Reserve Bank holds as South Africa clears first ratings hurdle

Dave Mohr, Chief Investment Strategist at Old Mutual.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

South Africa cleared the first two of three ratings hurdles, but with warnings that political infighting poses risks to the longer-term ratings outlook. Moody’s released a credit opinion noting that Government has a track record of good fiscal management, but reforms are needed to raise the longer-term economic growth rate. A downgrade would be likely in the absence of such reforms. Moody’s rates South Africa two notches above sub-investment (“junk”) status, with a negative outlook.

Fitch affirmed South Africa’s foreign and local currency ratings at BBB-, the lowest investment grade level, but changed the outlook from stable to negative. This suggests a ratings downgrade could follow in 2017. Fitch emphasised that political infighting in the lead-up to the ruling party’s elective conference next year poses risks to governance and policy making that in turn undermines the investment climate in the local economy. Like Moody’s, Fitch appears comfortable with the fiscal plans laid out in October’s Medium-Term Budget. It also noted that Government’s debt structure is “highly favourable”, with 90% denominated in rand and an average maturity of 14 years (and therefore limited roll-over risk). However, it is very concerned over the debt levels of state-owned enterprises, and political interference within these entities.

On Friday, S&P Global is expected to announce its decision. Like Fitch, they have historically been less lenient on South Africa than Moody’s. S&P has South Africa’s foreign currency rating one notch above junk status with a negative outlook, but the local currency rating is three notches above junk. The most imminent downgrade risk therefore stems from S&P, but even if it materialises, it would not impact South Africa’s inclusion in the major global bond indices. This would require two agencies cutting local currency ratings to junk status.

Some positive developments

While political uncertainty might have increased, other ratings factors have probably improved. An improved growth outlook for the domestic economy is positive for ratings, but more needs to be done to sustain growth. The recently released draft Integrated Resource Plan (IRP) should ease some concerns on the part of ratings agencies and investors in general. The IRP gives only a small future role to nuclear in the planned energy mix until 2037, and a bigger role to renewables and gas. This diminishes the likelihood of South Africa committing itself to unaffordable mega-projects.

There have also been some potentially favourable developments in terms of labour market reform, notably the agreement in principle between business, government and labour to mechanisms that will avoid protracted strikes (especially secret balloting), while an independent commission has proposed a national minimum wage of R3 500 per month. While labour representatives have complained that this is too low, and small businesses that it’s high, it appears to strike the right balance from an overall macroeconomic point-of-view.

Rand relatively resilient

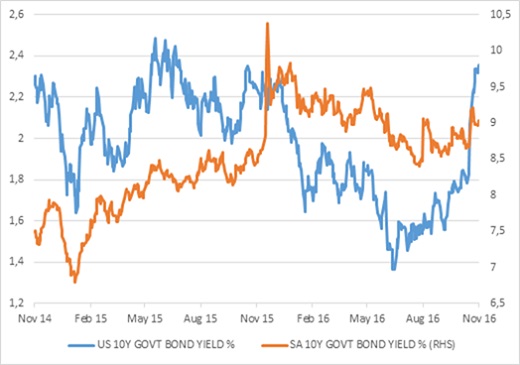

The rand remains within the broad range of R13.50 to R14.50 per US dollar, and though choppy, has reacted a lot better to the US election outcome than other emerging markets. The Mexican peso, Turkish lira and Indian rupee recently hit record lows against the dollar, with country-specific issues compounded by a sharp increase in US government bond yields. The 10-year Treasury yield increased sharply after the election from 1.8% to 2.3%, the highest level this year. The market is clearly pricing in much higher short-term US interest rates, which has led to capital outflows from emerging markets, including South Africa. It might be pricing in too many rate hikes. Since US mortgages are directly linked to long-term bond yields, borrowing costs have surged for an important sector of the US economy.

The key event from a rand point of view in December is not necessarily the ratings announcements, but rather the Federal Reserve’s monetary policy meeting. A 0.25% interest rate hike is highly likely and expected by the market, but the Fed’s own outlook for interest rates in 2017 (expressed in its statement and “dot plots”) will be crucial. If the Fed delivers more hikes in line with market expectations over the next three years, there is no reason to expect large-scale rand depreciation.

Repo rate unchanged

The path of US interest rates has long been of great concern to our own Reserve Bank. Its Monetary Policy Committee (MPC) unanimously decided to hold the repo rate steady at 7% as expected last week, but it is very much in wait-and-see mode. Against the backdrop of renewed global uncertainty, it noted its ‘continued vigilance’ on inflation, meaning that it will act if the inflation outlook worsens decisively.

