Repo on hold for now, but higher interest rates expected by year-end already

Maura Feddersen, Economist at PwC.

The risks to the inflation outlook have tilted to the upside since the central bank’s last Monetary Policy Committee (MPC) meeting in mid-March. In a statement following this week’s gathering of policymakers, South African Reserve Bank (SARB) Governor Lesetja Kganyago noted that the key drivers of elevated inflationary expectations were a slight weakening in the rand exchange rate (5% against the US dollar over the past two months) and increasing Brent crude oil prices, which recently broke through the psychological ceiling of $80 per barrel.

Furthermore, the impact of various indirect taxes, including the increase in value-added tax (VAT) and the levy on sugar-sweetened beverages have started to manifest in higher inflation readings. While this prompted the unanimous decision by members of the MPC to keep the repo rate at 6.5% and prime rate at 10%, the SARB has primed the market for a monetary policy tightening cycle that could begin sooner than previously anticipated.

April’s inflation results confirmed projections that inflation had reached a turning point in March. Following from a multi-year low of 3.8% year-on-year (y-o-y) in March, inflation ticked up to 4.5% y-o-y in April. This latest number was the 13th straight reading falling inside of the target range of 3% - 6%. SARB Governor Kganyago reiterated that inflation would likely peak around 5.5% y-o-y in the first quarter of 2019, from an expected average value of 4.9% in 2018.

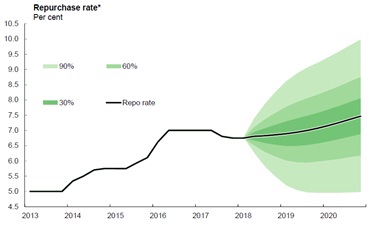

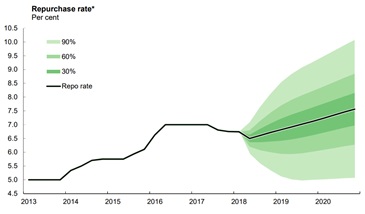

According to the SARB’s internal modelling tool, which serves as a guiding (but not prescriptive) policy guide, the renewed risks to the inflation outlook and various changed assumptions could prompt an interest rate hike of 25 basis points (bps) by the end of 2018 already. In March, the model suggested that a first hike of 25 bps would occur only at the end of 2019. The current view produced by the model suggests further increases in interest rates of 25 bps in 2019, and two 25 bps hikes in 2020. The prospect of an earlier tightening in monetary policy tightening reflects the changes in risks to the inflation outlook since the March meeting.

SARB interest rate forecast, March 2018

Source: SARB repurchase rate forecast, March 2018, the uncertainty bands for the repo rate are based on historical forecasting experience and stochastic simulations

SARB interest rate forecast, May 2018

Source: SARB repurchase rate forecast, May 2018, the uncertainty bands for the repo rate are based on historical forecasting experience and stochastic simulations

While headline inflation reached a trough in March, the prices of various segments of the food inflation basket are softening, including fruit prices, which declined by 8.2% y-o-y and bread and cereals prices, which eased by 3.7% y-o-y. This is good news for lower income households in particular, who spend a greater proportion of their income on consumption goods like food. Easing food price inflation forms part of the SARB’s set of updated assumptions and helps to mitigate the influence of a somewhat weaker exchange rate, rising fuel costs, and the impact of higher indirect taxes on inflation expectations.

The SARB will watch these drivers closely in coming weeks, with the MPC expected to meet again in July to deliberate a suitable interest rate stance that keeps inflation comfortably inside of the target range. The next interest rate decision is expected on Thursday, 19 July.