RSA 2013 Christmas sales outlook

The nominal growth in December 2012 retail sales of 6.1% (1.5% real) was by far the worst performance since 2009 and significantly below our expectations. This below-par year-end result was in stark contrast in the strong mid-2012 performance. Against this backdrop, and taking into account the assault on household finances, the current modest mid-year performance may well be expected to presage a disappointing year-end outcome.

In the first half of 2013, real demand (Gross Domestic Expenditure) grew just 2.7% (8.1% nominal) while real growth of 2.6% (8.3% nominal) in final consumption expenditure by households (FCEH) was recorded. Sales of durable goods (vehicles, furniture, appliances and electronics; accounting for 6.8% of total current FCEH), although still positive, are barely half the growth rates seen in recent times. Semi-durable sales (clothing, footwear, household textiles, tyres and vehicles parts; 8.6% of FCEH) performed well in the first half of 2013 while pressures on non-durable spend (essentially food and power/fuel; 41.6% of FCEH) translated into just a 2% real improvement in the first half of 2013. Spending on services (rent, medical, transport and communication; 43% of FCEH) is also reflecting embattled household spend with just 0.9% real growth in the first half of 2013.

Questions around the resilience of the consumer to ever escalating fuel, power, food, motor vehicle and other administered prices in the face of a stagnant jobs market have been growing for years and the imminent e-tolls in Gauteng provides only further concern. An estimated 5.4 million man-days have been lost due to strikes so far in 2013, predominantly in the private sector compared to 4.5 million man-days in calendar 2012. However the difference with last year is that most of the strikes to date have been protected whereas late-2012 strike activity was largely unprotected, resulting in significant wage losses to workers.

Affordability and the wherewithal of consumers to weather the economic climate drives consumer spend. Even including unsecured lending, debt servicing costs are relatively low at 7.7% of disposable incomes, but whereas the 6.6% debt service cost figure seen in 2004 was recorded at debt to disposable income levels of 58%, this figure is now at 75.8% despite four-decade low interest rates. Cumulative increases in fuel prices of most descriptions since the beginning of 2012 amount to almost 25%, affecting consumers as well as primary goods producers, intermediaries (agents and wholesalers) and retailers. Power prices have seen a similar rise (16% in 2012 and 8% this year). Both of these are displacing consumer spend, forcing businesses to close and adding to inflationary pressures throughout the chain. Thankfully the current over-recovery during October (21c/l for petrol up to 15/10/2013) is likely to see some respite for fuel prices in November.

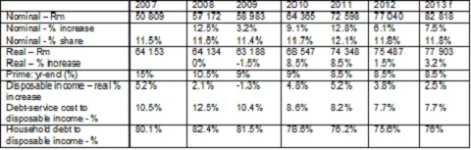

The strong performance in retail sales in 2010-2011 (see table below) and certainly over 2004-7, was due in large measure to the strong growth in disposable income of households, driven in turn by wage/salary increases outpacing inflation. Real disposable income of households grew 5.2% in 2011 but this rate slowed to 3.8% in 2012 and further to 2.2% and 2.4% in the first and second quarters of 2013 respectively (seasonally adjusted annualised rates). Obviously when growth in real disposable income slows, so does that in real consumption expenditure by households; this grew by 2.3% and 2.5% (saar) in the first and second quarters of 2013 respectively. If there is no wide-scale illegal strike action in the coming months and given average wage and salary increases of around 8% (refer to the Bureau for Economic Research (BER) third quarter of 2013 inflation expectations survey), then hopefully real disposable income growth will not moderate further.

After declining to 11.4% of total annual retail sales in 2009, the improving contribution of Christmas to total retail sales to 12.1% in 2011 was a welcome recovery but this came under threat last year, declining to 11.8%. Will this pressure intensify, causing pain for manufacturers, wholesalers and retailers? A factor to take into account in this regard is that many more consumers may have to rely on credit – whether it be in-house store credit or that provided by traditional financial institutions. Unsecured lending growth is tapering off while growth in credit extension to households of 8.2% in the first eight months has been trending lower of late.

Over the years better stock management has seen inventory levels ruthlessly rundown with industrial and commercial inventories to GDP falling from 17.3% in 2007 to 12.6% last year and remaining at those levels in the first half of 2013. Our experience to date is that a higher degree of advance ordering is taking place compared to last year but any dramatic improvement is unlikely in the near term in the face of high levels of uncertainty and lacklustre confidence.

Nominal retail sales have grown 7.3% (3% real) in the first eight months of 2013. We are detecting improved volumes in the run-up to Christmas across the food wholesalers and retailers with the hospitality side (restaurants and fast food chains) also being optimistic. In the ICT arena, tablets and smart phone demand shows no sign of slacking while on the IT front, a flat year has recently seen movement through the pipeline resulting in re-stocking ahead of Christmas. A large portion of durable and semi-durable goods are imported and the weak exchange rate may well affect retailers’ pricing power in the months ahead. Real sales of durable goods grew by 13.7% in the first half of 2012; this growth has fallen to 7.6% in the first half of 2013 but there is also invariably a pick-up in this segment at year-end. To this end we are currently experiencing strong growth in demand for cover in the household appliances, cellular and electronics sectors. This will go a long way towards offsetting the 3% nominal contraction in retail sales of household furniture, appliances and equipment experienced in the first eight months of 2013. The year-to-date 10.2% nominal growth in retail sales of hardware, paint and glass should also be sustained until year-end.

Given our cautious outlook, we foresee Christmas sales growing by 7.5% in current prices and marginally above 3% in real terms. The 10-year average for December sales is 10.3% nominal and 5.9% real. Caveats to this forecast do however include that there is no resurgence in strike activity that disrupts both production and workers earnings and that recent strikers don’t adversely affect the availability of certain goods (such as transport equipment and related accessories). To date large defaults have been the order of the day and average default values have risen. We are always wary of resultant potential stock overhangs in the first quarter of the new year and hence our advice to manufacturers and wholesalers at present would be to insist on short terms and to be wary of abnormally large orders. Retailers on the other hand will need to be cognisant that many consumers are having to reprioritise spending and that they will have to offer incentives in order to garner a share of the additional R5.8bn in sales expected in December.

Table – Christmas retail sales analysis

Source: Stats SA & SA Reserve Bank; CGIC analysis and forecast