Reprieve for consumers as SARB keeps rates on hold

Maura Feddersen, Economist at Strategy at PwC.

The Monetary Policy Committee (MPC) of the South African Reserve Bank (SARB) kept interest rates on hold this week, aligning with market expectations. The repo rate and prime lending rate therefore remain at 6.50% and 10%, respectively.

Rising global trade tensions, emerging markets turmoil and disappointing domestic economic growth results put pressure on the South African currency in the weeks leading up to the interest rate decision, raising the risk of imported inflation. However, SARB Governor Lesetja Kganyago emphasised the central bank continues to look past short-term market fluctuations, staying focused on longer-term trends, such as those associated with global monetary policy tightening, rising oil prices and domestic wage inflation pressures.

Inflation results improved to 4.9% year-on-year (y-o-y) in August, from 5.1% y-o-y in July. The slight moderation in inflation outcomes suggests inflation expectations for 2018 did not require an upward adjustment by the SARB in September. Expectations for headline CPI inflation for 2019 were revised marginally upward to 5.7% from 5.6% previously, while inflation expectations for 2020 remain unchanged at 5.4%.

After a downward revision of the 2018 economic growth forecast in July, the SARB again revised downward its growth expectations from 1.2% to 0.7% to account for poor outcomes in the first half of the year. Governor Kganyago noted that the threat of demand pressures on the inflation outlook were muted in view of current economic conditions.

SARB could raise interest rates in November

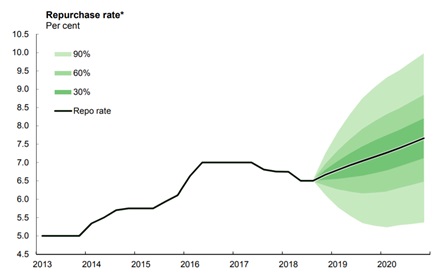

In the July MPC meeting, the central bank’s internal modelling tool suggested two interest rate hikes of 25 basis points (bps) were possible before the end of 2018 on the back of a worsening inflation outlook in 2019 and 2020. With a decision to keep interest rates on hold in September, an interest rate hike of 25 bps remains a possibility for November, when the last MPC meeting of 2018 takes place. However, if the risks to the inflation outlook moderate, especially those associated with currency weakness and rising oil prices, then the central bank may keep interest rates on hold in November as well, only embarking on the anticipated interest rate hiking cycle in 2019.

Repo fan, September 2018

Source: MPC statement September 2018

Looking further ahead, the SARB’s Quarterly Projection Model suggests five increases of 25 bps are possible by the end of 2020, which was also the SARB’s view in July. However, the central bank’s projection model serves only as a guiding tool, and shifts in the inflation outlook, or factors exogenous to the model could prompt action from the MPC to ensure not only that inflation remains inside of the target rate of 3%-6%, but also ideally becomes anchored in the middle of the range at 4.5% annually.