SA medium-term budget 2017

Sanisha Packirisamy, Economist at Momentum.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Have we reached the fiscal cliff?

Budget negative for bonds and the currency, but equities rallied post the announcement

In an immediate reaction to the budget announcement, the SA rand tumbled by 1.6%, while SA bond yields (R186) sold off by 18 basis points. A frustratingly unclear outlook on the direction of economic policy in SA weighs negatively on domestic growth prospects and as such revenue collection in the currently low growth environment will remain a significant challenge to fiscal consolidation over the medium-term expenditure framework (MTEF). Treasury warned additional tax proposals would have to be carefully considered in light of pressures in the economy. Consumer confidence remains in the doldrums. Tepid jobs growth, moderate wage settlements and declining growth in wealth metrics have stifled the SA consumer, while persistently weak growth and commodity price volatility have dampened corporate tax collections.

The FTSE/JSE ALSI reacted slightly positively in reaction to the budget announcement, closing nearly 0.4% higher on 25 October 2017. The equity market was supported by gains in industrial and resource shares, while financial stocks closed lower. The FTSE/JSE Industrials Index ended the day 0.9% up and the FTSE/JSE Resources Index added 0.6%, thanks to currency weakness. The FTSE/JSE Financials Index dropped nearly a percent, as the lack of a firm commitment to fiscal consolidation and little sign of a stabilisation in government’s debt ratios over the MTEF left the market concerned about additional negative ratings action.

Treasury employing more realistic nominal growth forecasts this time around

In its October 2017 Monetary Policy Review, the SA Reserve Bank (SARB) calculated a strong relationship between global and domestic growth historically. Between 1996 and 2016, a 1% increase in global growth was matched by a 0.94% increase in the level of SA output. However, a notable divergence opened between SA and global growth in 2011 and the gap started to widen materially since 2013. The results of the study highlight subdued confidence and lower real commodity prices as the main drivers behind SA’s growth underperformance. The study shows that if these variables had followed their longer-run averages, local growth could have registered at 2.1% in 2016 (and 2.4% in 2015), rather than the paltry 0.3% (1.3% in 2015) which instead materialised.

Treasury expects growth in real gross domestic product (GDP) to increase modestly in the medium term from 2016 levels, but these rates are likely to be insufficient to make meaningful inroads into SA’s elevated rates of unemployment, stark poverty levels and dangerously wide income inequality measures. Growth in real GDP, on a per capita basis, is expected to continue trending in negative territory in the near term. The rating agencies have highlighted the slow pace of economic growth on a per capita basis as a weakness to SA’s sovereign rating. After identifying supply bottlenecks and much-needed reforms in SA’s highly concentrated economy, Standard & Poor’s (S&P) assessed the delivery of reform as piecemeal to date. The potential for political interference could delay the implementation of necessary reforms, dampening already modest growth prospects. Ongoing political tensions are inhibiting firms’ capital investment and hiring decisions, which would have otherwise supported higher rates of economic activity.

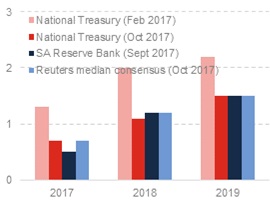

Chart 1: Treasury lowers real GDP growth forecasts (%)

Source: National Treasury, Momentum Investments

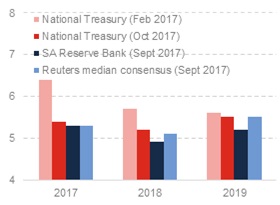

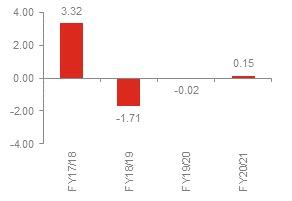

Chart 2: Treasury cuts inflation forecasts (%)

