SA businesses facing increased uncertainty

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of Asset Allocation at MMI Holdings.

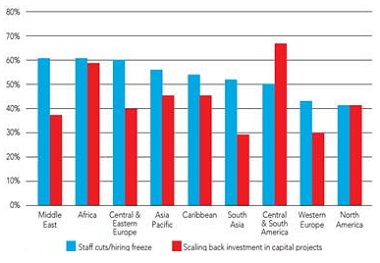

The Global Economic Conditions Survey (produced by the Association of Chartered Certified Accountants) revealed that global firms remained gloomy about their prospects in 4Q15.

Global firms remained gloomy about their prospects in 4Q15

The survey reported that 44% of respondents were less confident than they had been three months earlier; only slightly fewer than in 3Q15, when businesses were at their most pessimistic in four years.

In general, firms (globally) noted a greater reluctance to hire new workers as revenues fell further and fewer investment opportunities arose (chart 1). Businesses were largely concerned about growth fragilities in emerging market economies and the fall in commodity prices. Notwithstanding the steep fall in commodity prices, rapidly rising wages and escalating input costs have led to the bottom line being squeezed across the globe.

Chart 1: Weak hiring and investment intentions

Source: Global Economic Conditions Survey Report 4Q15

Domestic business sentiment remains in the doldrums

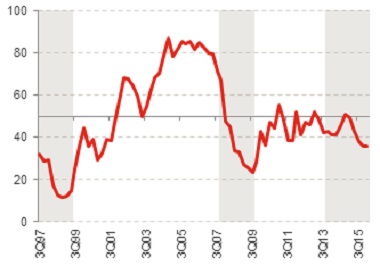

The Bureau of Economic Research’s (BER) Business Confidence Index (BCI) covers the building, manufacturing, retail, wholesale and new vehicle trade sectors and indicates the percentage of respondents that rated prevailing business conditions as satisfactory. The index ranges between 0 and 100, where 50 is taken as the neutral level. The headline index remained unchanged at 36 index points in 1Q16 from a quarter ago, tracking five points below the average reading of 41 points since the Global Financial Crisis (GFC). This reading reflects soft economic conditions and an adverse environment for SA businesses to hire extensively or expand on fixed investment projects. The South African Reserve Bank (SARB) recently confirmed that November 2013 signalled the upper turning point in the SA business cycle, implying that the domestic economy is currently in it’s 28th month of the current downward phase (see chart 2).

Chart 2: BCI trending mostly below 50 in recent downward phase in the economic cycle

Source: BER, SARB, Momentum Investments (grey bars = downward phases), data up to 1Q16

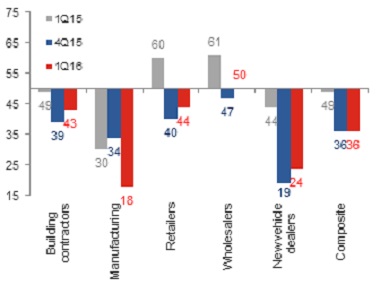

The largest drop in confidence was observed in the survey responses of manufacturers, where confidence slid 16 points lower in 1Q16, while confidence levels inched higher for the remaining industries. Nevertheless, overall confidence levels remained at or below the crucial 50 mark for all of the sectors surveyed pointing to broad-based economic headwinds (see chart 3).

Chart 3: Business confidence index by sector (>50 = expansion)

Source: BER, Momentum Investments

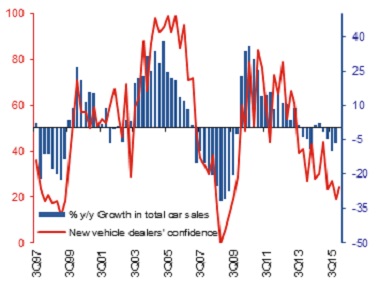

Subdued confidence across vehicle dealers indicates further weakness in new vehicle sales

Confidence levels for new vehicle dealers increased marginally from 19 index points in 4Q15 to 24 points in 1Q16 (see chart 4), but remained in negative territory for the eleventh consecutive quarter. According to the BER, the slight move higher was merely a normalisaton from an overly negative print in the final quarter of 2015, but the underlying survey indicators flag challenging conditions ahead in this sector. In contrast, the BER reported that used car sales were performing relatively well as consumers traded down in the tougher economic climate.

Chart 4: Bleak new vehicle dealer confidence reflective of a testing consumer environment

Source: Global Insight, Stats SA, Momentum Investments, data up to 1Q16

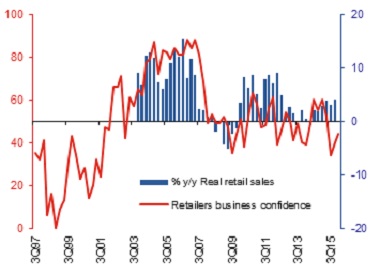

Retail sentiment remains soft

Retailer confidence edged four points higher to a reading of 44 in 1Q16 (see chart 5). According to the BER, sales volumes indicators for non-durable and semi-durable goods shifted lower while pre-emptive buying (in light of sharp currency depreciation and the expectation that this would filter into higher prices) supported sales of durable goods. As such, this is unlikely to be repeated in the near term.

