South Africa running out of steam

The South African recovery, according to the SA Reserve Bank (SARB), started in August 2009. South Africa’s economy usually lags the global cycle by a few months. The local economy initially bounced back quickly, led by consumer spending, a strengthening rand and a recovery in commodity prices. After a 1.5% contraction in 2009, annual GDP growth rose to 3.1% in 2010 and 3.6% in 2011. Growth then slowed to 2.5% in 2012 and 1.9% in 2013. The economic recovery was also helped by very accommodative fiscal policy as the government ran large budget deficits to increase spending and hire around 250 000 more employees. However, the government is now trying to slow its spending growth to below 2% per year in real terms and close the budget deficit. Failing to do so could result in another downgrade of our credit rating.

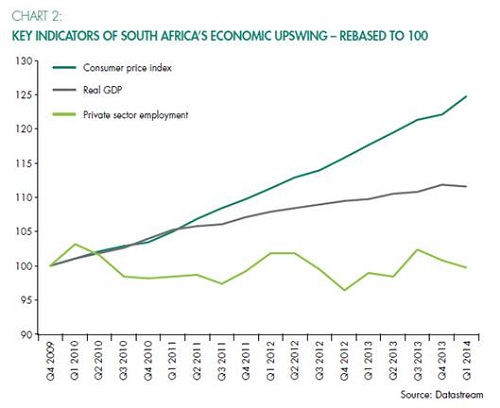

The rand strengthened between late 2009 and 2011, but has since lost 60% against the US dollar. The CPI has risen 27% since August 2009. The inflation rate (year-on-year change in the CPI) initially fell sharply from 6.3% to 3.1% then rose again and stabilised around 5% - 6% since early 2011. Even the rand’s relentless depreciation since August 2011 (from R6.80/US$ to R10.70/US$ last week), has only resulted in a modest rise in inflation. The limited reaction of inflation to major currency weakness marks an important shift in our economy, and if it continues, implies that future interest rate cycles should be more muted than in the past.

Consumers now face a squeeze

Consumers enjoyed real disposable income growth rates in excess of 4% per year between 2010 and 2012. Public servants in particular received generous pay increases. But wage growth is slowing and it is only those with jobs that benefited. While real GDP is 11% higher than at the start of the current upswing phase, private sector employment is slightly lower. It has thus been a classic “jobless recovery”. Without more jobs, consumer spending cannot grow sustainably and consumers are facing a relentless squeeze on their finances. Consumer sentiment was lower in the first quarter than at any time during the 2008-2009 recession, according to the FNB/BER survey (in contrast to US consumer confidence at six-year highs).

Apart from a boom in unsecured lending – typically to low income households with little previous access to formal bank credit – credit growth in South Africa has been slow. This is an area where we differ from other emerging markets. The “quantitative quintet” of Brazil, China, India, Turkey and Indonesia experienced credit growth of 15% - 20% per year since 2008. However, like these countries, South Africa benefited from massive capital inflows as global investors stretched for yields. South Africa received about R330 billion in cumulative net inflows since August 2009 (according to JSE data), of which R250 billion flowed into the bond market. These capital inflows have so far financed our current account deficit, effectively allowing South Africa to continue living beyond its means.

Production growth has been disappointing

Meanwhile, despite an initial recovery in commodity prices and a weaker rand, mining output has moved sideways, but with fairly large swings from quarter to quarter. More recently, it has been hobbled by a series of protracted strikes. The Association of Mineworkers and Construction Union strike in the platinum sector ended last week, but only after costing producers an estimated R24 billion in revenues and workers R10 billion in wages. Improved platinum production should help to accelerate local economic growth somewhat in the second half of 2014 and assist in narrowing the still-wide foreign trade deficit.

Manufacturing production has risen about 12% since the start of the recovery, held back initially by weak foreign demand and more recently by weak local demand. There are promising signs of exports picking up but not enough to jump-start the economy yet.

Local equities performed well over the period, with the JSE All Share Index (including dividends) rising more than 70% in real rand terms since August 2009. The earnings of JSE listed companies have rebounded 70%. In US dollar terms, the JSE also rebounded quickly from late 2009, but moved broadly sideways since early 2011. The All Share Index is only 11% up over three years in US dollar terms, but most of that performance has happened since February this year.

The JSE All Share’s high PE ratio reflects a mixture of highly valued largecap defensive rand hedges, and shares exposed to the local economy with lower ratings (but which are not historically cheap). However, while high PE ratios imply lower future returns, they cannot predict corrections nor do they imply a major bear market. Historically, South Africa experienced major equity slumps only when a macro shock hit the US (such as 2008) or due to a crisis in emerging markets (such as 1998).

Growth recession

The underlying growth rate of the local economy has slowed to around 2%. If growth remains persistently below our 3% - 3.5% long-term potential with little to no job creation, it means the economy is trapped in a growth recession (even if it should escape a technical recession). Looking ahead, the SARB’s latest leading indicator was unchanged in April, and has been trending sideways since mid-2010. The leading indicator points to changes in economic activity six to nine months ahead, suggesting no significant improvement ahead (unless exports start accelerating).