Source: National Treasury, Momentum Investments

In Momentum Investments’ view, Treasury’s latest assumptions on real growth and inflation (and hence nominal GDP) look more realistic this time around. In the absence of a negative growth shock or a mismanagement of funds, Momentum Investments does not expect further slippage relative to what Treasury has indicated in its October 2017 assessment. Treasury anticipates real growth to increase at an average rate of 1.6% in the MTEF. Relative to the February 2017 national budget, Treasury downwardly revised its real GDP growth estimate from 1.3% in 2017 to 0.7% and from 2% in 2018 to 1.1% (see chart 1). Treasury’s latest growth expectations are broadly in line with the SARB’s September 2017 growth projections and the median market estimate for October 2017.

Treasury’s headline inflation estimates have also been revised lower to average 5.5% in the MTEF. It noted a potential downgrade to the local currency rating and higher administered prices as key upside risks to this forecast. The 2017 headline inflation projection was lowered from 6.4% to 5.4%, while the 2018 forecast declined by 0.5% from 5.7% (see chart 2).

A further deterioration in the projected economic outlook poses a threat to medium-term revenue collection. In a local downgrade scenario (due to the weak growth trajectory and widening fiscal deficits), Treasury indicated real growth in 2018 could be 0.5% lower than its baseline forecast, while 0.6% could be shaved off its 2019 growth estimate. Should more pronounced effects filter through, Treasury estimates a contraction in real GDP growth of 1.2% in 2018, picking up to only 0.8% in 2019. A third scenario run by Treasury studies the impact of a potential upside surprise in domestic growth driven by higher global activity and an average 5% increase in commodity prices in the medium term. In this scenario, local growth could reach 1.4% in 2018, increasing to 2.4% by 2020.

Compliance concerns are an additional risk to revenue collection. Treasury notes policy and administrative factors may be contributing to the current revenue shortfall and highlights weakening tax morality as a challenge in the current low growth environment.

Poor revenue performance

In Momentum Investment’s budget preview, the firm indicated the current underperformance in gross tax revenues (tracking at 6.1% in year-on-year (y/y) terms relative to Treasury’s February 2017 predictions for a 10.6% rise) would result in a shortfall of R51 billion if extrapolated for the remainder of the year. In its October 2017 update, Treasury projected a tax revenue shortfall of R50.8 billion relative to the 2017 budget estimate, which is the largest downward revision since the 2009 recession. A R69.3 billion shortfall is estimated for FY2018/19 and a larger R89.4 billion undershoot is forecasted for FY2019/20.

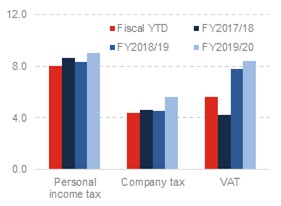

The largest revenue disappointment relative to the February 2017 budget has been in personal income tax (PIT). The 13.6% y/y projection for PIT in FY2017/18 in February 2017 (lowered to 8.6% in October 2017) included fiscal drag measures and the rate increase announced for the highest marginal tax bracket from 41% to 45%. However, according to Treasury, a moderation in average wage settlements, low bonus payments, job losses and a slower expansion in public-sector employment has contained the year-to-date (YTD) increase in PIT at 8.0% y/y (see chart 3).

Corporate income tax (CIT) increased 4.4% y/y YTD, relative to government’s revised full-year 4.6% projection. The run rate may however improve into December 2017, when seasonal lumpy receipts are generally noted. Treasury indicates company tax under-collections are the result of persistently weak growth and commodity price volatility. The YTD run rate in value-added taxes (VAT) is slightly ahead of the revised October 2017 target, but markedly below February’s target. VAT receipts are 5.6% higher relative to the previous fiscal year on a YTD basis, ahead of government’s new target of 4.2%. Treasury attributes weak investment and household consumption to a sharp contraction in imports, which affected VAT as well as customs duties.

