Recession arrived ahead of COVID-19 panic

Most industries ended 2019 on a low note

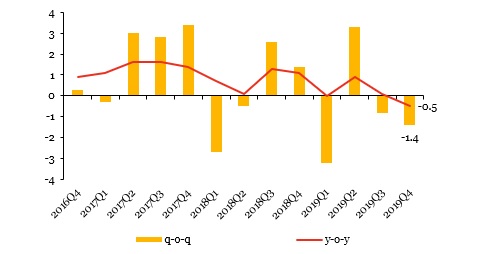

Statistics South Africa (StatsSA) reported on March 3 that the South African economy slipped into recession during the second half of 2019. Real gross domestic product (GDP) declined by 1.4% quarter-on-quarter (q-o-q) during the period compared to expectations of a 0.2%% q-o-q decline. Due to this contraction, economic growth averaged only 0.2% in 2019 compared to 0.8% in the preceding year. The 0.2% number was the weakest calendar year growth rate since the global financial crisis and marginally lower than the 0.3% used by the National Treasury for its revenue forecasts in Budget 2020.

Graph 1: GDP seesaw continues and swings economy into a recession

Source: Stats SA

Only three out of ten industries (mining, personal services, as well as finance, real estate and business services) posted positive q-o-q growth in 2019Q4. Mineral sales, for example, increased by 1.3% q-o-q during the October – December period and were 10.6% higher in 2019 overall compared to the preceding year. The finance, real estate and business services industry has been a reliable growth driver in the South African economy for many years and has not recorded a single q-o-q decline in real activity in the past four years. Other tertiary (services) sectors were not as fortunate, with the transport, storage and communication industry contracting for four straight quarters during 2019.

The mix of q-o-q changes resulted in the South African economy being 0.5% year-on-year (y-o-y) smaller in the fourth quarter – a negative y-o-y number has not been seen since 2016. On a calendar year basis, only three industries (finance, real estate and business services; general government services; and personal services) expanded in 2019. Trade, catering and accommodation activities were stagnant while the remaining six industries all contracted to varying degrees. The data reflects a very weak economy that has been stuck in a rut for quite some time. Construction activity was in a third year of recession in 2019 while mining and agriculture both contracted for a second straight year. Gross fixed capital formation also contracted for a second straight year while net exports also detracted from GDP growth.

There is currently a great focus on the operating climate for factories. The manufacturing sector contracted by 1.8% q-o-q and 2.6% y-o-y in the fourth quarter as manufacturing production declined by an average of 3.1% y-o-y during 2019Q4. Closer to the present, the Absa Purchasing Managers’ Index (PMI) declined for a fourth consecutive month to 44.3 in February 2020 – the lowest level in nearly a decade. Four of the five subcomponents of the PMI declined last month. A key reason for the decline in manufacturing activity was electricity loadshedding while weakness in external demand for factory goods also appeared to have contributed to a decline in sales orders – export sales declined for a fourth straight month.

Data released over the past weekend showed the extent of damage that the coronavirus disease 2019 (COVID-19) has caused the Chinese manufacturing economy. The National Bureau of Statistics (NBS) of China Manufacturing PMI plunged to a record low of 35.7 from 50.0 in the preceding month and a consensus forecast of 46.0. This PMI measures the performance of mostly large-scale, state-owned manufacturing companies. The Caixin China General Manufacturing PMI – surveyed amongst private industrial companies – dropped to 40.3 in February from 51.1 in the previous month. This was also the lowest level since the survey began in 2004 and well below the market consensus of 45.7.

Unsurprisingly, the rest of the Chinese economy is also under pressure. The NBS Non-Manufacturing PMI dropped from 54.1 in January to 29.6 in February. Fitch Solutions said last month that its scenarios suggest GDP growth in the world’s second largest economy could fall near 5% this year due to the adverse impact of COVID-19, compared to earlier projections near 6%. Calculations by the International Monetary Fund (IMF) suggests that this could result on a 0.2 percentage point decline in South African GDP growth this year due to adverse trade affects. (See here for more information on the impact of trade-disrupting COVID-19 on South African business.) Some forecasts are even more pessimistic on China’s growth outlook.

This is bad news for an already-tepid domestic growth outlook. The National Treasury said in its Budget Review 2020 released late last month it expects the economy to grow by 0.9% this year. It also suggested that growth could improve to above 1% in 2020 if the reforms outlined in its “Economic Transformation, Inclusive Growth, and Competitiveness: Towards an Economic Strategy for South Africa” discussion document are implemented at a moderate pace. Conversely, finance officials warned that an adverse scenario with mounting distress at state-owned enterprises, a worsening global growth outlook, deteriorating international trade relations, and less favourable bilateral trade conditions could push the local economy into another recession in 2020.