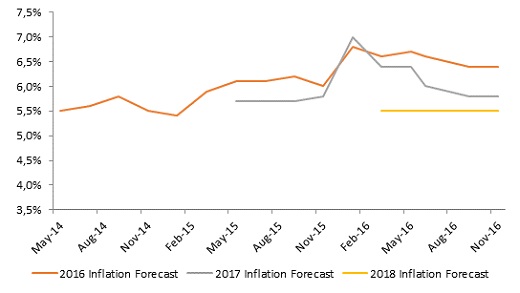

Its inflation forecast is broadly unchanged from the September MPC meeting, but the MPC’s view of the risks to this outlook has shifted from neutral to negative due to concerns over exchange rate volatility. The Reserve Bank expects inflation to average 6.4% in 2016, 5.8% in 2017 and 5.5% in 2018.

Actual consumer inflation came in higher than expected in October, mainly due to food prices. The consumer price index increased by 6.4% year-on-year, up from 6.1% in September. Food and beverage inflation accelerated to 11.7%. The outlook for food inflation at consumer level is that it will decline since food price inflation at factory level has already started decreasing, but remains high at 12.6%. Farm level food inflation has slowed sharply, from a peak of 27% in February to 10% in October. With the exception of coffee and sugar, global food prices are also negative on a year-on-year basis in US dollar terms. The combination of a more favourable base, a firmer currency and subdued global food prices all point to food inflation moderating next year.

Import prices are declining across a broad front. Petroleum, chemicals, metal products, machinery, computers, audio visual equipment and medical appliances all recorded notable year-on-year declines in September, the latest month for which import prices are available. The rand was marginally weaker on average in September 2016 compared to the same month last year, meaning the declines in import prices are not due to exchange rate movements.

The oil price, of course, is always a potential dark horse. It has firmed up in recent days as expectation has been building that major producers will announce an output cut this week. It remains to be seen if they will, given the strong fiscal incentives these countries face to increase production. The SARB assumes an oil price of $53 per barrel in 2017 in its inflation forecast. Petrol inflation was 0% in October. Due to the petrol price increase in November, and the declining rand oil price a year ago, petrol inflation will climb to around 8%. The current over-recovery of 42 cents per litre implies petrol inflation of around 5% in December.

Inflation expected to peak soon

The SARB expects inflation to peak soon and decline below 6% during the second quarter of next year. Core inflation, which excludes the impact of volatile food and energy prices, was a touch higher at 5.7%. The SARB expects core inflation to remain within the target range over the next three years.

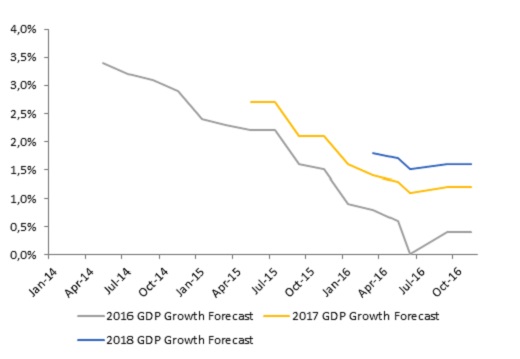

The SARB’s economic growth forecast is unchanged. It expects 0.4% growth this year, improving to 1.2% in 2017 and 1.6% for the following two years. Inflationary pressures therefore stem from supply-side factors, not because of strong demand in the economy. On the contrary, demand is weak, particularly on the part of households that have cut back borrowing substantially. Tighter fiscal policy (i.e. tax hikes and spending cuts) also means that there is scope to be more relaxed on the monetary policy side.

What are the investment implications?

It appears that the repo rate is close to or at its peak for the current cycle. Given the uncertainty around the US interest rate outlook, credit ratings and local politics, which could potentially impact on the rand, repo rate cuts are unlikely in the short term. However, a sustained downward drift in inflation should eventually lead rate cuts. This favours longer-term bonds over cash in fixed income portfolios. Bonds are also attractive relative to other asset classes, especially global bonds. The South African 10-year government bond currently yields 9%, probably already discounting downgrade risks to a large extent. This yield is already well above inflation, but there is also the prospect of capital gains if rates decline. Bonds can of course suffer capital losses too, as was the case last year in a rising inflation and interest rate environment and against the backdrop of a plunging rand. If bond yields decline, listed property also tends to do well.

Lower (or just stable) interest rates are good news for South African consumers and should benefit interest rate-sensitive sectors on the JSE (retailers and financials). However, equities are always a long-term investment and are influenced by many factors in the short term. In the long term, it is profit growth that matters to share prices, and lower rates obviously help not only consumers but also companies’ own financing costs. But to capture the long-term benefit of shareholding, one needs to remain invested for the long term.

Given the inherent uncertainty in markets – no one can predict the future – appropriate diversification remains important. Building a portfolio entirely around a single interest rate view (or forecast of any single macroeconomic variable) is risky.

Chart 1: US and South African bond yields

Source: Datastream

Chart 2: SARB’s real economic growth forecasts over time

Source: SARB

Chart 3: SARB’s headline inflation forecasts over time

Source: SARB