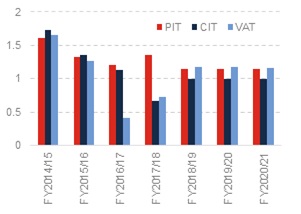

Treasury acknowledges robust tax buoyancy ratios are unlikely to persist. Between FY2010/11 and FY2015/16, the tax buoyancy ratio averaged 1.28, implying that for every 10% growth in nominal GDP during that period, 12.8% growth in revenue collection was achieved on average. However, a persistent negative output gap is likely to drive ratio lower in the medium term.

Chart 3: Key government revenue projections (% y/y)

Source: Global Insight, National Treasury, Momentum Investments

Chart 4: Tax buoyancy ratios

Source: National Treasury, Momentum Investments

Treasury cut its PIT buoyancy assumption for the MTEF from 1.28 a year ago to 1.15 (see chart 4). Similarly, the highly uncertain CIT buoyancy ratio is expected to fall to its long-run average of 1. A spike in the VAT buoyancy ratio in FY2017/18, due to a sharp contraction in imports, is not expected to recur.

Tax proposals in the pipeline

Government admits additional tax proposals have to be carefully considered in light of overall pressures in the economy. More information on tax proposals is expected in the February 2018 budget. In its October 2017 update, Treasury alluded to a Health Promotion Levy (sugar tax) which is currently under consideration at Parliament, with a proposed implement date of 1 April 2018. No further details on the impending carbon tax were given, except to confirm a revised Carbon Tax Bill would be published in due course.

In the February 2017 budget, Treasury hinted at using medical tax credits to fund the national health insurance (NHI). It claims R18.5 billion was distributed to 3 million members in FY2014/15. Treasury noted it is “considering changes to the design, targeting and value of the medical tax credit as part of the policy development process for the 2018 budget”.

Less commitment shown to fiscal consolidation

On the consolidated budget figures, total revenue collections are now expected to be R189.9 billion lower between FY2017/18 and FY2019/20 in the next three fiscal years (back-end loaded) than projected a year ago in the October 2016 Medium Term Budget Policy Statement (MTBPS). Expenditure projections have only decreased by R9.9 billion in the same period. As a result, Treasury expects a markedly slower pace of fiscal consolidation than proposed in February 2017.

Chart 5: Expenditure outstrips revenue growth (%)

Source: National Treasury, Momentum Investments

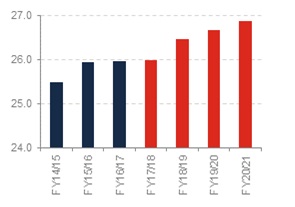

Chart 6: SA’s tax to GDP ratio edging higher (%)

Source: National Treasury, Momentum Investments

With expenditure growth outstripping revenue growth on average between FY2017/18 and FY2020/21, this budget is seen to be expansionary in nature (see chart 5), but not stimulatory as the largest growing expenditure item is still the interest bill. Average nominal growth in revenues is pitched at 7.1% for the same period, while average nominal growth in expenditure is likely to outpace at 7.6%. In Momentum Investments’ opinion, expansionary fiscal and monetary policy are likely to have a limited positive growth impact in the current environment. SA’s growth problems are instead centred on a lack of a clear direction in economic policy, which has dampened sentiment and curbed investment.

Despite explicitly deviating from the fiscal consolidation path set out in February 2017, as a result of revenues undershooting, SA’s tax burden is expected to drift higher in the medium term. While this could be construed as slightly contractionary for growth, reduced revenue forecasts have left the tax burden, in the outer year of the MTEF, lower than predicted in the February 2017 budget. SA’s tax-to-GDP ratio is set to climb from 26% currently to 26.9% by FY2020/21 (see chart 6). SA’s current tax burden ranks above that of the Organisation for Economic Co-operation and Development (OECD) composite and is higher than a number of emerging markets, including Brazil, Turkey and India.

