreciation is likely to materialise against those regions that are expected to adopt highly accommodative monetary policy, read: Japan and the Eurozone. Meanwhile, a modest depreciation against the US Dollar to an average of R11.30 is forecast for 2015, relative to the 2014 average of R10.84. This depreciation is premised on further acceleration in US GDP growth and a gradual rise in US interest rates from 2H 2015. The risks to our currency outlook are evenly balanced.

Figure 6: SA trade weighted exchange rate (index 2010 = 100)

Source: I-Net

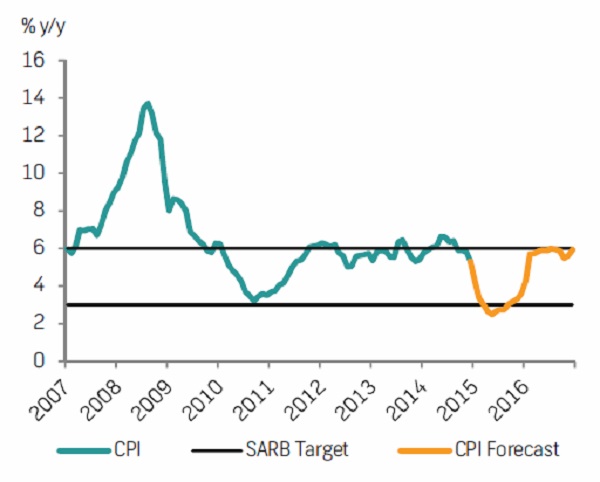

Temporary, but significant inflation reprieve

Inflation slowed to a nineteen month low of 5.3% year-onyear (y/y) in December 2014, from a recent peak of 6.6% y/y in June 2014. The decelerating inflation rate has been driven by lower food and petrol price inflation. This in turn, is due to a relatively stabile Rand exchange rate, low agricultural commodity prices and the recent fall in the oil price. The trends established in late 2014 are expected to continue and accelerate in 2015.

In particular, petrol price inflation is expected to turn deeply negative (averaging –21% y/y in 2015) as further petrol price cuts take place. This is based on our view that the oil price will remain under pressure during 1H 2015 and only recover modestly in 2H 2015.

Food inflation is likely to continue to moderate as the low maize price filters through into retail goods. However, food prices will be kept from falling aggressively due to elevated

meat costs as farmers restock herds. On average food inflation is forecast to move down to 4.2% in 2015, from 7.9% in 2014. Inflation for other retail goods is likely to slow in line with a firmer (trade weighted) Rand exchange rate and falling transport costs. Rental inflation is also likely to slow slightly on improving mortgage credit extension, low interest rates and slowing headline inflation. Meanwhile, elevated municipal and electricity charges will place some upward pressure on prices.

The net effect is a headline inflation rate that falls from 6.1% in 2014 to 3.2% in 2015, the weakest in more than a decade. Core inflation is likely to remain more sticky, falling from 5.6% in 2014 to 4.8% in 2015.

In 2016 headline inflation is expected to rebound to an average of 5.7% as a result of a partial recovery in oil prices and further significant administered price increases. However, core inflation is forecast to continue to decline to 4.5%, due to the lagged effect of low transport costs and a slightly firmer Rand in 2015.

We view the risks to the inflation outlook to be evenly balanced. Upside risks may emanate from a: faster recovery in the oil price, larger pass through from previous Rand weakness or an increase in consumption taxes by government. Meanwhile, downside risks could come from a

further fall in commodity prices, more significant Rand strength or a deterioration in GDP growth.

Hiking cycle on hold

The monetary policy committee (MPC) of the SARB has increased the repo rate by a cumulative 75 basis points (to a level of 5.75%) since the beginning of the hiking cycle in January 2014. During most of 2014, the SARB emphasized the need to gradually normalise interest rates in order to combat the inflation risks posed by a weak and vulnerable Rand. However, following the 55% fall in the oil price since 3Q 2014 risks to both the inflation and exchange rate outlook have diminished. As a result we now expect the SARB to remain on hold for the duration of 2015.

Unfortunately, the windfall from lower oil prices is only likely to be transitory (from an inflation perspective) and the Rand is expected to face renewed pressure in 2016 as US interest

rates begin to rise. Therefore, SA’s interest rate tightening cycle can be expected to continue from early 2016 onwards. The pace and magnitude of tightening will depend largely on the rhetoric coming from the US Federal Reserve (Fed) and its impact on the currency. We currently anticipate 50 basis points of interest rate hikes in 2016 for SA. This is premised on a gradual, shallow hiking cycle in the US and on-going monetary accommodation from the Eurozone and Japan.

There is likely to be some speculation over interest rate cuts over the coming months given the sharp inflation slowdown that is set to take place. We do not think that a rate cut is viable due to our forecast for an inflation rebound in 2016. Moreover, SA’s CA deficit remains relatively large and further stimulus to consumer spending increases the probability of the deficit widening. This would raise the risk of medium term macroeconomic instability in an environment that is likely to be characterized by weak commodity prices, rising US interest rates and US Dollar strength. Nevertheless, a small rate cut in 2015 is possible if the Rand strengthens meaningfully against the US Dollar and SA’s supply side constraints begin to ease.

Figure 7: SA headline inflation forecast

Source: Econostat

FNB Economic Forecast Summary: