Rate cut expectations: what the SARB and US Fed might do this week

Anticipation is building as the South African Reserve Bank (SARB) and its larger counterpart, the US Federal Reserve (Fed), prepare to announce their upcoming interest rate decisions.

The Federal Open Markets Committee (FOMC) meeting is scheduled for 17 to 18 September, with the announcement scheduled at 2 pm EST on the 18th. This precedes the SARB rate announcement on 19 September. While the timing may seem fortuitous at first, it presents a challenge: the SARB must make its decision without insight into the Fed's actions as its meeting precedes the Fed announcement, thus it is deprived of crucial input. Despite this uncertainty, rate cuts are anticipated in both countries, with some arguing they are overdue.

A recent history of rates and rate cuts

The recent rate cycle has diverged significantly from the patterns of the past 30 years. The Fed hiked rates at the fastest pace in decades to combat the worst inflation in 40 years. These effects spilled over globally, resulting in higher inflation and rates worldwide, although not to the same extent as in the US.

At one point during the inflation spike, South Africa's inflation rate was more than 2.6% lower than that of the US, a historically rare occurrence. Typically, South Africa's inflation rate averages around 3% above the US rate.

This unprecedented rise in rates had significant consequences. Asset prices fell globally, investment flows into emerging markets reversed, and rates in economies worldwide rose in response.

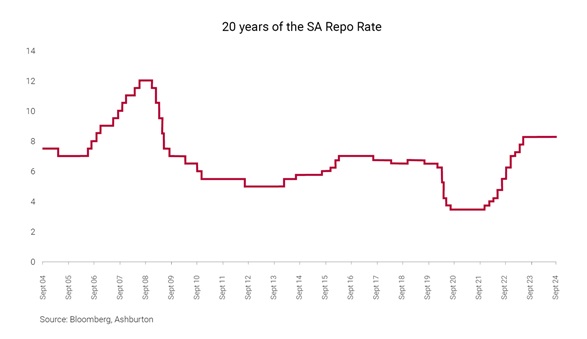

In South Africa, the Repo rate (the interest rate at which a country’s central bank lends money to commercial banks) is at its highest level since the spikes of 2002 and 2008, with the current real repo rate 3.65% above inflation. This real rate exceeds the 2008 peak and is the highest since 2006. Over the last 20 years, the average real repo rate was 1.16%.

With inflation under control in South Africa, why hasn't the SARB cut rates?

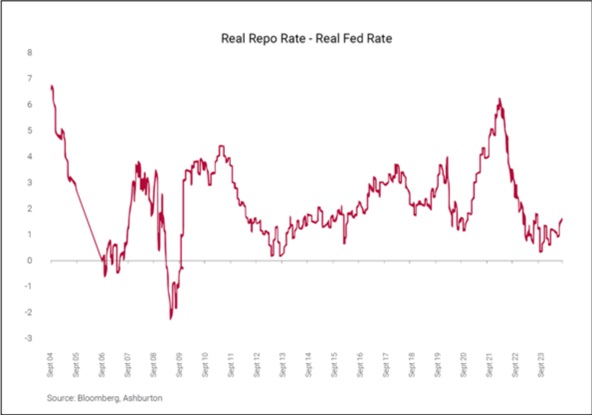

The answer once again lies in the US. Their recent inflation scare, slow progress in returning to target levels, and persistent economic surprises have prevented cuts. While South Africa's real rate is relatively high, the difference between its real policy rate and that of the US is historically low, constraining the SARB's actions significantly.

Current rate cut expectations

The Fed is expected to cut rates by either 0.25% or 0.5% at its upcoming meeting, with further cuts expected in 2024 and 2025, potentially lowering rates to at least 3.5% from the current 5.25%. This represents between 1.75% and 2.5% worth of cuts over the next 12-18 months.

The SARB is likely to mirror this rate path, with cuts expected at the end of the month and continuing through next year. Projections suggest the Repo rate will bottom out between 6.25% and 6.75%.

Potential impact of expected rates changes

These changes will impact various sectors of the economy. For most people, this will provide welcome relief on home loans, credit cards and other debt. New homeowners can expect monthly payments to drop between R750 to R775 per R1-million loan size with the first 1% worth of cuts, while those with about 10 years left on their loans will see a reduction of R620 to R650 per R1-million outstanding.

For market participants, lower rates typically benefit riskier asset classes such as property and equity, particularly if South Africa's socio-economic circumstances continue to improve. While fixed income funds may yield less in absolute terms, real returns remain attractive as local inflation continues to fall towards 4% or lower.

We are entering a new chapter in local and global markets, with lower inflation and falling interest rates. However, this era will likely differ from much of the last 20 years. Interest rates globally are expected to remain in positive real territory for the foreseeable future, unlike much of the recent past post the 2008 crises. These higher rates should better balance the needs of both borrowers and lenders, potentially leading to improved long-term outcomes for both.