While it is crucial to maintain spend on essential services and preserve social security benefits, including social grants and unemployment insurance fund benefits that protect the more vulnerable income-earning groups, in the longer term a leaner government and deficit reduction are necessary to positively impact the private sector and overall growth.

Slight miss on the expenditure ceiling

Government remains broadly committed to the expenditure ceiling in the medium term. However, it notes the recapitalisation of SA Airways (SAA) and the SA Post Office (SAPO) are putting the ceiling at risk of a R3.9 billion breach. Despite the emphasis the rating agencies have placed on the deterioration in financial standing and governance measures at many of the key state-owned enterprises (SOEs), government was unable to commit to a funding plan in the October 2017 MTBPS. It notes it is considering the disposable of assets to offset these appropriations in the current year, but no further details have been divulged. Selling off assets to fund running costs is seen as a negative by Momentum Investments, particularly if it gives rise to further bailouts down the line.

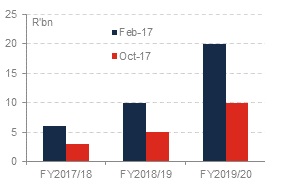

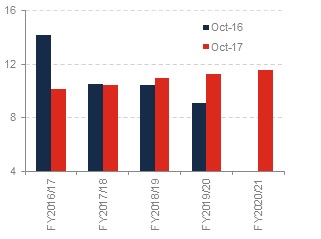

Government has drawn down on the contingency reserve (an amount set aside to accommodate unforeseen spending pressures) to partly offset revenue shortfalls and reduce borrowing. With government slashing the contingency reserve from R10 billion in FY2018/19 to R5 billion and from R20 billion to R10 billion in FY2019/20 (see chart 7), reserve funds are much lower than they have been in previous budgeting cycles. This reduces government’s wiggle room in the event it needs to react to medium-term expenditure risks, such as an overrun on the public-services wage bill or additional funding needs for higher education.

Chart 7: Contingency reserve drawdown

Source: National Treasury, Momentum Investments

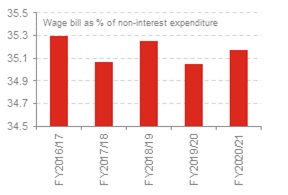

Chart 8: Sticky government wage bill

Source: National Treasury, Momentum Investments

The civil servant wage bill is still one of the largest drags on expenditure. For every R1 government spends on non-interest expenditure, around 35 cents goes towards funding the government wage bill (see chart 8). In 2012, government announced it would attempt to curb unsustainable growth in the public sector wage bill by blocking appointments to non-critical posts and reducing headcount in administrative and managerial posts. In addition, performance bonuses and staff promotions were to be monitored closely. Treasury noted some national departments battling to operate within these limits and pointed out that several departments have left bills unpaid in order to maintain service delivery levels. This points to a possibility that some national and provincial departments will exceed compensation ceilings. The MTEF can accommodate a nominal wage billincrease of 7.3% per year (1.8% in real terms), however some departments are already at risk of exceeding this limit, even if the number of staff does not increase.

Government clamped down on non-core spending and has improved value from procurement between FY2013/14 and FY2016/17. During that period, the cost for consultants decreased by 4.1% per year, while conference venues and facilities decreased by a larger 7% per year. Travel and subsistence costs (the largest portion in non-core expenses) decreased by 1.8% every year in the same period. Treasury notes the bulk of cost cutting has already taken place and little room remains to cut expenses further.

Planned infrastructure investment amounts to R948 billion in the medium term

Government highlighted infrastructure spending as a priority for the 2018 budget. In particular, government will be focusing on maintaining real growth in infrastructure spend, expanding agri-parks programmes, revitalising township industrial parks and technology innovation hubs, rural roads, broadband and water infrastructure as well as maintenance at the local government level. Little other detail on government’s infrastructure plan was shared in the October 2017 MTBPS.