Chart 5: Retailer confidence points to challenging retail conditions ahead

Source: Global Insight, Stats SA, Momentum Investments, data up to 1Q16

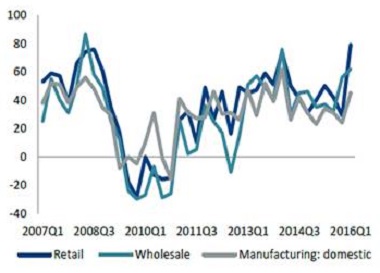

The underlying survey detail shows a sharp increase in average selling prices in the retail sector (finally following trends observed in the wholesale sector, see chart 6), but measures of profitability deteriorated further. The sharp move higher in average purchasing price and selling price inflation indicators suggest a wider increase in consumer price inflation in upcoming months.

Over the past three quarters there has been a distinct disconnect between muted retailer sentiment and relatively firm retail sales growth as captured by Stats SA, leaving us cautious on growth in household consumption expenditure. Lower-income earners are increasingly facing higher food costs and the threat of further job losses, well upper-income earners are more exposed to rising interest rates and a slowdown in growth in net wealth creation on the back of recent movements in equity and home prices.

Chart 6: Net % expecting an increase in selling prices

Source: Global Insight, Stats SA, Momentum Investments

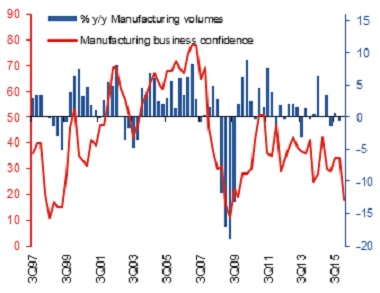

Manufacturers increasingly facing slowing demand domestically and in export markets

Manufacturing sentiment tanked by 16 points in 1Q16 to 18 (see chart 7). The manufacturing sentiment index has remained in negative territory since 3Q11, corresponding to the weak 1.4% average growth rate experienced in manufacturing volumes produced over the corresponding period. Labour unrest has been a key driver behind the volatility in growth in manufacturing goods volumes produced.

Chart 7: Manufacturers feeling the heat

Source: Global Insight, Stats SA, Momentum Investments

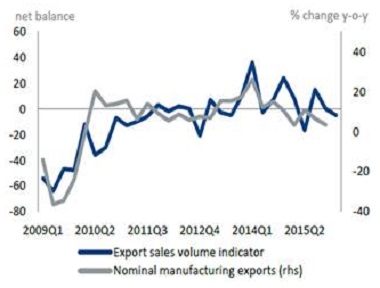

According to the BER, domestic indicators of sales and order volumes dipped further in 1Q16 with wholesalers and retailers reporting a further deceleration in the growth of orders placed. Meanwhile, underlying survey indicators gauging the export industry surprised negatively and point to further downward pressure on nominal manufactured goods exports as captured in the SARS Trade Statistics data (see chart 8).

Chart 8: Manufacturers not benefitting in full from a weaker exchange rate

Source: Global Insight, Stats SA, Momentum Investments

Cautious outlook regarding planned fixed investment outlays

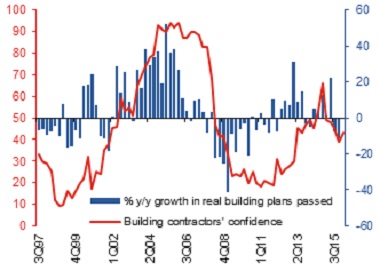

Building confidence rose marginally by four index points to 43 in 1Q16 (see chart 9), but underlying activity indicators measuring sentiment in the residential and non-residential building market decelerated further. The BER highlighted the weakness in forward-looking indicators as quantity surveyors and architects indicated pressure on possible projects in the pipeline. Building plans completed have also not kept up with building plans passed, suggesting that many plans are cancelled along the way.

Chart 9: Fragile growth prospects hindering building activity

Source: Global Insight, Stats SA, Momentum Investments, data up to 1Q16

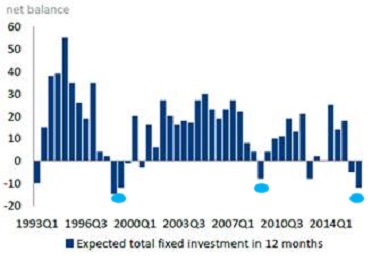

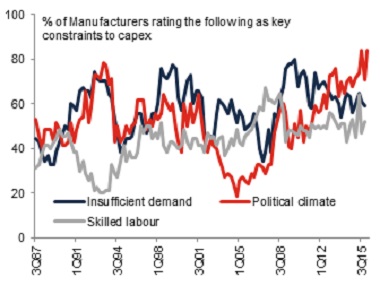

Moreover, the percentage of manufacturers rating the present level of output below capacity remains elevated. Manufacturers have maintained a cautious outlook on future investment spend (see chart 10) which tends to correspond with periods of high uncertainty. Manufacturers remain apprehensive of the consequences of an uncertain political climate. The percentage of manufacturers rating the current political climate as a key constraint to investment has once again spiked to all-time highs most likely on the back of Nenegate in early December 2015 (see chart 11).

