SARB takes action to see inflation at the midpoint of the target range

South Africa needs to lower its inflation trajectory to temper interest rate hiking cycle

The Monetary Policy Committee (MPC) of the South African Reserve Bank (SARB) adopted a tighter monetary policy stance in November, raising interest rates by 25 basis points (bps) and bringing the repo and prime lending rates to 6.75% and 10.25%, respectively.

In hiking interest rates, SARB Governor Lesetja Kganyago noted the MPC aimed for a more moderate interest rate hiking cycle: waiting for inflation developments to unfold would have raised the risk of a more aggressive interest rate stance being required in coming months.

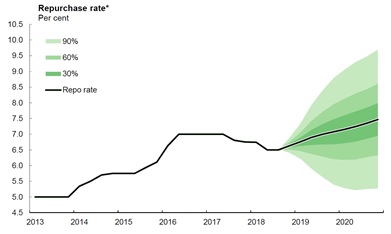

The increase in interest rates came in spite of an improvement to the inflation outlook, with the SARB revising down its forecast for 2018 headline inflation to 4.7% from 4.8% previously. Inflation is expected to average 5.5% (down from 5.7% previously) and 5.4% in 2019 and 2020, respectively. The expected peak in headline inflation moved out to the third quarter of next year to 5.6%, which was previously forecast at 5.9% in the second quarter of 2019. This inflation outlook, however, is predicated on November’s interest rate increase, as well as the following three increases of 25 bps each before the end of 2020, bringing the repo rate to 7.5%.

SARB Quarterly Projection Model repo rate forecast, November 2018

The MPC would like to see inflation stabilise at the midpoint of the target range of 4.5%, which would prevent shocks to the economy from pushing inflation to breach the upper end of the 3%-6% target range – a risk the SARB has warned of at numerous previous MPC meetings. Through seeing inflation settle at the midpoint of the target range and ensuring price stability, the SARB can contribute to fostering an important foundation of sustainable economic growth.

This month’s MPC decision was a close decision, with three members preferring a rate hike of 25 bps and three members preferring rates to remain on hold. This reflects the SARB’s ongoing dilemma, where weak economic performance and constrained household finances provide little threat of demand pressures pushing up prices. This is visible in core inflation, which has remained below the midpoint of the target range for the most part of 2018.

On the other hand, headline inflation is expected to tick up in coming months, driven in part by rising utilities tariffs, as well as base effects. Upside risks to the outlook include the ongoing tightening in global financial conditions, wage growth, oil prices and rising electricity and water tariffs. Furthermore, rand vulnerability remains a key risk to the inflation outlook, with the risk of emerging market risk spill over, developed markets monetary policy tightening, as well as domestic economic drivers playing a role in recent exchange rate volatility.

According to the SARB, the rand remains undervalued, even after a recent period of exchange rate strengthening, which has limited the risk of imported inflation as an immediate threat to the inflation outlook. Most recently, Statistics South Africa (StatsSA) reported that its price index for imports declined by 0.1% year-on-year (y-o-y) in August. Imports excluding crude petroleum cost 7.4% y-o-y less.

Looking forward, the SARB’s interest rate hike affirms the emphasis not only on anchoring inflation inside the target band, but more closely to the middle of the range to allow greater flexibility around the anchor of 4.5%. The Quarterly Projection Model, a broad policy guide used by the SARB, suggests another three hikes of 25 bps are on the cards before the end of 2020, which entails a slight moderation in the expected hiking cycle, compared to the projections detailed at the September MPC meeting.

The SARB’s target of anchoring inflation near 4.5% is ambitious. Since adopting inflation targeting in 1999, inflation has averaged near the top end of the 3% - 6% target range. On a calendar year basis, inflation has overaged around 4.5% only two times over the past decade, in 2010 and 2015. Even with the support of higher interest rates, the central bank sees inflation averaging 5.3% in the last quarter of 2020 – still some way from 4.5%.

Inflation in South Africa is both a structural and monetary phenomenon, thus inflation can be tamed only to some extent by higher interest rates. On the structural side, reforms are necessary to lower inflation. This includes changes in the way that inflation-drivers like electricity, fuel and other administered prices are determined – and this requires changes to how these markets and related entities operate.

The International Monetary Fund (IMF) commented last week that monetary policy “should focus on anchoring inflation expectations at the mid-point of the target band”. A September survey by the Bureau for Economic Research (BER) found that analysts, business people and trade union officials expect inflation to average 5.6% in 2020 – far from the 4.5% level currently in focus.

South Africa needs to lower its inflation expectations in order to temper the upward curve in interest rates. However, considering that inflation in South Africa is currently largely supply-side driven, the moderating of inflation expectations requires a broader conversation about the nature of price pressures in the country. Expectations will continue to be elevated relative to the 4.5% goal for as long as administered prices in particular are anticipated to rise rapidly.