Worrying rise in interest bill crowding out more desirable forms of expenditure

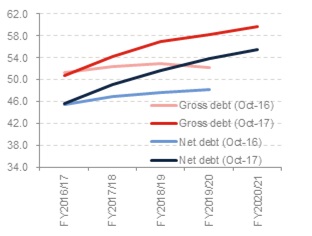

With the budget deficit ratio stabilising at around 4.6% of GDP in the medium term, the gross debt ratio is set to climb from 54.2% of GDP in FY2017/18 to 59.7% in FY2020/21 (see chart 9). Only a year ago, government expected the gross debt ratio to decrease from 52.5% of GDP in FY2017/18 to 52.3% of GDP in FY2019/20. Treasury estimates stabilising gross debt below 60% of GDP in the coming decade “will require spending cuts or tax hikes amounting to 0.8% of GDP (R40 billion in FY2018/19 terms)”.

Chart 9: Major deterioration in debt profile (% of GDP)

Source: National Treasury, Momentum Investments

Chart 10: Hefty interest bill (% y/y)

Source: National Treasury, Momentum Investments

Due to the rapid increase in government debt, the interest bill is expected to remain the fastest-growing expenditure item at an average of 11% per year in nominal terms (see chart 10) and equating to 5.5% in real terms. Debt-service costs are expected to rise to a whopping 15% relative to the main budget revenue inflow. The rapid rise in debt-servicing costs is crowding out other (social and growth-enhancing) spending priorities and has been raised as a key concern by the rating agencies in the past.

Contingent liability and longer-term spending risks

Treasury did not give an update on its contingent liabilities, of which guarantees are the largest portion. The latest available figure for government’s guarantees stood at R688.8 billion in FY2016/117, suggesting that total debt inclusive of contingent liabilities would rise to over 80% in the medium term. But with an increase shareholder activism, SOEs are facing difficulties in raising debt and this could lead to greater demands on the fiscus. The financial standing of SOEs has deteriorated in recent years. Treasury claims the return on equity measure for all SOEs declined from 7.5% in FY2011/12 to a meagre 0.2% in FY2016/17. Government notes total interest payments by SOEs are projected to increase from R49.8 billion in FY2016/17 to R69.3 billion by FY2019/20, implying that some entities could come up short, unless reforms to improve governance and boost profitability are implemented as a matter of urgency.

The largest state guarantee (R350 billion) is to public electricity utility Eskom. If Eskom’s application for a tariff increase for FY2018/19 as well as its Regulatory Clearing Account application are unsuccessful, further government assistance may be necessary. While government’s R19.1 billion guarantee to SAA is much smaller, investors have grown wary of a fruitful turnaround strategy at the country’s national carrier. A permanent chief executive officer has been appointed at SAA, backed by a new board, in an effort to improve governance as well as to get the carrier back on firmer financial footing. In Momentum Investments’ view, government should consider privatising some of its SOEs, before it is forced to so at fire-sale prices.

Government disclosed that the Road Accident Fund (RAF) has been insolvent for over 35 years. Claim amounts which have been settled in court, but have not yet been paid, amounted to R8.5 billion at the end of FY2016/17 and are forecasted to grow in the medium term.

Even though disbursements to Higher Education and Training are the second-fastest growing item in the budget, frustration over university fees continues to mount in SA. The Commission of Inquiry into Higher Education and Training has submitted its report to the President on the feasibility of providing fee-free higher education, while government is concurrently looking into the option of providing financial aid towards the full cost of study for students from poor and middle-income households. Government predicts provision for financial aid for the full cost of study to 75% of undergraduate university students would push post-school education spend up from 1.4% of GDP currently to 4.1% of GDP by FY2030/31.

Finally, Cabinet adopted the white paper on the NHI in June 2017. On an assumed growth rate of 2.5% per year, Treasury estimates that the full implementation of the NHI would increase public health expenditure to 6.8% of GDP by FY2025/26 (from 3.9% in FY2017/18).

Have we reached the fiscal cliff?