Chart 10: Manufacturers scaling back on fixed investment plans

Source: Global Insight, Stats SA, Momentum Investments

Chart 11: Sign of increased uncertainty

Source: BER, Stats SA, Momentum Investments, latest data = 1Q16 (insufficient demand and skilled labour reading up to 4Q15)

Corporate profitability under strain

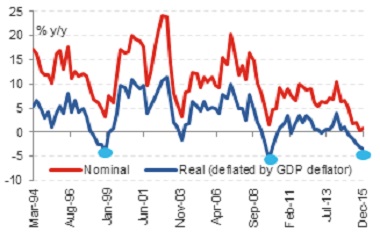

Stats SA data confirmed a collapse in growth in corporate profits in both nominal and real (deflated by the GDP deflator) terms against the backdrop of slowing economic conditions and mounting wage pressures. In nominal terms, growth in corporate profits dipped to an all-time low since the series began in 1994, whilst real growth has previously dipped into negative territory on three separate occasions (see chart 12).

Chart 12: Growth in corporate profitability stalls

Source: BER, SARB, Deutsche Bank, Momentum Investments, latest data = 4Q15

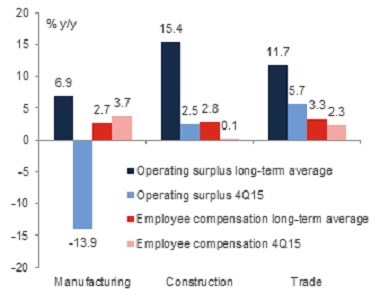

Meanwhile, growth in employee compensation has maintained a healthy clip, growing at 7.8% y/y in 4Q15 (2.9% in real terms). Although this has slowed from the long-term average of 10.2% (3.9% in real terms) and the post-crisis average of 9.6% (3.4% in real terms), wage pressures have compressed corporate margins. In the face of struggling growth in domestic demand, corporates will be forced to contain their wage bills to prevent a sharper collapse in corporate profit growth (see chart 13). This, in turn, highlights further downside risk to growth in household consumption expenditure as net hiring comes under further pressure.

Chart 13: Real wage growth still positive despite sharp slowdown in growth in profitability

Source: SARB, Momentum Investments, latest data = 4Q15, operating surplus=proxy for corporate profitability, employee compensation in real terms

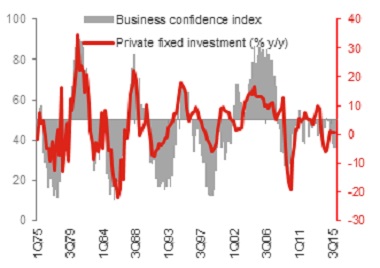

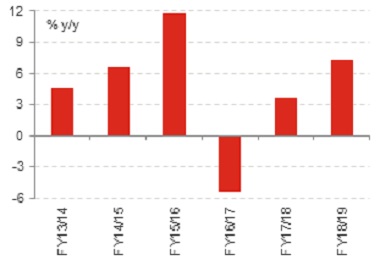

Three out of the four corporate profit recessions in chart 12 (denoted by the turquoise dots) have coincided with negative investment intentions as sketched out in chart 10. As such, elevated uncertainty and a collapse in profit growth are unlikely to provide much support to private fixed investment spend in upcoming months (see chart 14). Given that growth in budgeted public sector infrastructure spend is expected to contract over the next fiscal year (see chart 15), overall fixed investment in SA is unlikely to be a major driver of overall economic growth this year and next.

Chart 14: No quick recovery expected in private fixed investment

Source: BER, SARB, Momentum Investments, latest data = 4Q15

Chart 15: Treasury’s budget figures suggest a contraction in public infrastructure spend over the next fiscal year

Source: BER, SARB, RMB, Momentum Investments, latest data = 4Q15

Downside risks to SA growth view

Although we are already quite far in the downturn of the current economic cycle, as confirmed by the SARB, the BER has warned that should the underlying activity survey indicators dip further in 2Q16, we could see the overall business confidence index adjusting to even lower levels. This implies that economic conditions could get worse before they get better. Energy supply constraints and lingering policy uncertainty create a subdued environment for both new infrastructure spend and employment growth and will continue to stifle GDP prospects both this year and next. Against this backdrop, we do not expect the economy to expand by more than a 1% this year and close to 1.5% in 2017 with risks remaining to the downside as headwinds to domestic demand (fixed investment + household spend + government consumption) escalate. Moreover, a disappointing survey result on manufactured export orders suggest that suppressed global economic conditions and low commodity prices may partly offset the benefit of a weaker currency.