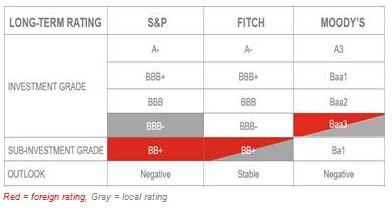

S&P and Fitch downgraded SA’s foreign currency rating to sub-investment grade in April 2017, following a damaging cabinet reshuffle which raised the risk of an adverse change in the direction of economic policy and fiscal policy management. However, the ratings which matter most for SA’s inclusion in the Citi World Government Bond Index (WGBI) are the local ratings by S&P and Moody’s, which still rank one notch above sub-investment grade (see table 1).

Table 1: SA’s sovereign ratings

Source: S&P, Moody’s, Fitch, Momentum Investments

While Momentum Investments intimated the rating agencies may choose to remain on hold at the upcoming reviews in anticipation of the highly-uncertain outcome of the African National Congress National Elective Conference in December 2017, the lack of commitment to fiscal consolidation and a climbing debt ratio over the MTEF could prompt a downgrade as early as November 2017. Treasury admitted that although aggressive fiscal consolidation to stabilise debt ratios and narrow the budget deficit could reduce financial risks, this approach could also weaken demand, curb investment and dissuade employment creation. Nonetheless, Treasury qualified its opinion by adding that taking no action could very well result in rating downgrades, pronounced capital outflows and a sell-off in the local currency.

The budget failed to outline how government would break the economy out of its current weak growth cycle. Policy uncertainty remains a key barrier to investment in SA. The budget revealed little new information regarding the progress made towards gazetting the mining charter, other than announcing it has been postponed to December 2017. Without definitive legislation, which has buy-in from all key stakeholders, SA is unlikely to be seen as an attractive destination for new (and foreign) investment in the mining sector.

Similarly, there was no further update on the controversial issue of land reform. Government is still consulting stakeholders on the Regulation of Agricultural Land Holdings Bill. More equitable land ownership could compromise agricultural investment and food security if not approached correctly. Ceilings for private agricultural land ownership and regulating ownership of agricultural land by foreigners could hamper the agricultural sector’s development. In Momentum Investments’ opinion, transformative efforts driven by increased state intervention could dissuade private fixed investment if not accompanied by new policy initiatives to place the economy on a higher and more sustainable growth path.

Potential growth remains muted and real GDP growth will likely struggle to outpace population growth in SA over the next few years.

Low levels of real GDP per capita will add to social spending pressures in Momentum Investments’ opinion. Aside from low economic growth, rising political tensions are accentuating economic and social vulnerabilities.

The pressure on the fiscus remains high. Revenue estimates are declining, while debt measures are set to increase further. While SA should by growing its state assets, the country is accumulating more state dependencies, which aggravate SA’s overall debt profile and creditworthiness risks.

Although prudent monetary policy, quality fiscal institutions and SA’s floating exchange rate regime (acting as a shock absorber) have in the past been noted as vital pillars of strength in SA, rising perceptions of political interference in key spheres of government institutions threaten SA’s macroeconomic performance. SA’s potential growth profile and overall governance could be negatively impacted by political infighting, distracting policymakers from adhering to sound fiscal management and maintaining a healthy investment climate through the implementation of growth-enhancing policy initiatives.

A downgrade in SA’s local currency rating to junk status by S&P and Moody’s would trigger SA’s exclusion from the WGBI, which could prompt significant capital outflows from the SA government bond market. Estimates of potential outflows range anywhere between R85 billion and R130 billion. Citi notes that while buying into the index inclusion might have been staggered, the exit door could be crowded. Re-entry into the index will be difficult to achieve. The Citi WGBI requires a minimum credit quality of A- by S&P and A3 by Moody’s for the country’s local currency rating (four notches above junk status).

To see info graphic of Medium Term Budget Policy: Have we reached our Fiscal cliff? Click here.